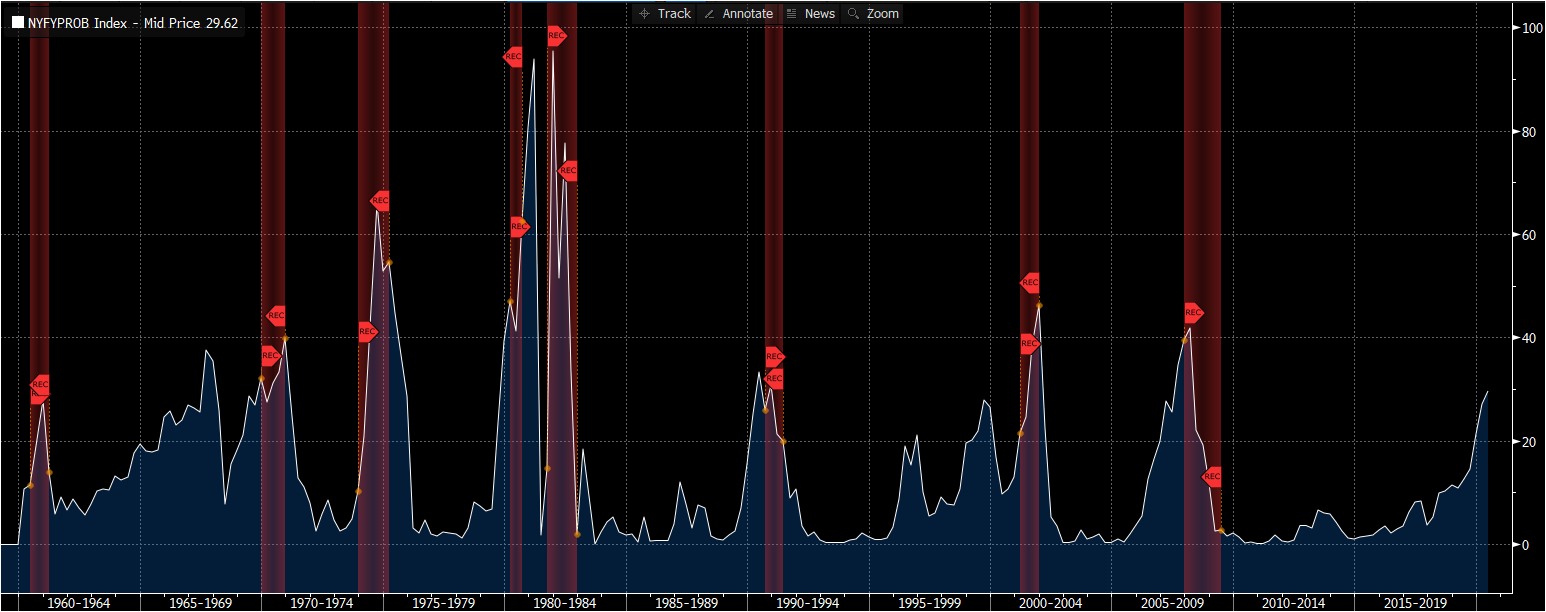

Hong Kong simmers, trade war is all about Trump, and Boris kicks off his campaign. Hong Kong on edgeProtesters are blocking major roads in downtown Hong Kong, and they have vowed to stay until the government withdraws controversial legislation that would for the first time allow extraditions to China. Clashes have been reported and police have used tear gas and rubber bullets to control what they called a "riot situation." Both the extradition plan and the unrest are the kind of things which spook market participants, and stocks in the city tumbled amid concern about capital outflows. Somewhat counter-intuitively it all supported the Hong Kong dollar, because it pushed up interbank interest rates as well as the cost of shorting the currency. In a show of support for protesters, U.S. Congressional leaders have vowed to review Hong Kong's special trading privileges if lawmakers pass the bill. The latest coverage is here. It's all about DTPrepare to be shocked: The biggest obstacle to a U.S.-China trade deal that could rescue global growth from the brink of a slow down is none other than Donald J. Trump. Tariff Man said on Tuesday he's personally holding up an accord and that he won't complete the agreement unless Beijing returns to terms negotiated earlier in the year. The brinkmanship puts Xi Jinping -- China's strongest leader in decades -- in perhaps the toughest spot of his six-year presidency. If he caves to Trump's threats, he risks looking weak at home. If he declines the meeting, he must accept the economic costs that come with Trump possibly extending the trade conflict through the 2020 presidential elections. Currently the silence from Beijing is deafening. Everything will be fine, Five Things is telling itself as it hugs its legs and rocks quietly in the corner. Enter BorisLook, you don't like it, and we don't like it, but this U.K. leadership contest could have some pretty profound implications for British and European assets, so let's just get this done. Boris Johnson today launches his campaign to become prime minister, and the centerpiece of his pitch is to take the country out of the European Union on Oct. 31, come what may. For those who fear a no-deal departure that's a worry, because among the painfully large field he is the favorite. But even if he wins the contest, he may face a battle to keep his word – the opposition Labour Party is trying once again to seize control of the Parliamentary agenda as part of an effort to stop the next leader taking the U.K. out with no deal. It's fine. Everything is fine. MarketsJune's risk rally has faltered. The MSCI Asia Pacific Index dropped 0.4%, led by that slump in Hong Kong. Japan's Topix finished 0.5% lower. The Stoxx Europe 600 index was also down 0.5% as of 5:56 a.m. Eastern time, the S&P 500 was set to decline at the New York open, the yield on 10-year Treasuries was at 2.12%, and gold was climbing again. Coming up...It's inflation day! The latest U.S. consumer price data will hit at 8:30 a.m., and you'll want to tune in. Why? Well, remember that Fed guy Powell saying that he thought weak inflation was likely "transitory"? This release will give us a clue whether he is right, and if he is it could be bad news for the recent bond rally. Speaking of, there's also a 10-year Treasury auction a bit later. Otherwise, feel free to take off the rest of the day. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Sid's interested in this morningFor all the paranoia over trade tensions and the risk the Fed doesn't cut rates this year, there's a decent slew of positive stuff happening right now. U.S. financial conditions are at a five-year norm -- suggesting whipsaw markets aren't really dragging down on growth. Central bankers keep reminding us implicitly that they will cap real rates to keep the debt-driven supercycle going. For all the talk of currency wars, relatively muted equity price swings and synchronized dovish monetary policy are killing FX volatility. And as Jefferies points out, rate cuts are happening all over the place, from New Zealand to the Philippines, without central bankers having to worry that weaker currencies will boost imported inflation. Meanwhile, the fall in Treasury yields is rekindling carry trades around the world. Against this risk-taking backdrop feeding growth, the outlook for the second half of the year feels more binary than usual. Bonds seem to be flashing recession signals, as per the New York Fed's implied recession-probability model. It's at 29% right now, the highest since 2008. Yet other lead indicators from the OECD may suggest a tentative pick-up in the coming months.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. Before it's here, it's on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can't find anywhere else. Learn more. |

Post a Comment