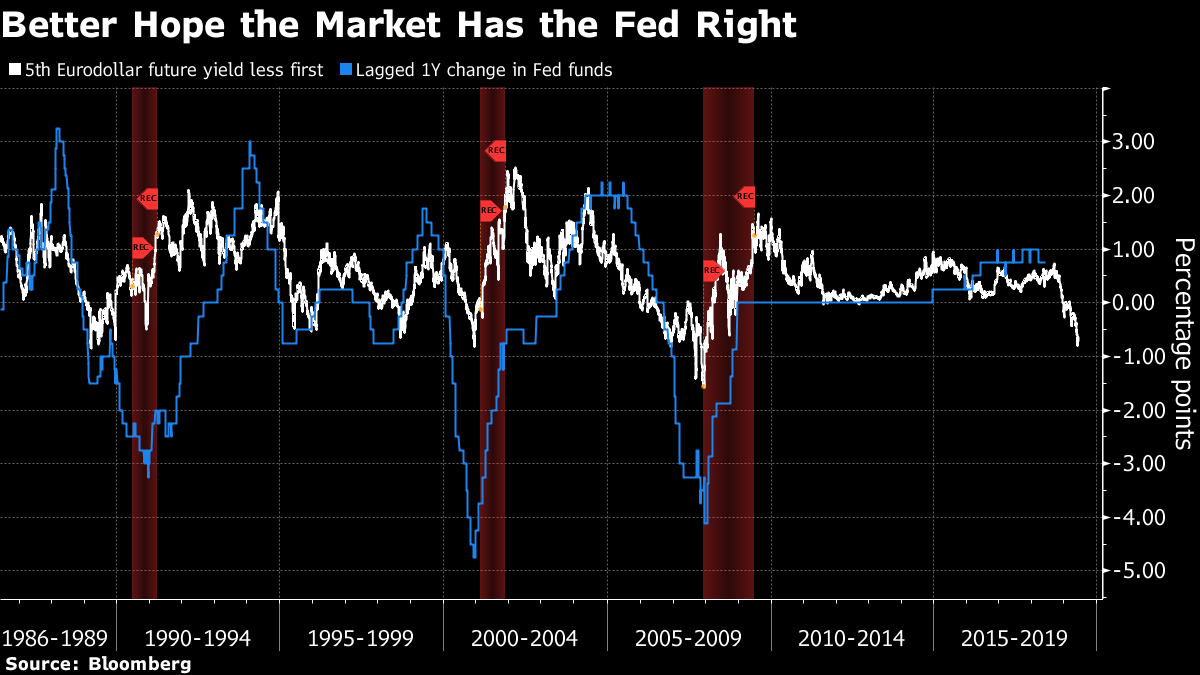

Trouble with Tehran, companies lobby Trump on tariffs, and a new era for White House communications. Here are some of the things people in markets are talking about today. Risky businessGiven all the angst over trade and growth coursing through financial markets, a sudden uptick in geopolitical tensions is ill-timed, to say the least. The big flash point right now is the Persian Gulf, where stress is building after the U.S. assigned blame for two oil tanker attacks on Iran. Tehran denied involvement. (And there's certainly an argument that the potential benefits to the nation are outweighed by the risks.) But then American officials released images of what they say is an Islamic Revolutionary Guard Corps patrol boat removing an unexploded mine from one of the vessels. The extent of the spillover to markets is unclear; even oil is taking developments in stride as the potential supply shock of a Middle East conflict is counter-balanced by a trade-war driven drop in demand. For now, anyway. Listen to your heartSpeaking of the trade war, Five Things is sad to report it didn't suddenly disappear overnight. That's not for want of trying in some quarters, however. More than 500 companies and 140 groups representing manufacturers, retailers, oil and gas firms and other industries signed a letter addressed to President Donald Trump on Thursday from "Tariffs Hurt the Heartland," an umbrella group of trade associations that's pushing back against the protectionist showdown. Wal-Mart Inc., Target Corp. and Macy's Inc. were among the names asking Tariff Man not to do his thing and to return to the negotiating table. He may not feel like easing the pressure on China, however, since the man on the other side of that table suddenly has a whole lot of problems. Some consolation for Xi Jinping, though: he isn't the only one trying to figure out how to deal with Trump. So long, SarahAfter a turbulent tenure marked by attacks on the media, dissemination of false information and the near-disappearance of the daily press briefing, White House Press Secretary Sarah Huckabee Sanders is leaving the Trump administration. She's going at the end of the month, with no replacement yet named. Investors will wait and watch with interest to see who will take over, as any possibility of a return to a more regular and/or stable flow of communications from the White House will surely be welcome. Then again, given some of Sanders' work, maybe it wouldn't. MarketsInvestors are showing caution as the week comes to an end. The MSCI Asia Pacific Index edged lower by 0.1%, led by the gauge in Shanghai. Japan's Topix was a regional winner, finishing 0.3% higher. The Stoxx Europe 600 index fell and was 0.5% lower as of 6:01 a.m. Eastern time. S&P futures pointed to a dip at the open, the yield on 10-year Treasuries dropped to 2.06%, and gold jumped again. Coming up...Seriously? It's Friday people, could we not just take it easy today? No? OK, fine. The big data drop will be retail sales numbers at 8:30 a.m., with everyone on guard for a shock that might make Jerome Powell say the same dovish things again but more forcefully this time. Industrial production is 9:15 a.m., and University of Michigan sentiment figures are at 10:00 a.m. alongside business inventories. The Baker Hughes rig count is at 1:00 p.m., and after that we're pretty sure you'll be allowed to go home. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Luke's interested in this morningThe Fed's task is far from easy: if the June dot plot and forecast revisions point to softening in the U.S. economy and the need to lower rates from current levels, there will be confusion as to why the central bank isn't taking proactive action to allay the soft patch. However, if growth and inflation forecasts remain relatively unchanged and the median estimate for rates doesn't suggest easing is in the offing, the central bank risks another tone-deaf "transitory" or "autopilot" moment. In a webcast on Thursday, DoubleLine's Jeffrey Gundlach was asked if the Fed would be capitulating to Trump if they lowered rates. No, he said, the central bank would be capitulating to the bond market. Weeden & Co. chief global strategist Michael Purves has similarly referred to the bond market "taunting the Fed" at current pricing. Given the limited sample size of U.S. downturns, it's completely fair to argue that things are different this time, with a benign outcome for the American economy on the cards even in the absence of rate cuts. But the scariest thing for financial markets and the U.S. economy could well be if the bond market is wrong. For all the talk about how the bond market always gets the Fed wrong, there's not been so much in the other direction. History says whatever the Fed needs to deliver to offset headwinds is at least what the market's thinking or more. To be specific, when the yield spread between the fifth and the front-month Eurodollar futures contracts (a proxy for one-year market-implied easing) is this negative, the Fed has either delivered that much accommodation or much, much more.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. Before it's here, it's on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can't find anywhere else. Learn more. |

Post a Comment