| The monetary menagerie on days like this can get confusing. Beyond hawks (who want tighter money) and doves (who want easier money), there is also the retinue of bulls and bears, all braced for potential black swans, such as viruses. But it looks as though the world is finally ready for a new and apparently much less menacing animal: the tapir. The bottom line from Wednesday's meeting of the Federal Open Market Committee, as communicated by Chairman Jerome Powell, is that the taper will arrive in November, and continue munching away at the Fed's monthly purchases of assets until they are all gone, in June of next year. At that point, the tapir can retire not very graciously into the sunset, its proboscis swaying gently in the breeze. Everyone can then start worrying about rates. He was sufficiently clear about how the Fed views the next few months to leave little doubt. For a long time the necessary condition for starting to taper off support has been "substantial further progress" toward the goals of raising inflation and bringing unemployment under control. Powell said it "wouldn't take a knock-out employment report" next month, just a "decent" one to pass this test. He added that the substantial further progress test "in my own thinking is all but met." Barring some surprisingly bad economic data next month, we should assume that the tapering progress will get under way at the next FOMC meeting, in November.

Moreover, Powell was far more explicit than he needed to be over the likely timing of the taper, saying that a gradual tapering "that concludes around the middle of next year" was likely to be appropriate. This means that when the tapir arrives, it will do so at an ungainly gallop. Doing the arithmetic, the most sensible reading of Powell is that the Fed starts tapering at $15 billion per meeting (or put differently, $10 billion per month), starting in November. That would get the job finished next June. It would also be a more aggressive monetary tightening than many expected.

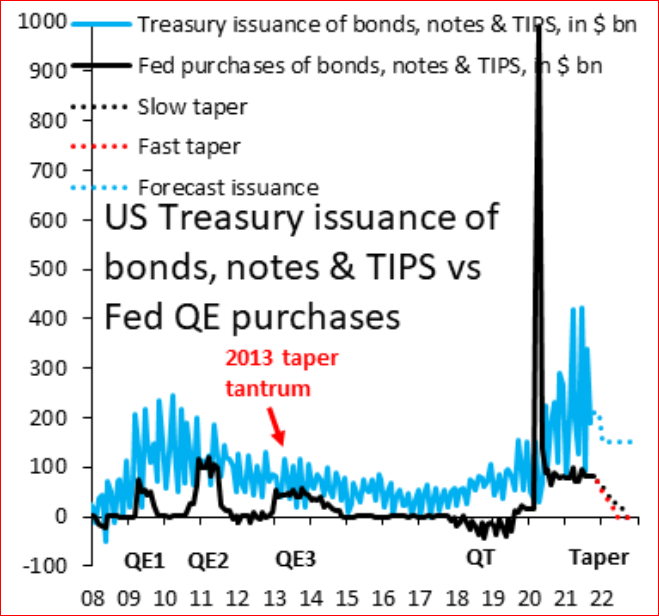

Robin Brooks, chief economist of the Institute of International Finance, offers the following chart, with the scenarios of a "fast taper" and a "slow taper" (phrases that become much more fun if you visualize them through the tapir analogy):  As Brooks said on Twitter: The FOMC thinks QE should be done by mid-2022. That means a "fast" taper (red), i.e. $10 bn drop in purchases of Treasury securities PER MONTH, not PER MEETING, which gets you done by June. It also means announcement Nov. 4 & Nov purchases down to $70 bn from $80 bn in October.

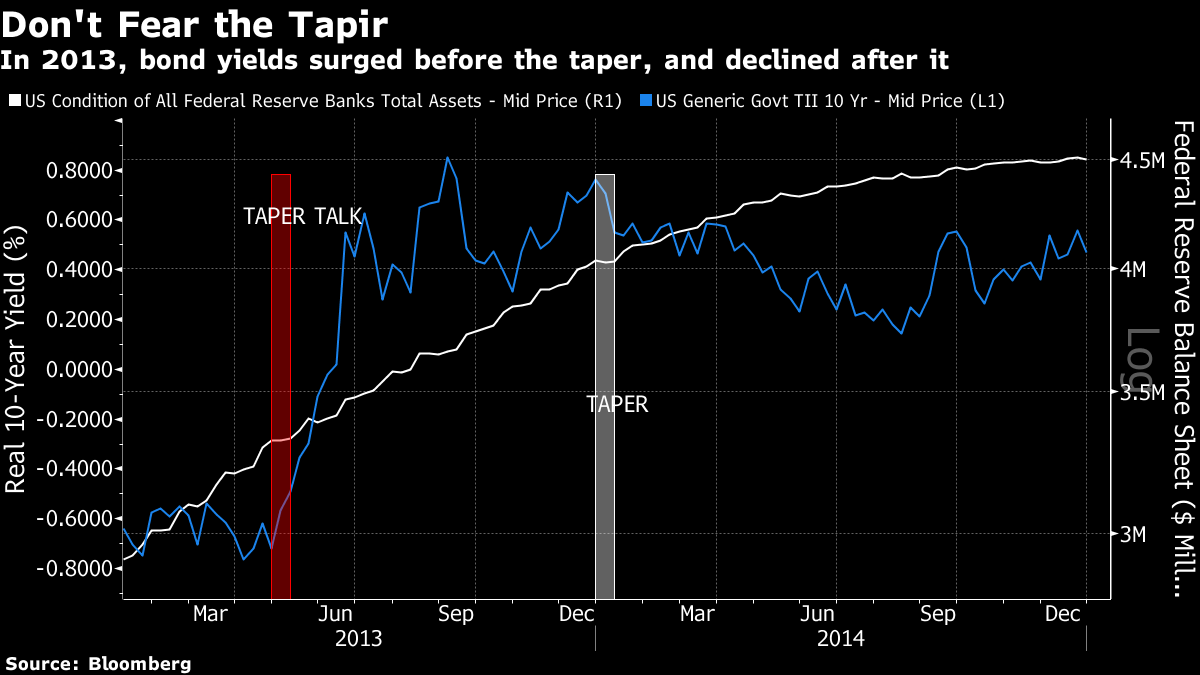

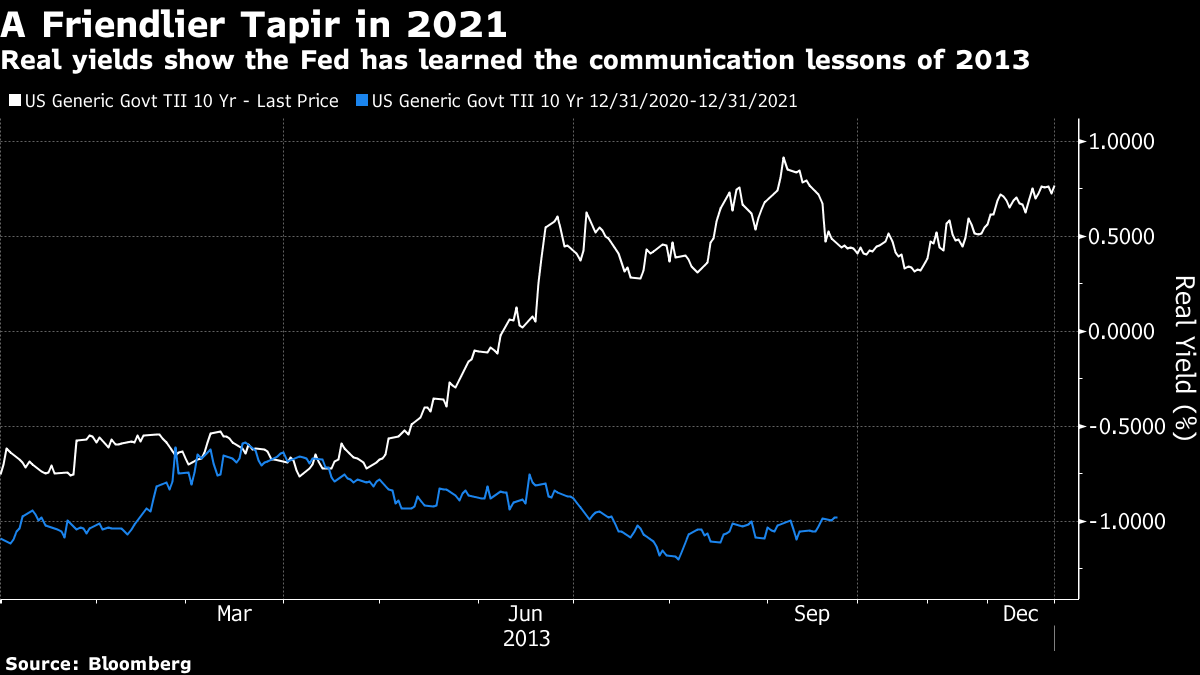

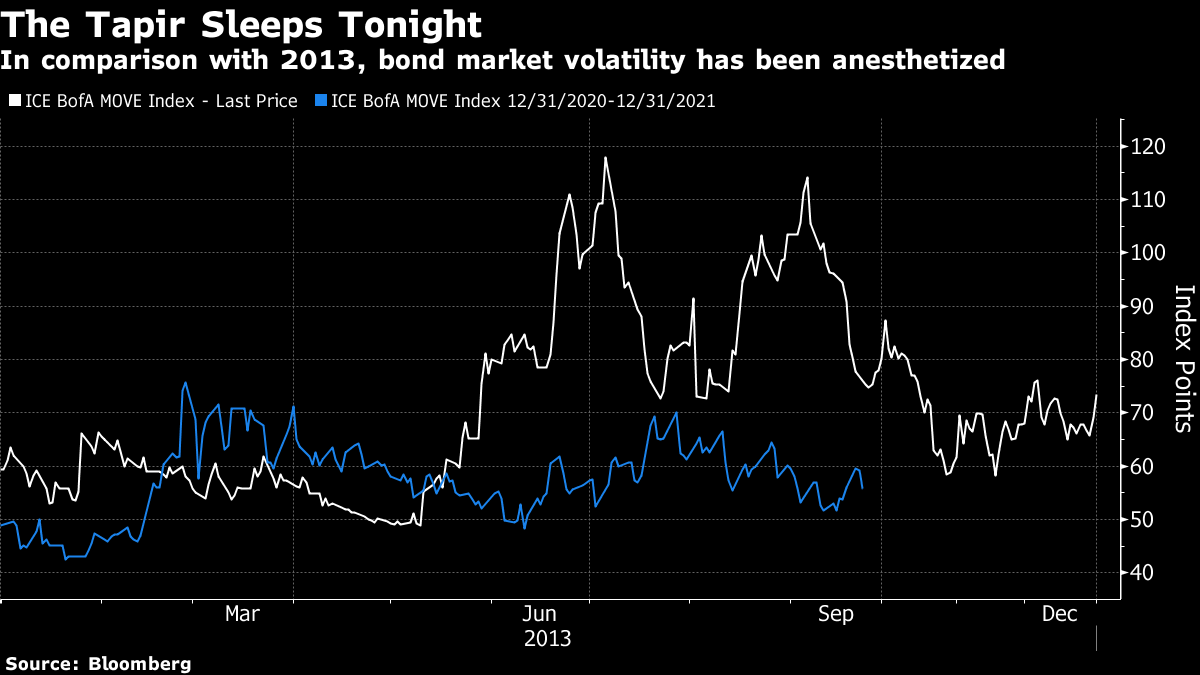

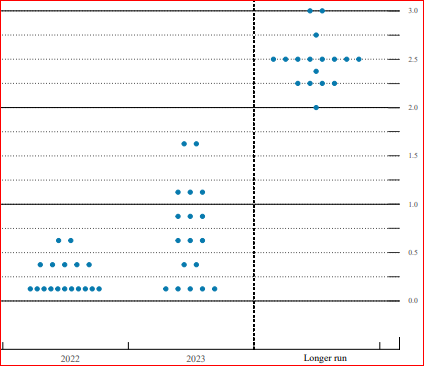

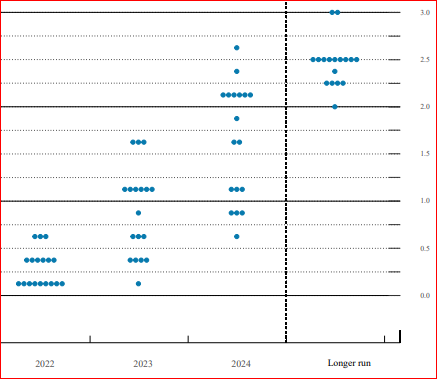

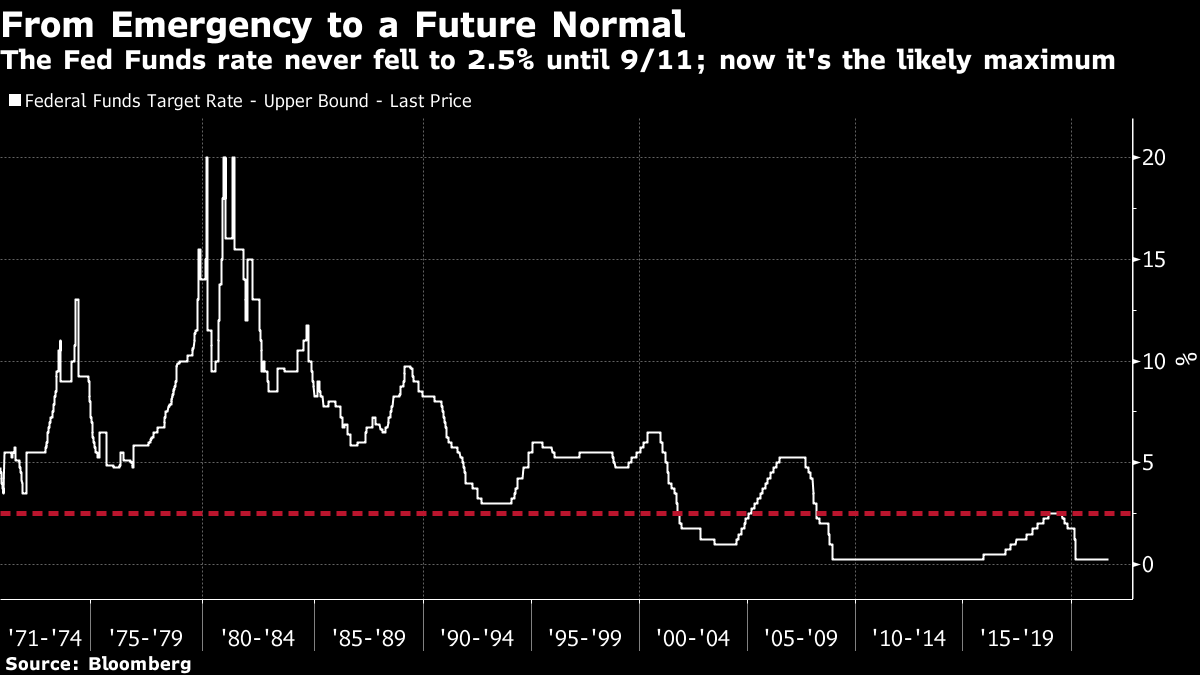

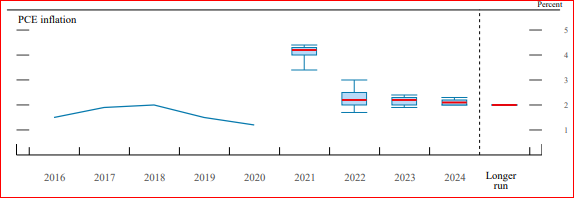

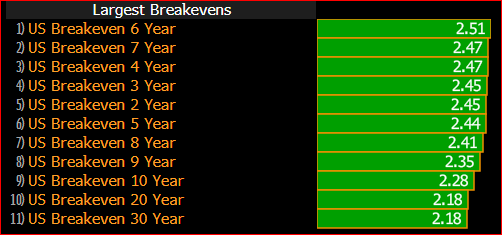

So this was a "hawkish hold" leading to a fast tapir. And the market scarcely batted an eyelid. The Fed has spent much of this year looking at the example of 2013, when poor communication about tapering caused real yields to surge starting in May, long before the eventual taper announcement in May. Once the tapering had actually started, real yields began to decline:  This Year of the Tapir could scarcely have been more different. There was an incipient tantrum in rates early in the year, which has subsequently been totally reversed. In 2013, the surge in rates scared the Fed into a major surprise, when it announced that it would not after all start tapering in September. It waited until December. At this point, the market is supine and gives no reason for Powell and his colleagues to delay:  If we look at bond market volatility, as measured by the ICE BofA MOVE index, we again see that traders are remarkably calm about this year's taper, by comparison with 2013. Then, the Fed waited for the MOVE to decline before tapering in December. This time it should be able to start in November:  So the Fed has comprehensively avoided repeating its mistake of 2013. But the next move promises to be harder. When will it start hiking interest rates? Unusually, Powell used his press conference to draw attention to the "dots" in which each FOMC member lists their predictions for inflation, growth, unemployment and the benchmark fed funds rate on a dot chart. He normally downplays the dots. This time he happily pointed out that half of the committee have now said they expect rates to rise once next year. This means that some have grown more hawkish since the last dots were published in June. The following chart shows expected fed funds rates from June, above, and from September below:   A majority now expects to hike next year, the recalcitrant minority that expects rates still to be on the floor by the end of 2023 has been reduced from five to one. This is a fairly direct message to all and sundry that the Fed is more hawkish than had been thought However, there are limits to this. If we look at the fed funds rate over history, we discover that it first dipped as low as 2.5% after the 9/11 terrorist attacks of 2001. While that was an emergency measure in response to a disaster, the FOMC now seems confident that 2.5%, marked in red on the chart, is going to be the ceiling from now on:  This is a picture of a horribly sluggish "new normal." Meanwhile, inflation predictions in the dot plot also suggest that FOMC members think we will stay in the doldrums for a long time. Their prediction for this year is high, but 2021 is 75% over; it isn't so much a prediction at this point as an acknowledgement of reality. For the longer run, they expect inflation to get back as low as 2.1% by 2024, and then settle in at 2%:  This suggests minimal faith in growth, and great confidence in the thesis that the current inflation is transitory. It also suggests that the Fed is noticeably more confident about low inflation even than markets. This is a screen shot of where inflation breakevens out to 30 years stood at the close of the day (using the ILBE function on the Bloomberg terminal):  So the Fed arguably now looks too confident about beating inflation, yet also to be rather more hawkish than many thought necessary. Put those together, and it seems to be rather more energized to limit inflation than previously advertised. The big takeaway from Jackson Hole last year was the beginning of average inflation targeting, or AIT, which meant allowing price increases to run above target for a while. The dot plot is predicting that that won't happen. Steve Blitz, chief U.S. economist for TS Lombard, suggests that this could also have negative effects for the U.S. economy by strengthening the dollar: What is more interesting is how the unnerving of the FOMC's resolve to run inflation hot, telegraphed in and around the Jackson Hole speech by Powell and others, has morphed into a "same old, same old" pace of tightening in 2022, 23, and 24. We are now up to a split in the FOMC on hikes next year (Last November I forecast the first hike in Dec 2022) with 3 voting for two hikes. Everyone is on board, save one, for hikes in 2023, with 10 looking for the year-end funds rate to be 0.875% or higher (3 are at 1.625%).

As market pricing increasingly reflects a Fed that has not "changed its spots" (what was all that Fed listens and the announcement of AIT for? To impact markets short-term), their policy guidance will counter benefits coming from government on trade and boosting domestic capital investment by, in effect, re-engaging a strong dollar policy.

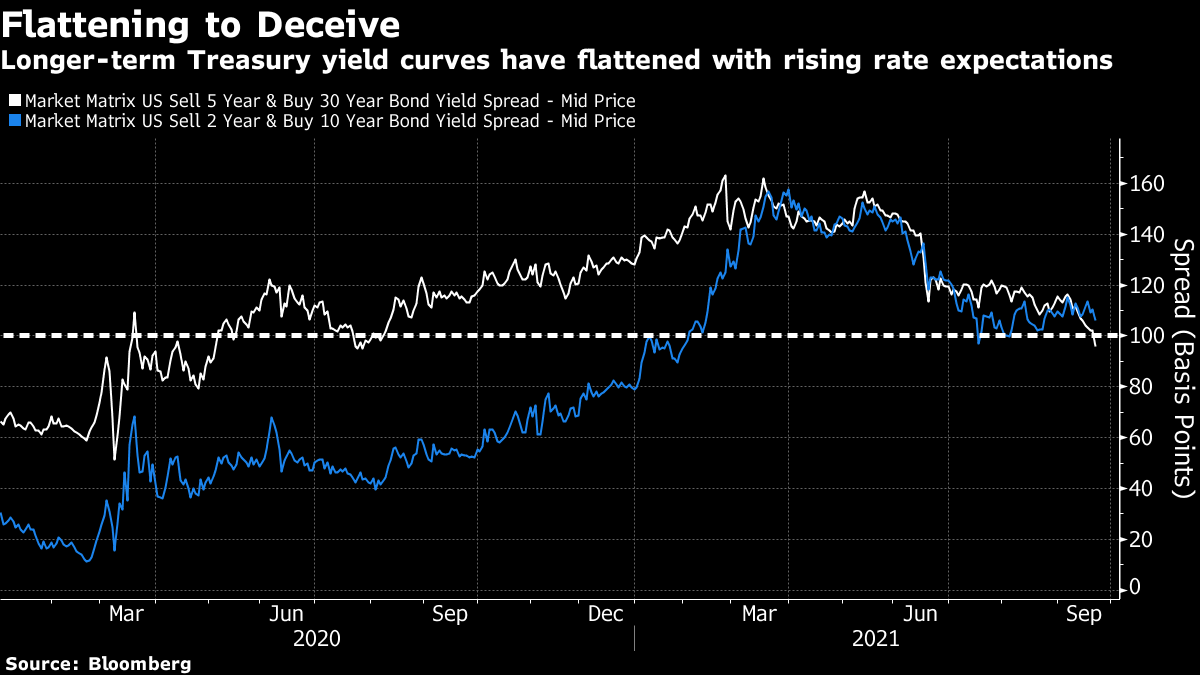

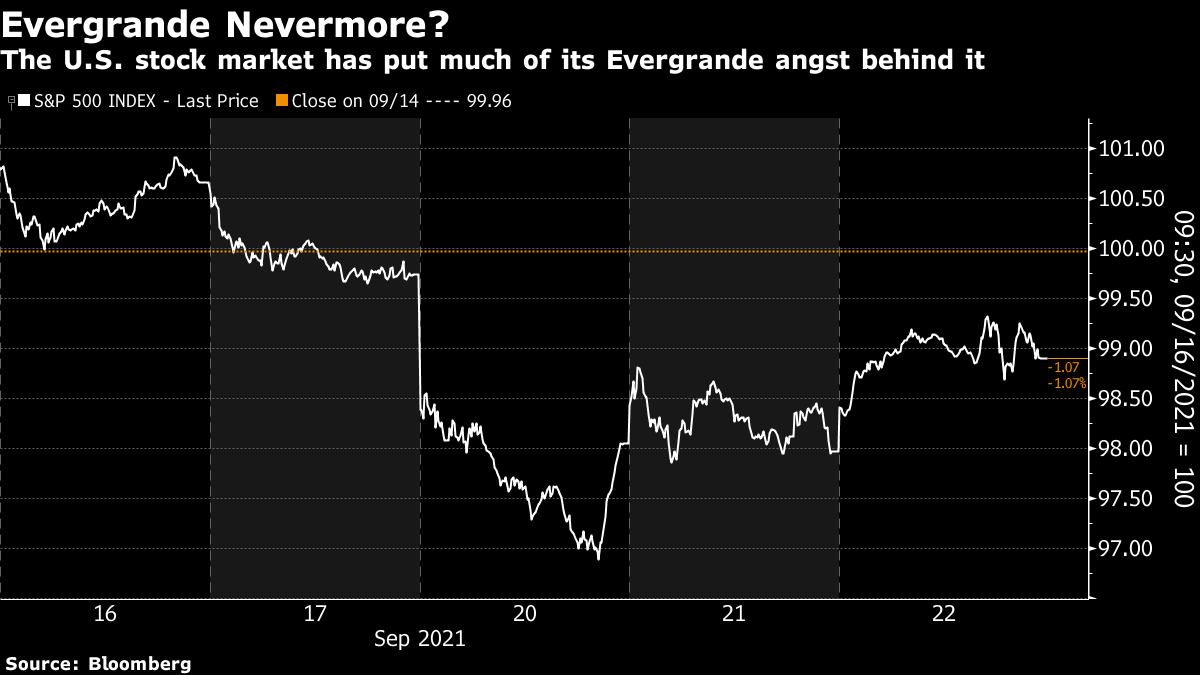

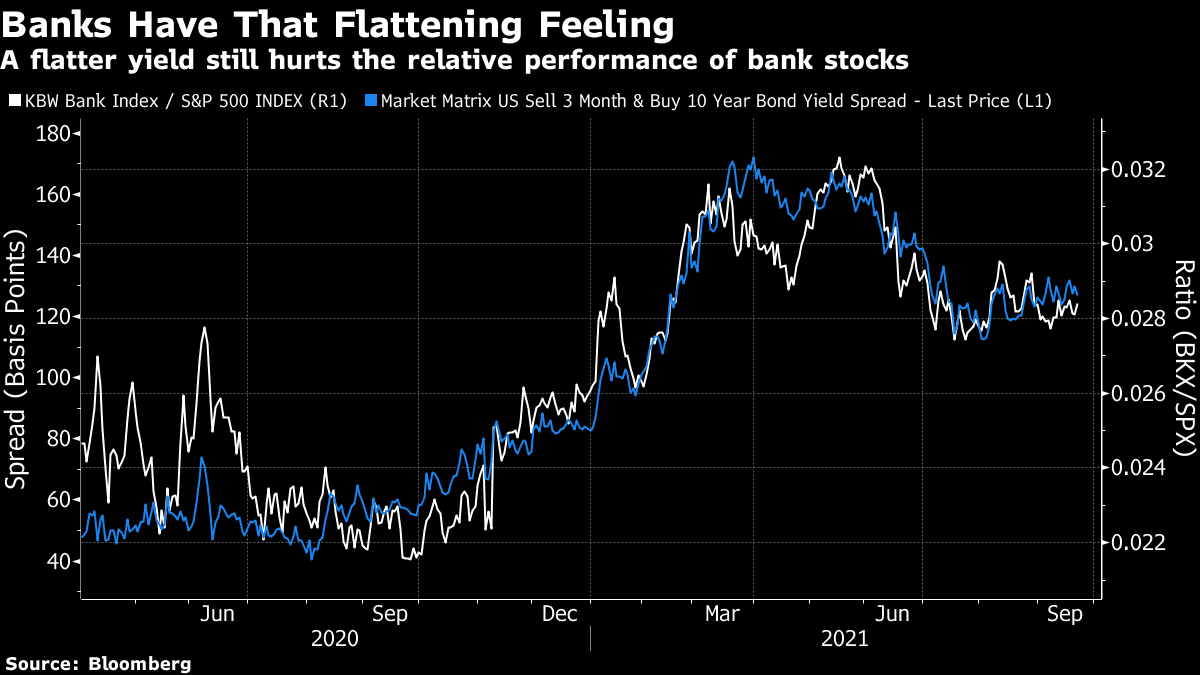

Digging into the subtleties of the bond market, it looks as though investors in Treasuries share Blitz's concern. The yield curve is flattening, particularly at its longest-term extremes. The spread between 5- and 30-year yields dropped below 100 basis points after the FOMC meeting, for the first time since just before last year's Jackson Hole's conference. Such a flat curve implies that there won't be much inflation in the future, but also that there won't be much growth. It's a signal that the bond market thinks the Fed is going to make a hawkish mistake, and stamp out the life in the economy, when previously there had been a belief that the Fed would be easy and let inflation move higher:  Meanwhile, the stock market's reaction suggests stunning insouciance. It took a long time for the U.S. equity market to wake up to the threat posed by the China Evergrande Group imbroglio, then there was the spasm of selling on Monday morning; now calm has returned. With no obviously good new news about Evergrande, and some rather unwelcome news from the Fed, there were plenty of excuses to sell. But stocks held firm:  The yield curve did continue to work its malign magic over the banking sector. Banks are traditionally held to benefit from a steeper curve as it makes the lending business more profitable; and since the crisis calmed down last April, bank stocks' relative performance has moved in line with the curve. It's another clear indication that the "reflation trade", which involved outperforming banks, has run aground. That is at least in part because investors think the Fed has been too hawkish:  But the lasting impression from the day is that for markets the tapir no longer has the power to induce fear in the way that it did eight years ago. That Powell was about as hawkish as he could be, and yet stocks continued their rally, does at least prove that one other market animal didn't make an appearance. The post-Evergrande bounce has some life in it. It's no dead cat. I have another suggestion for reading. After a summer hiatus, the Bloomberg book club is about to spring back to life. As trailed at the beginning of the summer, we will be discussing Winning the Loser's Game, by Charles D. (Charley) Ellis, the investment classic that established the case for passive investing among many other things. An eighth edition came out earlier this year, and Ellis contends that his thesis looks stronger than ever. We will be discussing it with Ellis on the terminal during the first week of October. The book is worth reading for any subscriber to this newsletter. But even if you've never read it, or it's been a while since you looked at it, the conversation is likely to be fascinating. Watch this space, and read Winning the Loser's Game if you can. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment