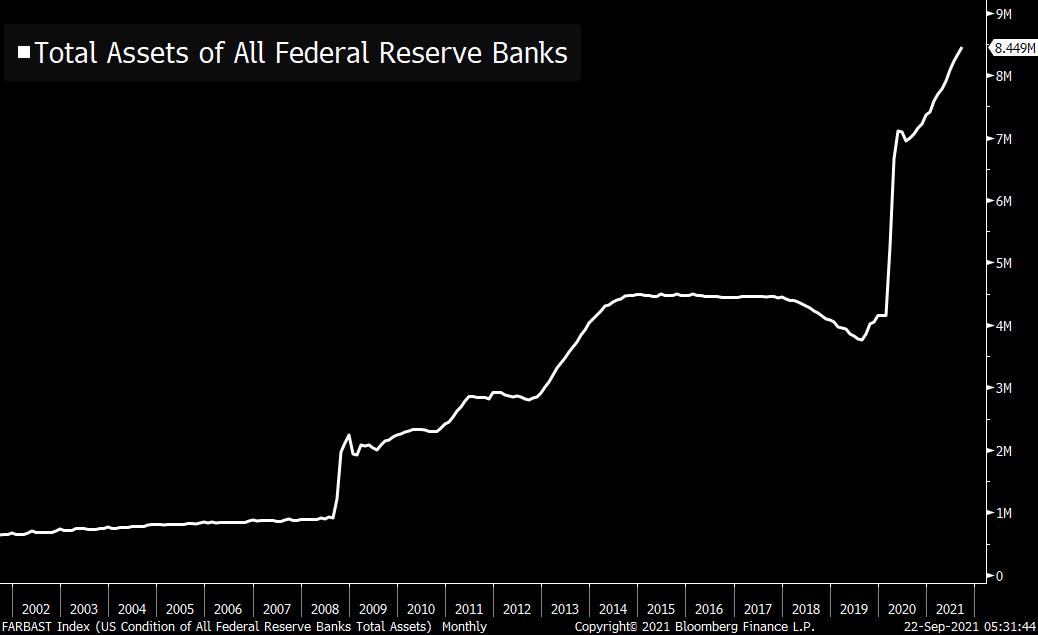

| It's Fed decision day, Evergrande fears ease, and debt ceiling standoff intensifies. The Federal Reserve isn't expected to unfurl it's much heralded taper announcement today, but the meeting is seen as a chance for Chair Jerome Powell to lay the groundwork for a decision to slow asset purchases in November. The statement, which includes updated projections for interest rates, is at 2:00 p.m. Eastern Time and will be followed by a press conference with Powell 30 minutes later. His task of convincing investors that the time might be coming to start withdrawing stimulus is made more difficult by the myriad risks facing the global economy. Markets, and Powell of course, are also waiting to see if President Joe Biden nominates him for another four-year term as Chair. Global markets were given some relief from their contagion fears about a disorderly collapse of China Evergrande Group after the country's central bank boosted liquidity in the economy. The indebted conglomerate issued a vaguely worded statement about interest due tomorrow on one of its yuan denominated bonds, saying an agreement with creditors had been reached without specifying how much interest would be paid or when. There also seems to be little risk for Wall Street banks, with Citigroup Inc., JPMorgan Chase & Co. and Bank of America Corp. all saying they had no direct exposure to the developer.  | The Democrat-controlled House approved a bill to keep the federal government funded past Sept. 30 and to suspend the debt ceiling for a year. Republican opposition in the Senate means the move is sure to fail when it reaches that chamber. While there still is no exact date for the government to run out of money, Treasury Secretary Janet Yellen it will happen "sometime in October." For investors, there remains the expectation that it will be sorted out, and lessons from debt standoffs in the past back up this view. The performance split between Asian and rest of the world equities continued for another session as fears about Evergrande contagion to Europe and the U.S. eased. Overnight the MSCI Asia Pacific Index slipped 0.7% while in Japan, where the central bank left policy unchanged, the Topix index closed 1% lower. Europe's Stoxx 600 Index was 0.6% higher by 5:50 a.m. with miners the biggest gainers on a rebound in metal prices. S&P 500 futures pointed to a relatively strong start to the session, the 10-year Treasury yield was at 1.328%, oil gained and gold was higher. U.S. existing home sales numbers for August are at 10:00 a.m. Crude investors are expecting a large drawdown in today's inventories data at 10:30 a.m. Brazil's central bank also announces it latest monetary policy decision today. The Food and Drug Administration may decide today on a recommendation for boosters made by Pfizer and its partner, BioNTech SE. President Biden will announce an order for 500 million doses of the Pfizer shot for the rest of the world. General Mills Inc. and BlackBerry Ltd. are among the companies reporting results. Here's what caught our eye over the last 24 hours. When the Great Financial Crisis hit over a decade ago, the Fed expanded its balance sheet dramatically. And a lot of people called this "money printing" but it didn't really result in much inflation. It's worth remembering why the effect was so mild. While it's true that the Fed created trillions of dollars of new reserves with the push of a button, it did so while removing Treasuries from private hands. As such, the financial position of the private sector was essentially unchanged. There wasn't new money sloshing around the system, chasing goods and driving prices higher. Lately, of course, we have seen elevated inflation, and we have a pretty good idea as to why. A lot of money was put into consumers' hands (through fiscal policy, not monetary) and at the same time, we've seen severe supply-side disruptions thanks to the pandemic. This combo of snarled supply chains, soaring demand for physical goods, and other changes to consumption patterns has given us the situation we find ourselves today. Basically it's got nothing to do with the reserves-for-Treasuries asset swap described above. This brings us to the debt ceiling, which everyone forgets about until we're reminded every few years of this silly law where Congress has to actively raise the amount of debt that gets authorized (a vote separate from spending) in order to avoid default. There's a simple way around this problem, and that's for the Treasury to mint a platinum coin (an option clearly spelled out in the law) and use that money to retire (buy back) U.S. federal debt currently being held by the Fed, reducing the total stock and providing breathing room under the debt ceiling. Of course, making money through the minting of high-denomination coins sounds weird and inflationary. But it only sounds inflationary for the same reason that people thought QE would be inflationary in 2009. As my colleague Ed Harrison puts it, you can think of the coin as a kind of Treasury QE. It would simply be an asset swap. The Fed is given a coin to hold on its balance sheet. The Treasury gets retired debt back. The effect on the real economy is marginal at best. There's no new spending. No new money chasing goods. Just different arms of the government making accounting changes. If you understand why QE wasn't inflationary in the wake of the GFC, you understand why the economic significance of the coin would be modest as well. Follow Bloomberg's Joe Weisenthal on Twitter at @TheStalwart Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment