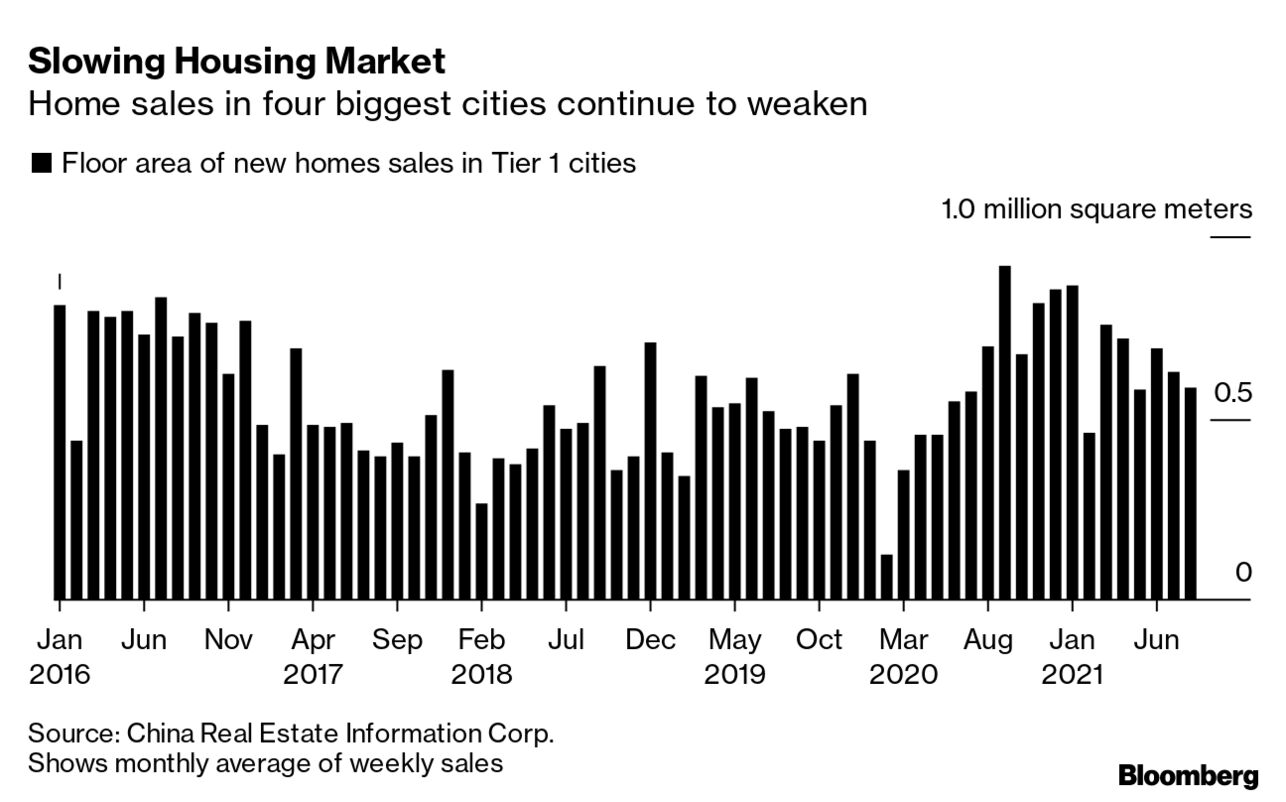

| China's crackdown on casinos threatens the future of Macau. Pfizer says the efficacy of its Covid-19 vaccine diminishes over time. The biggest package of U.S. tax increases in a generation takes a major step forward. Here's what you need to know this morning. China's casino crackdown is threatening to fundamentally transform Macau's identity. The resort city's top gaming stocks lost a record $18.4 billion in combined market value on Wednesday after officials said they would change casino regulations to tighten restrictions on operators, including appointing government representatives to "supervise" companies in the world's biggest gaming hub. The selloff continued among U.S.-listed casinos, too, with Wynn Resorts seeing its biggest two-day rout since March 2020. China's approach indicates a level of scrutiny not previously seen in Macau, which is the only place in China where casinos are allowed. Pfizer said that data from the U.S. and Israel suggest that the efficacy of its Covid-19 vaccine wanes over time, and that a booster dose was safe and effective at warding off the virus and new variants. The study comes just days after a panel of scientists from around the world said vaccines work so well, most people don't yet need a booster. Meanwhile, the number of people getting a first dose of Covid-19 vaccine is declining again in the U.S., and here's why the delta variant is surging among children.  | Asian stocks look set for a steady open after easing concerns about the economic growth outlook and a jump in energy shares bolstered U.S. stocks. Treasury yields advanced. Futures rose in Japan and Australia and were steady in Hong Kong, while U.S. contracts edged up. The S&P 500 posted the biggest jump since August, a dollar gauge slipped and oil rallied, with Brent crude scaling $75 a barrel. The progress of President Joe Biden's economic agenda is also a major focus for investors. The biggest set of U.S. tax increases in a generation took a major step forward on with approval by the House Ways and Means Committee of $2.1 trillion in new levies mostly focused on corporations and the wealthy. Australia is joining a new Indo-Pacific security partnership with the U.S. and U.K. that will allow it to acquire nuclear-powered submarines, likely signaling the end of its deal with France to buy conventional craft. Australian Prime Minister Scott Morrison, U.S. President Joe Biden and U.K. Prime Minister Boris Johnson announced the trilateral security partnership in a virtual meeting on Wednesday. The new framework comes as China expands its military presence in the region, though a senior U.S. official said it isn't targeting China or any other country. Almost every government in the world isn't doing enough to cut greenhouse gas emissions, making it likely global temperatures will rise beyond the tipping point of 1.5 degrees Celsius in coming years, a new report says. Scientists have said keeping the planet's warming within 1.5° C is key to staving off the worst impacts of climate change. Global emissions must be halved by 2030 to keep that target in sight, but governments are nowhere near that reduction, according to the nonprofit group Climate Action Tracker. Of the countries analyzed, only The Gambia has set ambitious-enough policies, the report said. This is what's caught our eye over the past 24 hours: China's real estate sector accounts for an estimated 30% of its gross domestic output. Per Travis Lundy, an independent special situations analyst who blogs on the SmartKarma platform, that is more than was seen in the U.S. before the 2008 financial crisis, and more than in Japan before the real estate bubble popped. Rebalancing a sector that's so important without causing outsized damage to the wider economy is inevitably going to be tricky. But it's tricky from a societal standpoint too, with Chinese homeowners more likely to protest falling property prices than spiking ones.  For years, the dominant path to financial security in China has been to scrimp together enough money to buy a house and then enjoy watching its value go up. If that's no longer the case, or if there's now a question mark over the certainty of that dynamic, it raises the question "what is the alternative?" I've previously described China's markets as resembling a great ball of money that tends to roll from one asset to another, be it stocks or bonds. There's a big pile of savings without an external outlet thanks to capital controls. Property has been a reliable destination for this excess money for a long time, and so we're left to wonder, what — if anything — might replace it? |

Post a Comment