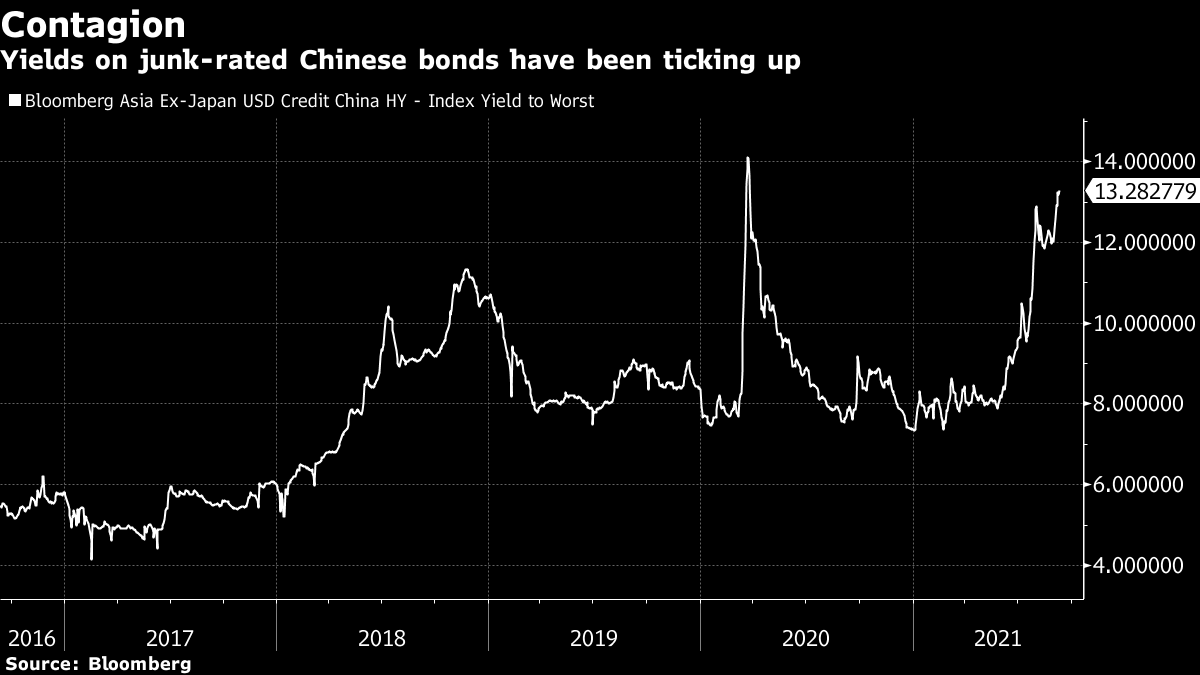

| Biden orders millions of workers to get vaccinated. China's got a new catchphrase. Ford shuts factories in India. What you need to know this Friday morning. President Joe Biden said he will order millions of government and health care workers to get vaccinated, with no option to opt for regular testing instead. In addition rules will be put in place requiring private employers with more than 100 employees to mandate shots or testing. And airline passengers who refuse to wear masks on flights will be hit with new heavier fines of up to $3,000. Meanwhile, a group of African and international organizations has warned that a proliferation of Covid-19 variants in Africa, partly attributed to the slow rollout of vaccines, could lead to mutations that complicate attempts to end the pandemic. Just 3.2% of Africa's 1.2 billion people have been fully dosed. Elsewhere, Singapore is hitting Covid-19 case levels not seen since the early days of the outbreak, but its high vaccination rate has helped contain hospitalizations and deaths; and thousands of Tokyo bar owners are rebelling against state of emergency rules. Here, we answer 12 of today's most pressing Covid questions. First it was "Common Prosperity", now Xi Jinping's government appears to have a new favorite phrase — the "disorderly expansion of capital" — which investors are trying to get their heads around. Since first appearing in a Politburo readout in December, the phrase has been employed by government agencies and researchers to explain actions against tech moguls, celebrities and private tutors that fueled a $1.5 trillion stock rout last month. The slogan, like "common prosperity," is among several Xi-isms feeding concerns that China is tilting away from free markets and back toward more ideologically driven centralized planning.  | Asian stocks look set for a steady start after a bout of weakness in global shares due to a slowdown in the pandemic recovery and the prospect of reduced central bank stimulus. Equity futures for Japan, Australia and Hong Kong pointed to modest gains. U.S. contracts fluctuated after the S&P 500 dropped for a fourth session, the longest losing streak since June, and the tech-heavy Nasdaq 100 retreated. Chinese technology stocks listed in the U.S. edged lower after a bruising tumble in Asia. Treasuries climbed amid the mood of caution and strong demand at a 30-year bond auction. A gauge of the dollar fell. In commodities, oil slid after China decided to tap crude reserves to ease a surge in energy costs. Ford will shut its car factories in India and record roughly $2 billion in restructuring charges, scaling back significantly in a country that past management saw becoming one of its three biggest markets. Manufacturing of vehicles for sale in India will stop immediately, and about 4,000 employees will be affected, the carmaker said in a statement. Meanwhile, over at Apple, the software chief in charge of the Watch has taken over as head of the company's self-driving car project, after its previous leader went to Ford. For all the latest news on the future of the world's car industry, check out Bloomberg Hyperdrive. American firms in China are hoping for a meeting between Presidents Joe Biden and Xi Jinping this year, according to a new survey, as they look for relief from trade barriers raised during the Trump era. More than 60% of American Chamber of Commerce in China members surveyed cited the need to restore regular visa services for business executives and their families, according to a survey released by the group Friday. Another 47% wanted the removal of tariffs, with more than three-quarters of companies complaining that measures levied during the trade war were impacting their operations. But don't hold your breath for a U.S. visit by Xi just yet. He hasn't set foot outside China for 600 days. This is what's caught our eye over the past 24 hours: A spike in yields on junk-rated bonds and multiplying crackdowns have lots of people talking about the possibility of a "Lehman moment" in China, one in which regulators would allow a systemically important bank or property developer to fail. That seems extremely unlikely. There's now reams of analysis pointing out the extent to which Lehman crushed financial markets in 2008 by sparking a liquidity crisis that infected most other banks. Letting Lehman go allowed the financialized economy to infect the real one, creating the great recession which took the U.S. years to climb out of. In the two decades since then, we've seen multiple examples of authorities scrambling to avoid another Lehman. Yields on eurozone government bonds hit records before bailouts were handed out. Greek government bonds now yield less than 1%. Yields on U.S. junk-rated debt also jumped in the sell-off of March 2020. They are now at their lowest levels since the late 1990s after the Federal Reserve unveiled a corporate bond-buying program.  All of which is to say, that the tendency in the aftermath of Lehman Brothers has been towards supporting existing financialization rather than letting it go altogether. Authorities have been willing to stomach more financialization to avoid allowing the financial sector to infect the real economy once again. Or as Viktor Shvets over at Macquarie puts it: "There is a strong argument that deep financialization reduces long-term growth and amplifies inequalities and disinflation. True, but consequences on demand and credit of reversing or even slowing financialization will be devastating — medicine worse than the disease. China was late to appreciating this, but it is now onboard with 'managing risks.'"

The tradeoff for accepting more support of the financial sector is financial repression and a steady march lower in returns for investors as they struggle to put money to work. But it's far more appealing than the alternative. |

Post a Comment