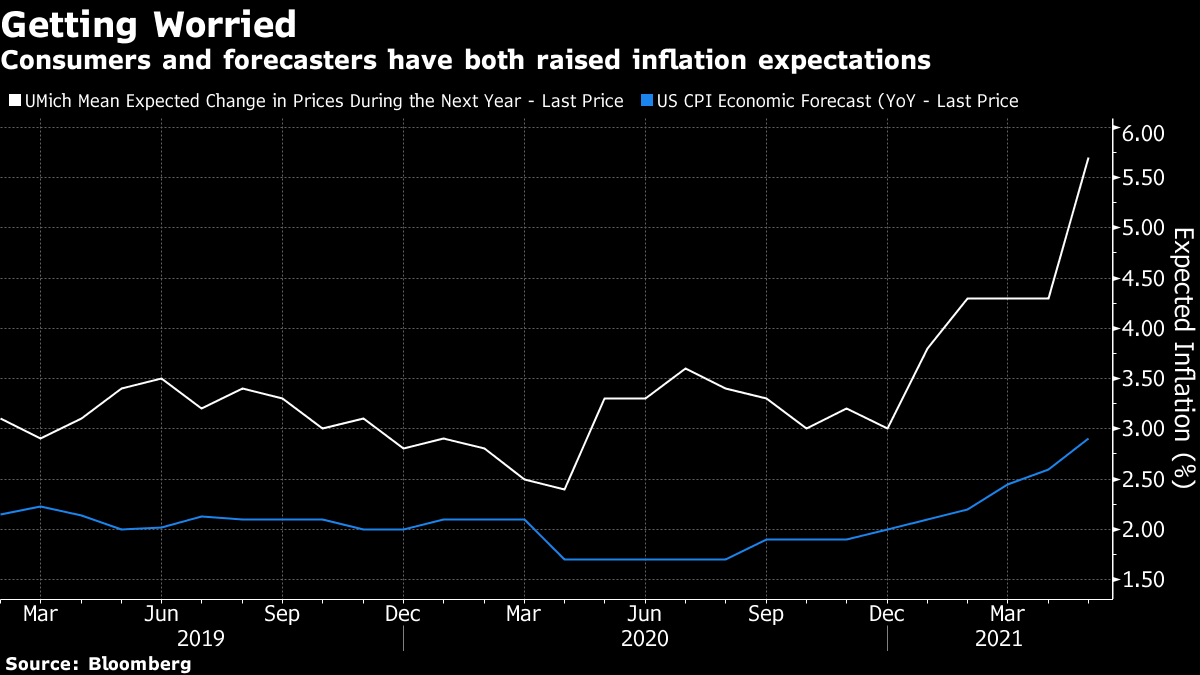

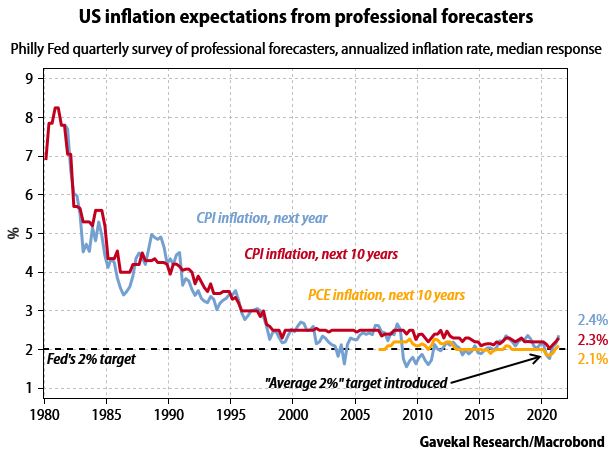

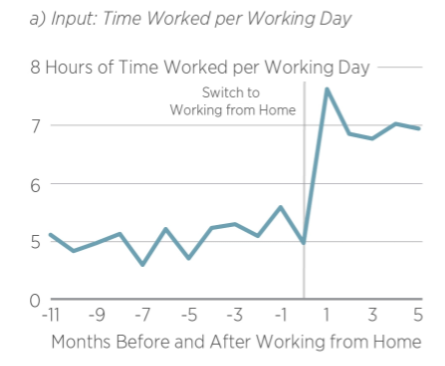

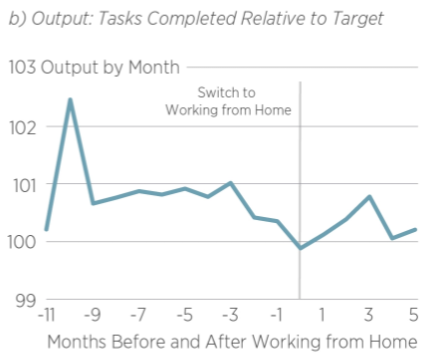

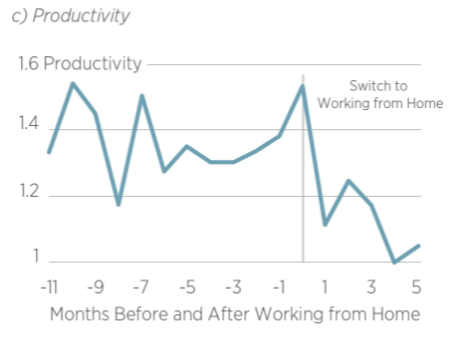

What to Expect When You're Expecting (Inflation Edition)What exact measures should we hold on to when building forecasts for inflation? And how much care do we need to take over the issue of reflexivity? In inflation, as in many other areas of economic life, perceptions can form reality, and that is certainly true of inflation. That is why the Federal Reserve wants to see expectations "well anchored." The best version of market predictions is derived from the breakeven rates between inflation-protected and fixed-income Treasury bonds. On that basis, we see the outlook for the next five years is continuing to tick up to a new high for this cycle of 2.77% — but expectations for the five years after that have dipped slightly, to 2.35%.  Breakevens change every day, though the numbers from the bond market do suggest investors still think inflation will stay broadly under control over the coming decade — with, presumably, some tightening from the Fed down the pike. More discomfiting for the Fed are the data that come from opinion surveys, of consumers and of professional forecasters. These projections haven't been tested in a market, but they have the ability to form their own reality. The University of Michigan monthly survey of consumers' expectations perennially shows shoppers foreseeing more inflation than will in fact arrive. The important factor here is the direction of travel — if they are more worried about inflation, they will do more to guard against it, which will tend to push up prices. Meanwhile, experts' forecasts, relatively isolated from the hurly-burly of markets, have been relatively laid back. Economists have consistently suggested that inflation will stay under control. This means the latest forecasts for the next year from the Michigan survey, and from Bloomberg's own survey of professional forecasters, could come as unwelcome reading:  This does look as though inflationary psychology is being jolted back into life. The Fed wants this to happen to a certain extent, as it is trying to breathe more life into the labor market. But not to the extent that it loses control of the narrative. One final measure of expectations comes from a quarterly survey conducted by the Philadelphia Fed. It polls well-known economists on their expectations for both CPI and the less widely quoted PCE measure of inflation, which is the Fed's favorite target, and which tends to be slightly lower than CPI. Again, this survey is unwelcome, albeit not terrifying reading. The chart comes from Gavekal Economics:  At one level, this chart is a monument to the success of Paul Volcker. The legendary Fed chairman of the 1980s successfully convinced a generation of economists that U.S. inflation wouldn't be allowed to get out of hand again. But the sheer stability of the last two decades commands that even the slightest shift upward be taken seriously. These numbers suggest the Fed is convincing the world that it really will allow the economy to "run hot" for a while; but also that it is running a risk of re-establishing inflation psychology again. (To be clear, this chart also shows that there is a long way to go before we return to anything like the psychology that greeted Volcker). So, has the Fed got it wrong? Now that bond traders, consumers and economists are all worrying about inflation more than they used to, should the Fed be a little more concerned? These are exactly the questions I will be attempting to answer on a live blog on the terminal tomorrow at 10 a.m. New York time, with brilliant colleagues Jack Farchy and Lisa Abramowicz, under moderation from Kriti Gupta:  The discussion will go on for an hour. We'll take questions during the conversation, but email any in advance to: TopLive@Bloomberg.net. Once on the terminal you have to search for this not-very-easy-to-remember address: TLIV 609D2041B2200000. I'll hope to see you on the terminal, and for those who don't have access I'll write up the main conclusions in tomorrow's Points of Return. Working From Home, Part IHow do we all feel about working from home? It seems to me that sentiment swung strongly in one direction in the first weeks after the pandemic hit western Europe and North America, as people realized it was much easier than they had expected. A year on, we can still see that it's a more valid option than previously thought, mainly thanks to technology. Even so, any ongoing changes to work culture will be somewhat less radical than people seemed to think 12 months ago. Bloomberg's office is still barely a quarter full, though it's noticeable that people are very happy to be back. That might shift a bit when and if New York returns more fully to normal and commuting becomes more unpleasant again. But for now the advantages of being in a dedicated office, in which you can compartmentalize the part of your life dedicated to work, and where you have chance interactions with people who can help you, seem overwhelming. There's also some empirical quantitative evidence that working from home isn't terribly productive. The University of Chicago's Becker Friedman Institute produced this interesting report on an unnamed Asian tech company, which switched all its employees (more than 10,000 of them) to WFH in March last year. The charts tell the story clearly enough. People at home tend to spend more time working:  However, they don't tend to get any more done. Indeed, after an initial surge, if anything they accomplish less than in the office:  Therefore, productivity fell. I doubt this will surprise anyone by this point, but here are the numbers as calculated by the Becker Friedman Institute. Productivity took a serious initial hit, recovered a little as people began to adapt to their new circumstances, and then fell further. Five months into the WFH era, employees' productivity had dropped by about 20%. For most, work had eaten up more time than they had saved by abandoning their commute:  The output numbers are based on the primary goals set for employees by the company's internal analytics, which were also able to break down how much time employees spent in different activities, separating out calls, conferences, and periods of uninterrupted work. These findings aren't based on self-assessments (although they agree with the self-assessments that most people I know would make), and they concern a workforce of generally well-educated and highly skilled people, doing jobs that require a college degree. Such modern white-collar jobs were supposed to be just those that could be transposed to the home environment most easily. And yet productivity still tanked. What went wrong? Employees spent more time engaged in various types of formal and informal meetings during WFH, especially video conferences. Likewise, they spent substantially less time working without interruption. They also spent less time networking (both within the firm and with clients), and less time receiving coaching or 1:1 meetings with supervisors... The authors also found that the productivity of women was more negatively affected by WFH than men. However, this gender difference was not due to the presence of children in the home. Rather, the likely culprit is other demands placed on women in the domestic setting. Employees with children at home increased working hours significantly more than those who did not have children at home, accounting for a greater decrease in productivity.

After the initial pleasant surprise that working from home was as easy as it was, I suspect these findings ring true for many of us. More flexibility to work from home is in our future, and those suffering from a streaming cold are going to find it much easier to persuade their supervisors to work from home. But some of the bigger predictions of a change in the nature of work that were being made a year ago are beginning to sound less sensible, at least to me. Companies that produce communications technologies will redouble efforts to improve their offerings, and come up with a way to replicate the random discussions that only happen in the office and are so valuable. Working From Home, Part IIGetting back to the office isn't just about productivity. It's also about risk management. We're much less likely to take stupid risks if we communicate with each other effectively. It's when you bump into someone you weren't planning to talk to that you might just get talked out of doing something dumb. The latest newsletter from Whitney Tilson of Empire Financial Research includes this interesting nugget. It's only an anecdote, but it rings true: A friend who knows a number of the fund managers who've blown up in the past year made an interesting comment to me recently… He speculated that these blow-ups might not have happened had the portfolio manager and his team all been in the office together every day, as they were before the pandemic hit. Maybe someone would have identified the ballooning risks and stuck their head into the portfolio manager's office for a talk that could have averted disaster… It's an interesting theory – and one that has broader implications for all sorts of businesses, especially professional services like investment banks, law firms, and even my own company. It has definitely been more of a challenge to manage and build the culture of Empire Financial Research when our team has only been together in person a handful of times over the past year. That's one reason we're all looking forward to a retreat next month!

Archegos Capital Management, the most alarming and costly of this year's blow-ups, suggests that the Volcker Rule (which stops banks from speculating with depositors' funds) has been diluted too far. As a former head of the Federal Deposit Insurance Corp. argued for Bloomberg Opinion, the decision to exempt family offices from much of the reach of the rule looks already to have been a mistake. Some huge fortunes are now being run as family offices, and they are taking big risks. It's not just Archegos. If each of the banks lending money to Archegos had known how many others were doing the same, greater conservatism would have ruled. But even without tighter formal disclosure rules, and without tighter limits on what big banks can invest in, working from home may have contributed to the problem. People in Wall Street and the City of London and other financial centers used to talk to each other. Not just to their colleagues, but to counterparts at rival firms. It came naturally with the territory of commuting into a central business district every morning. This brings problems with it, such as groupthink. Big financial centers can foster the inflation of big asset bubbles. But we've learned in the last year that groupthink can flourish even more in cyberspace. Best not to work on the assumption that white-collar workers will be doing all their work from home from now on. Survival TipsCompetition is wonderful. It makes the world a better place. I always welcome it. And just to prove that I mean it, let me recommend a new daily newsletter on markets and investing, FT Unhedged by my former colleague Rob Armstrong. You can read the first edition here, and subscribe to get it in your inbox here (you'll need a premium subscription to the Financial Times). If you subscribed to my old newsletter from my years at the FT, and never unsubscribed, it should already have arrived in your inbox. I hired Rob almost exactly 10 years ago, to write for the FT's revered Lex column. He subsequently succeeded me as the head of Lex, and it's great that he's now also following me into the exhausting business of lengthy daily newsletters. Along the way, he found the time to branch out to become the FT's New York correspondent on fashion, one subject on which his opinion is indisputably more valuable than mine. In all seriousness, I think all Points of Return readers should check it out. And henceforward I will enjoy channeling my inner Jeff Bezos and remorselessly crunching FT Unhedged under foot like a bug. I love competition, but there are limits. Good luck Rob, you'll need it. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment