A Crypto-WeekendBitcoin never sleeps, or at least it doesn't take weekends off. It also has a strong tendency for dramatic moves on a Sunday. Here's what happened since the beginning of last week:  At one point, bitcoin was down 20.3% from its peak just before Coinbase Global Inc. started trading Wednesday. It's hard to believe the share debut had nothing to do with the decline. By far the biggest cryptocurrency exchange to go public, Coinbase immediately started to give ground after finding a price, and took bitcoin with it. This is a screengrab of Coinbase shares and bitcoin on Wednesday afternoon:  Coinbase is a big moment for the emerging crypto world. Many of those sinking money into the stock are the same people holding (or hodling) bitcoin. By Friday's close (the stock market sleeps on weekends even if crypto assets don't), Coinbase had shed 10% from its opening price, and 20% from its short-lived peak. It remains worth $68 billion, roughly the same as Colgate-Palmolive Co., and slightly larger than Intercontinental Exchange Inc., which owns the New York Stock Exchange among others. That is a remarkable badge of approval for the crypto-financial system. This could be a problem. Peter Atwater, of Financial Insyghts, points out that commentary surrounding Coinbase has been almost all about legitimacy and the notion that the crypto world has received an endorsement, rather than about growth, or fears of overheating. Here are comments he highlighted, with his own critique: - "With acceptance from traditional investors, a profitable start-up that eases transactions is offering proof of the industry's staying power."

- "It's going to legitimize a lot of what these companies are doing," Marcus Swanepoel, CEO of London-based crypto platform Luno, said of the Coinbase debut. "For one, it's going to show just how big the industry is and how much it's growing."

- [Coinbase CEO, Brian] "Armstrong also said that he hopes their public debut would legitimize the crypto space and would make people realize that the cryptocurrency ecosystem is growing to become an integral part of the financial ecosystem."

What was so striking to me about the messaging around this week's celebrity offering was the demand that the company be taken seriously. Company leaders, analysts and sponsors were all clear. The cryptocurrency space has matured. It no longer deserves to be seated at the kiddie table at Thanksgiving. Coinbase needs to be viewed in the same light as the New York Stock Exchange, the CME and the Nasdaq.

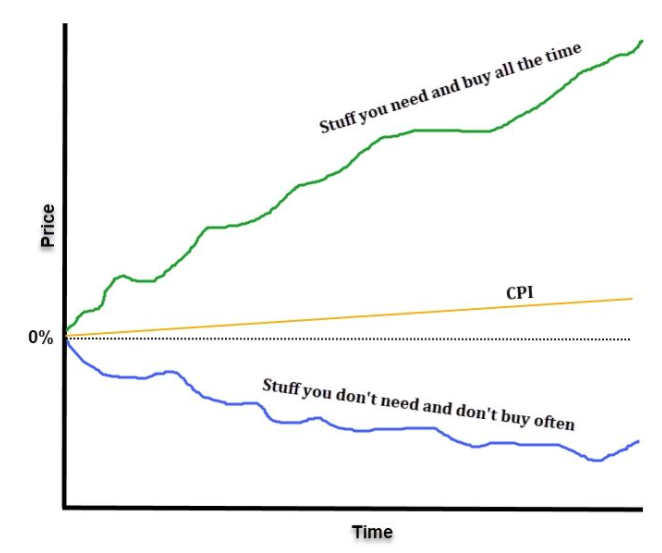

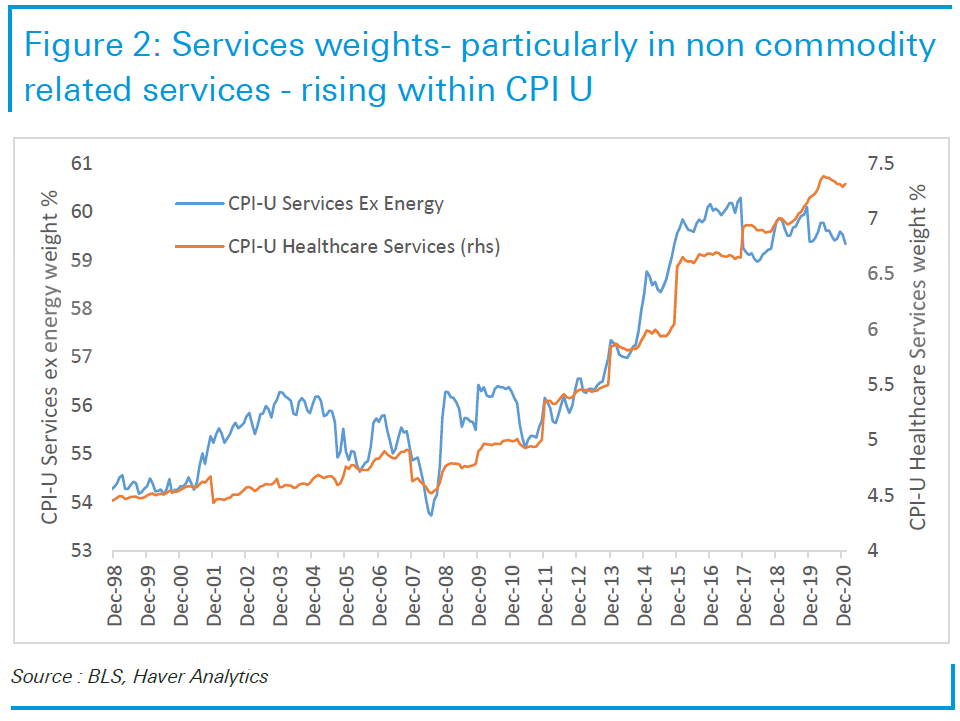

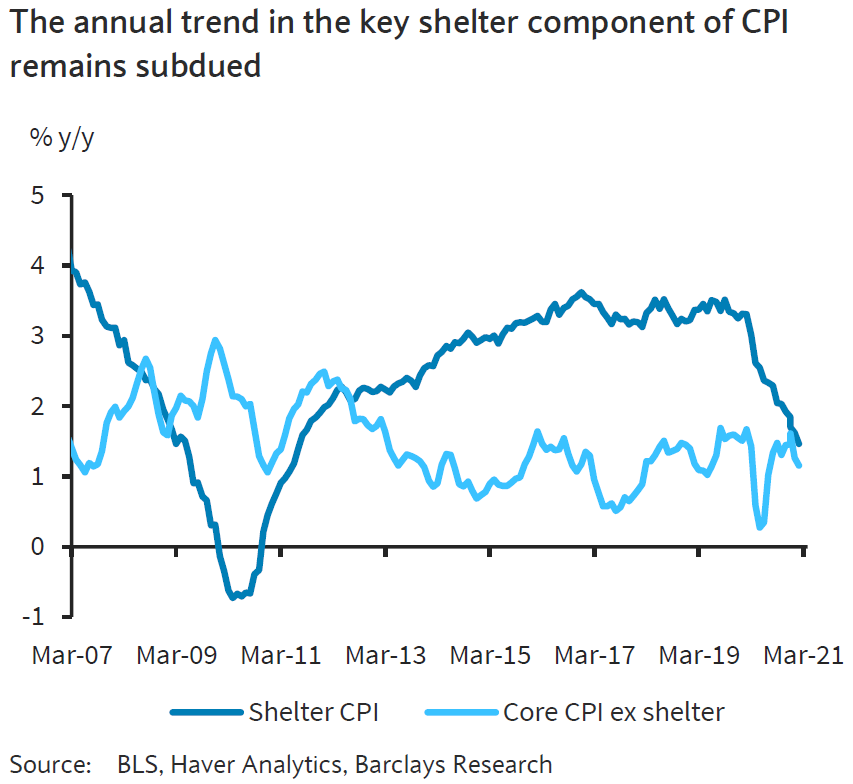

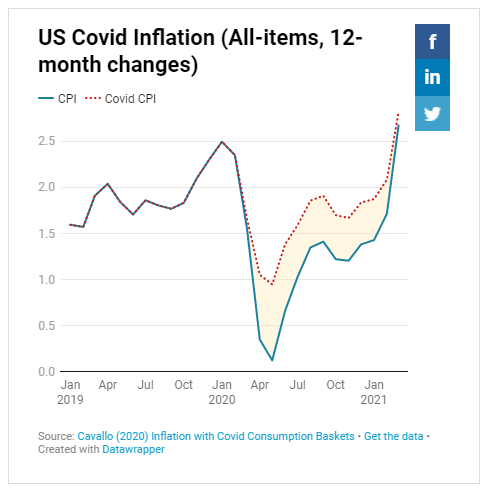

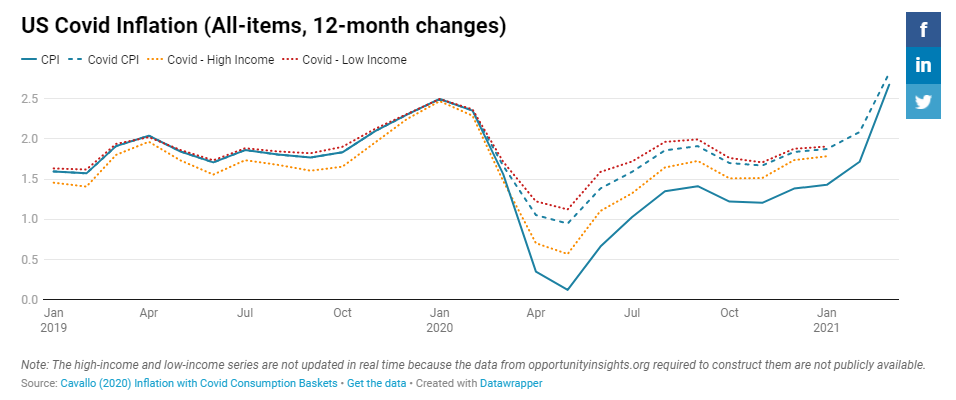

Why should this be a problem? Because when the most exciting thing to be said about an investment is that it has matured, the chances are that the excitement is over. As Atwater puts it, this is the kind of talk that comes "AFTER the peak is in." And if Coinbase wishes to be compared to the NYSE, the CME or the Nasdaq, it faces a problem because all those companies trade on much lower earnings multiples. When it comes to bitcoin itself, Atwater draws a comparison with gold miners and gold. "When picks and shovels are being touted as your best bet – rather than the gold mine itself – the rush is past." The same applies to buying crypto-exchanges rather than the digital assets themselves. Bitcoin has formed bubbles, suffered slumps, and rebounded before. It may soon have to repeat the feat. Meanwhile, a big crypto selloff can be expected to create a significant headwind for broader tech stocks, This is how Coinbase and the Nasdaq moved on launch day last week:  This does, then, look like a climax moment for crypto excitement. It would be wise, however, to assume that bitcoin could still rise again. A 20% fall in a few days for an asset whose total worth is more than $1 trillion certainly matters; but in the context of bitcoin's past experience, this isn't so remarkable. It barely brings the price back to its 50-day moving average, a good measure of the short-term trend. If we look at the last five years for bitcoin, on a logarithmic scale, this weekend's excitement isn't visible:  It might be time for crypto to take one of its habitual downdrafts. That could mean a lot of people will lose money. But it isn't the same thing as predicting the demise of crypto assets. The Deflating Reflation TradeIf bitcoin looks as if it might have peaked, the same might be said for the reflation trade that has dominated markets this year. Last week's economic data validated the notion that this rally is special — yet it was accompanied by a big move away from betting on reflation in bond markets. In the short term, that helped stocks, as it meant lower rates. But is it really correct that we can now forget about inflation? Naturally, that is too big a claim to make. We need far more evidence. But that doesn't mean we shouldn't discuss it. So, on Tuesday, at 1 p.m. New York time, Bloomberg will hold a conversation between myself and Bloomberg Opinion colleague (and much else besides) Mohamed El-Erian at TLIV <GO> on the terminal. Fire any questions to me or to Kriti Gupta, who will be moderating, at kgupta129@bloomberg.net. For ideas, you might try El-Erian's most recent piece on inflation for Bloomberg Opinion, or this piece on the dilemma for central banks, which brings forward arguments from his 2016 book, The Only Game in Town. That argued that central banks were left trying to do too much heavy lifting because of a failure of other economic institutions. I've tried to air as many views as I can in this newsletter over the last few months; maybe the most important are this one, on the possibility of a new inflationary regime, and this one on the role of demographics. If you think the debate should go in any different directions, let us know. A Matter of Measurement One key topic is the belief that the official numbers are wrong. This can come from distrust in government institutions; from a belief that the data-gathering is fixed to make inflation look lower than it is; or a suspicion that the "basket" of goods and services in the index has been politically fixed for the same purpose. Even among those who don't believe in direct political malfeasance, there is a persistent belief that inflation is more prevalent than the figures show. One chart I found on LinkedIn captures the widespread perception perfectly:  Compiling inflation numbers from raw data is difficult, and way above my pay-grade. So I tried talking to one of the acknowledged authorities on the subject, Emi Nakamura of the University of California, Berkeley, who won the 2019 John Bates Clark Medal, given annually to the best U.S.-based economist under 40, for her empirical work on inflation. You can find an audio interview I did with Nakamura three years ago here. Her work tends to involve sifting through what most of us would regard as intimidating amounts of data, to try to get at the mechanics of why prices go up, and how they can be aggregated into a meaningful measure of inflation. So, does the stylized picture in this chart accord with reality? Nakamura argues that it doesn't, because it misunderstands what is meant by inflation. Arguably, the greatest measurement problem is to take account of improvements in quality. An iPhone is a classic example. The cost of an iPhone goes up over time, but each new model displaces more gadgets. If you compare the cost of an iPhone with the cost of a GPS system, a phone, a Palm Pilot, a camera, a stopwatch, a calculator and so on, you can quickly arrive at the notion that we are in deflation. The strongest arguments that inflation is understated in the U.S. concern the cost of healthcare and higher education, both of which seem to rise ineffably. Or at least, the amount we spend on them rises each year. That is the critical issue. The question Nakamura asks is: "Would you rather go back and get the healthcare of 25 years ago, for the prices of 25 years ago, or take what is on offer today?" In many cases, you would take the latter. Procedures and medicines improve. Americans may pay much more for healthcare than they used to do, but that doesn't mean there has been inflation in prices; it means that providers have persuaded Americans to pay for new and more expensive products and services. Similar arguments apply to higher education. Elite universities and colleges appear to be in an arms race to provide new and better facilities, which justify (or arguably require) higher fees. With a college education now perceived to be more important than it used to be for career progression later in life, a higher price becomes justified for what is effectively a product of higher quality. And plenty of improvements have been made that make the service better, even if it isn't necessarily more valuable. Certainly, when I've returned to my alma mater, the improvement in facilities over the intervening three decades is breathtaking. Whether it really makes student life any better or happier is questionable — but we can say that about plenty of things that are now much improved. A further consideration is that the baskets of goods in consumer price indexes aren't static and shift over time in response to changes in spending habits. As this charts from Barclays Plc shows, the weight of services such as healthcare is indeed steadily increasing:  Housing and Inflation Another complaint is that inflation figures take no account of the rising cost of housing. This one seems pretty important given the well-documented intergenerational tensions it is creating. If twentysomethings find themselves with no choice but to return to the parental nest because housing is too expensive, then surely inflation numbers should reflect this? Again it's not that simple. "If you live in a house and its price goes up," says Nakamura, " you could say that the cost of your housing is actually negative. You could make money as though you had been paying negative rent." This leads to the impenetrable notion of the "owner equivalent rent," which measures the implicit cost to rent housing. But the bottom line is that in recent years the inflation in shelter costs has come down markedly, as again demonstrated by a Barclays chart:  Inflation and Inequity But isn't it true that costs for the poor have increased more than those for the wealthy? This is another enduring belief, strengthened by Covid-19. It has a strong element of truth. Nakamura points to the work done by Alberto Cavallo of Harvard Business School on "Covid inflation," which used data from credit and debit card receipts to take account of what people actually bought during the pandemic. If the CPI basket had been weighted this way, inflation would have followed the red line in the chart below — significantly higher than the official number for several months last year, but with the gap now almost closed:  On Cavallo's estimate, Covid did cause more inflation for the poor than the rich. But while the effect is clear, it isn't that big:  As of January, Cavallo's estimate was that Covid-adjusted inflation was 1.78% for the wealthiest and 1.9% for those on low incomes. Importantly, the official data are public, so anyone armed with a computer and some spreadsheets can calculate what different inflation rates would be if we assume that people buy different baskets of goods. Survival TipsBaseball is back, including even my son's little league, which suffered cancelation last season. Little league baseball is all the better if you've missed it for a year, and if it takes place against a bucolic backdrop of springtime, with daffodils and cherry trees in blossom. That said, baseball has one problem; the action can be a tad slow (and I say this as someone who was brought up on cricket). This brilliant video demonstrates that you can fit the entire Kentucky Derby between two typical pitches, in this case delivered by former Cy Young Award winner Zack Greinke. In the time that nothing at all happens in a baseball game, you can run the biggest horse race on the calendar. Yes, it would be a good idea to speed up the action a little. In this regard, the professionals could learn something from the little leaguers, who are hard to restrain. Have a good week, everyone. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment