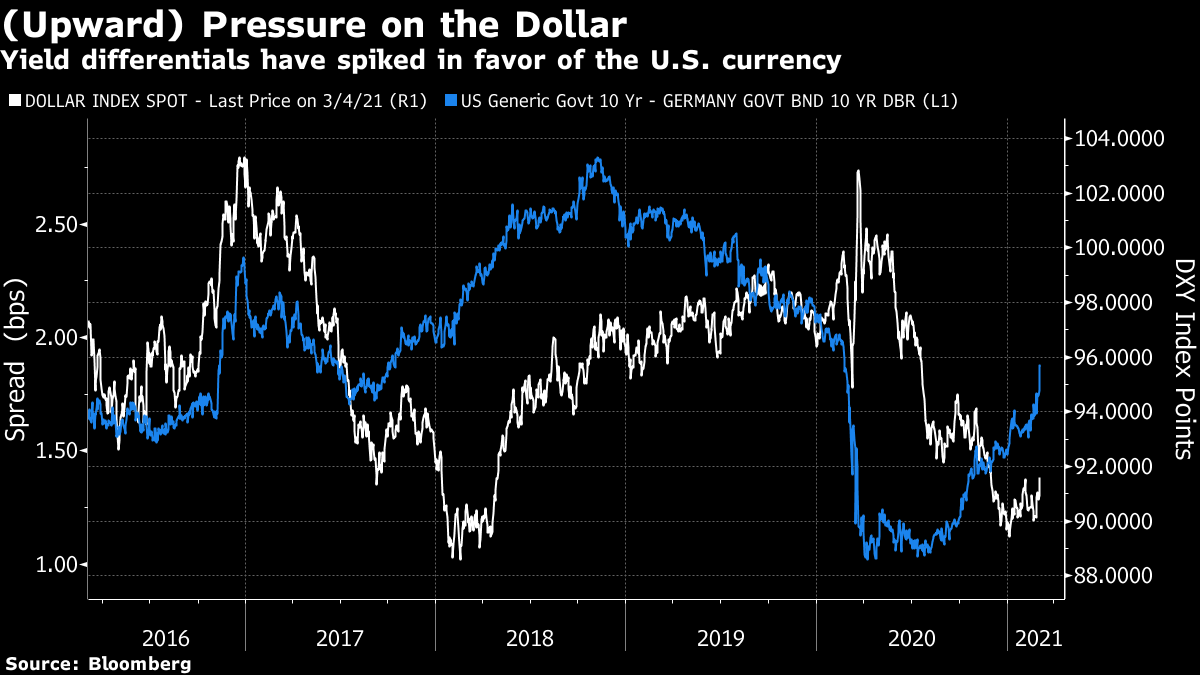

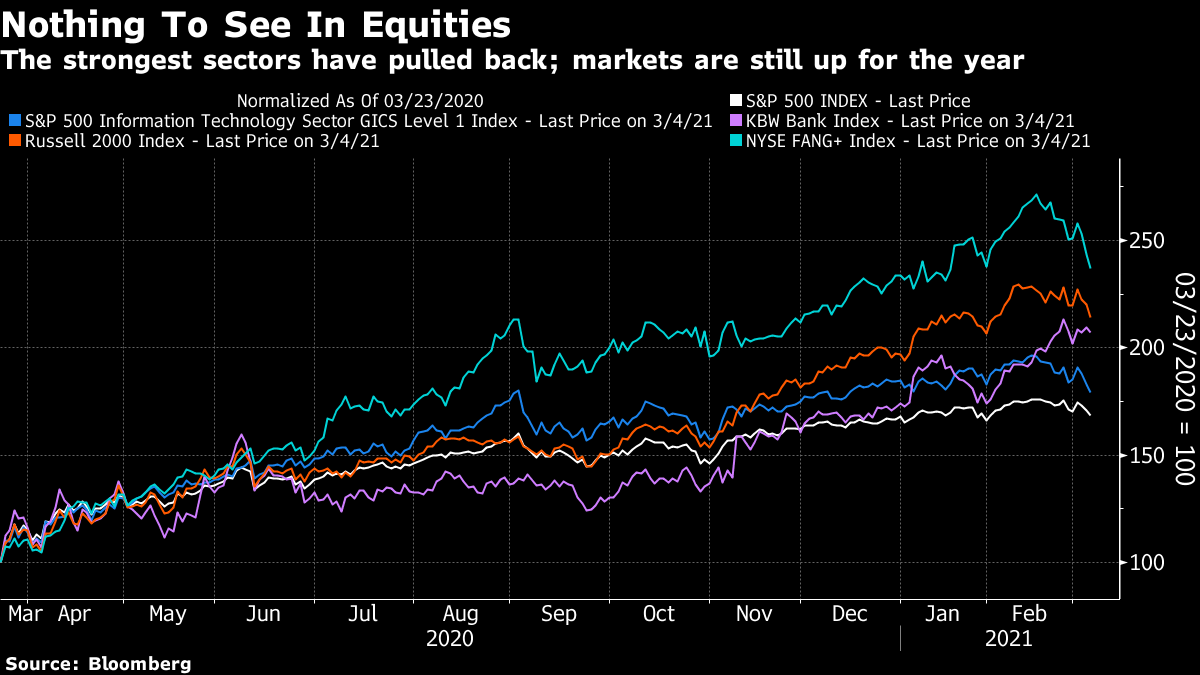

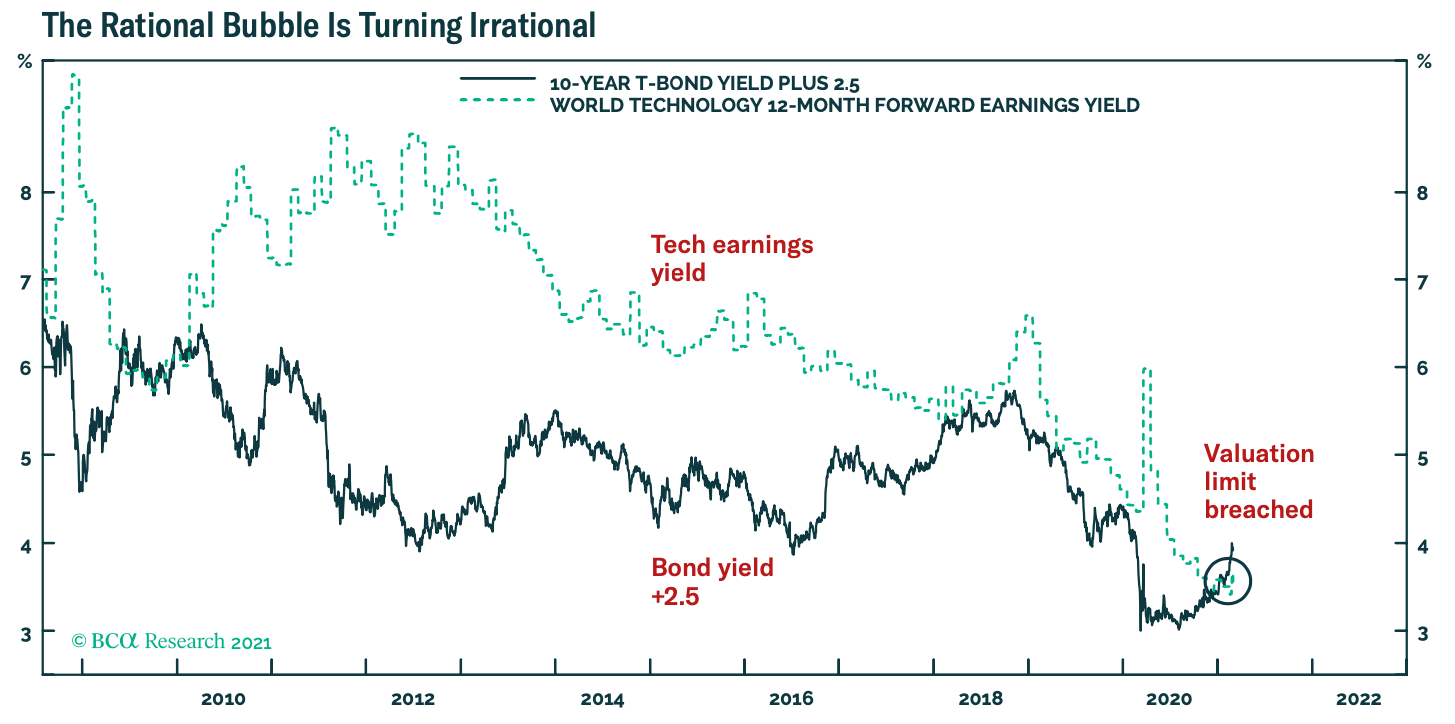

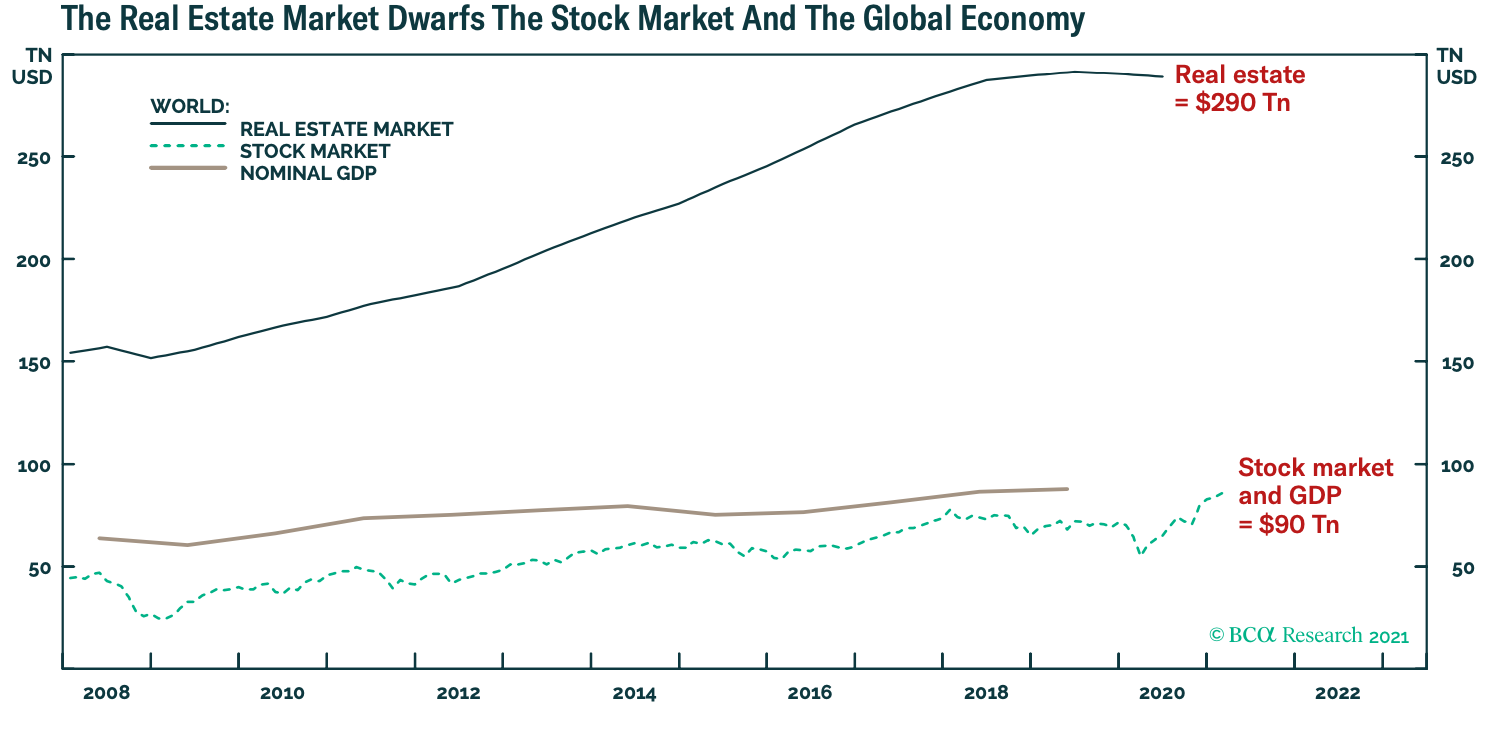

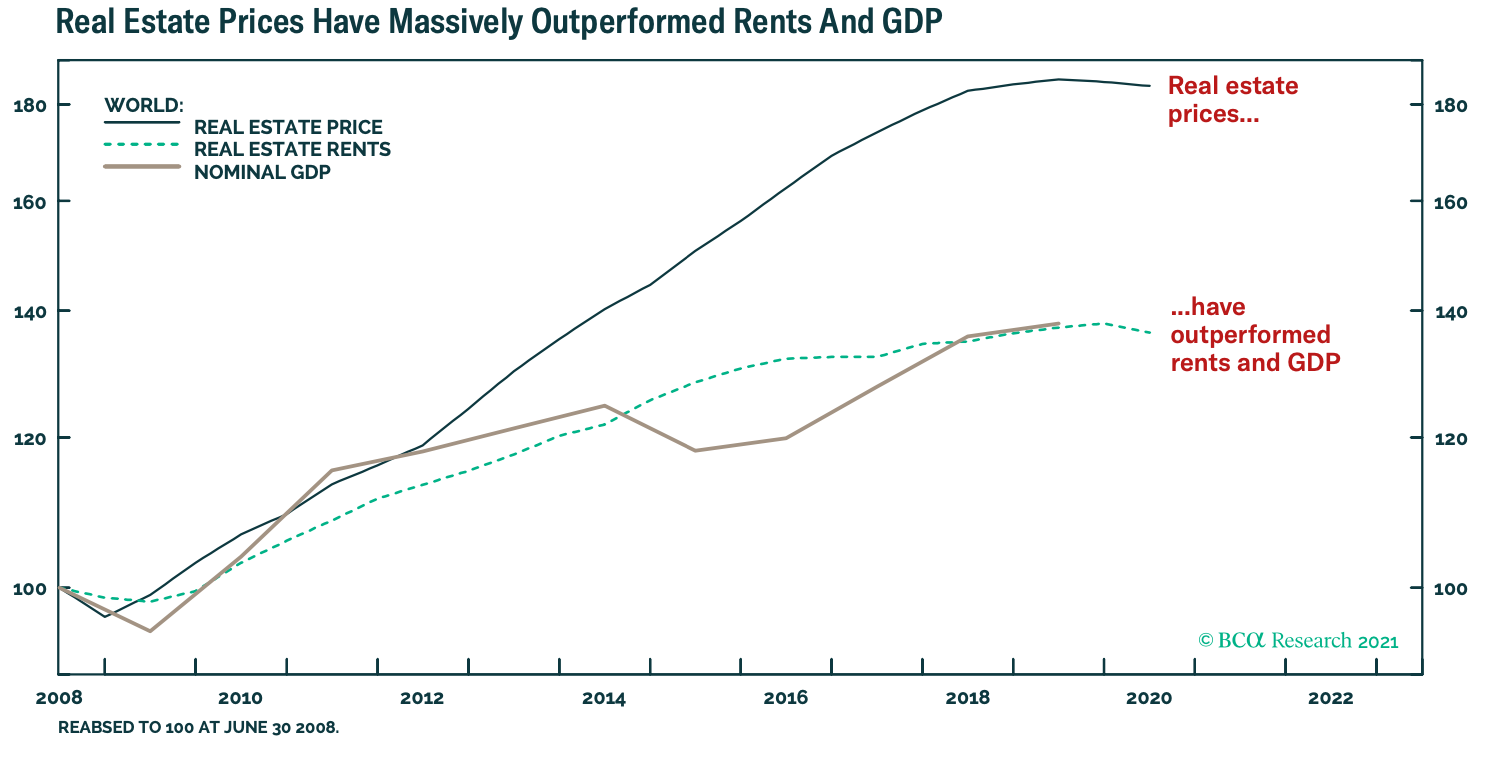

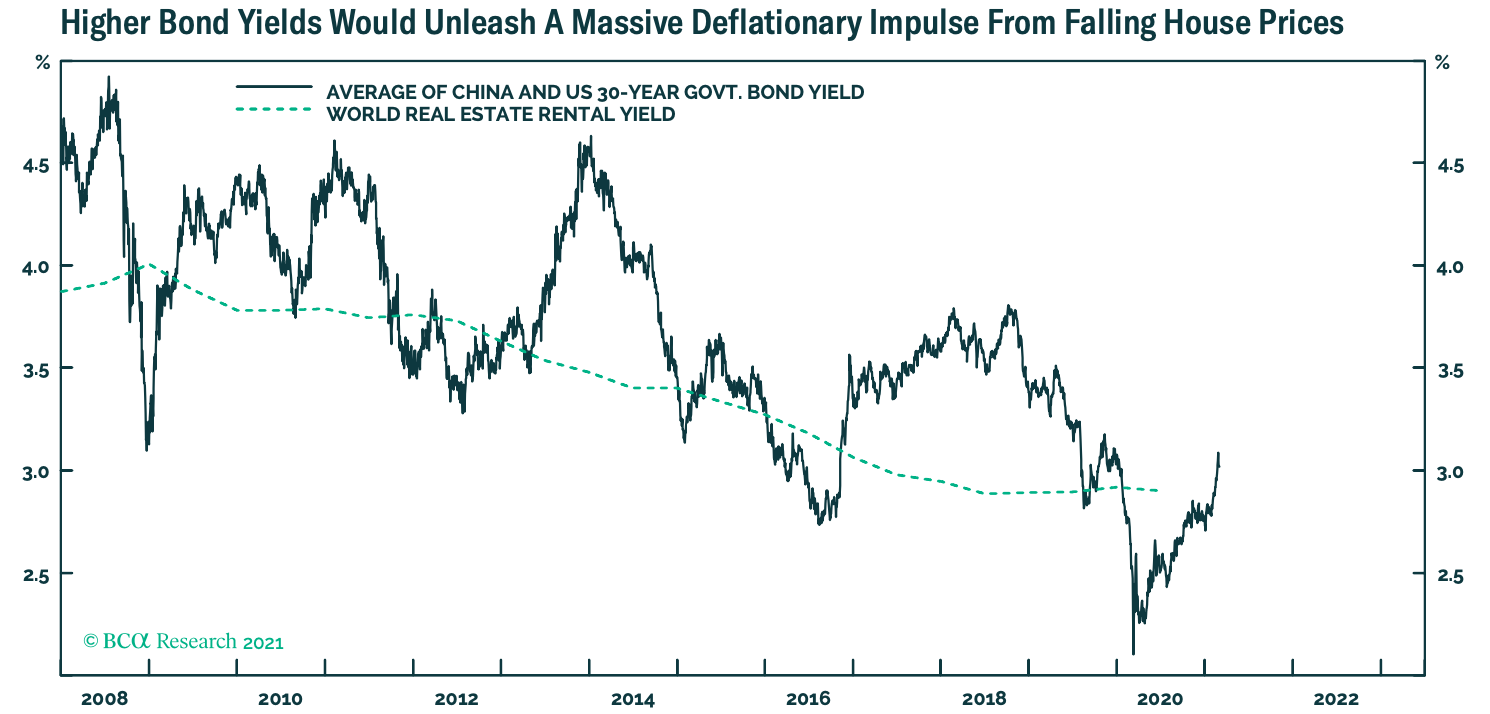

Words UnsaidIt appears that investors wanted Jerome Powell to say something else. "Stock Market Momentum Comeuppance Gets No Sympathy From the Fed" read the Bloomberg News headline after the Federal Reserve chairman spoke to a Wall Street Journal webinar. He echoed the Fedspeak we have heard over the last few days, saying the recent rise in bond yields was "something that was notable and caught my attention." But beyond repeating what is obviously an agreed form of words, he made no hints as to what the Fed might do about it. That wasn't good enough for the market, which wanted something specific. Thus, to quote my former colleague Krishna Guha, now vice chairman at Evercore ISI, Powell "stayed dovish but not dovish enough to prevent further increases in yields." Stocks also had another bad day. The Nasdaq-100 index is now down slightly for the year, and some gauges of tech stocks have fallen 10%, fulfilling the popular definition of a correction. Thursday's biggest development, arguably, was a surprising strengthening of the dollar. The popular DXY index, which compares the greenback to a group of the largest developed market currencies, is now above its 100-day moving average for the first time in 10 months, suggesting that the trend is turning. Meanwhile, the bond market is applying more upward pressure. Generally, as the chart shows, rate differentials tend to lead currencies, with a lag, and the spread of U.S. over German 10-year bond yields has risen sharply. If the dollar continues to rise, a widespread market assumption will have been thwarted. And the stronger currency will itself act as a counterweight against the inflation predicted for the U.S.:  Within the stock market, the rotation toward a new regime grows ever clearer. Bloomberg's FTW function measures the pure returns to each of a variety of market factors, when all others are held constant. The following chart shows the performance of value relative to momentum in the U.S. market. Value stocks (which look cheap compared to their fundamentals) had another great day, while the companies that previously had momentum stalled. All the move away from value driven by last year's pandemic has now been reversed. The market is clearly repositioning for companies that will prosper in a reflationary environment, and leaving those that prospered under pandemic conditions:  But while the rotation is quite dramatic, the shift in the stock market's overall value is not. The S&P 500 is still up since the start of this year and has barely declined. Previously dominant tech stocks have pulled back marginally and the FAANG internet platform companies have been trimmed back, while the Russell 2000 smaller companies index enjoyed quite a rally that is now evening out. In all cases these look so far like reasonable and minor corrections after a phenomenal surge since the pandemic low on March 23 last year. Remarkably, bank stocks have now outperformed tech stocks since last year's low:  The Fed appears to be treating the stock market as its measure of whether bond yields have risen too much. If rising yields spark a significant equity selloff, as happened at the end of 2018, it's fair to expect that the Fed will respond with extra support for the bond market. But not before that. At what point could that be reached? Dhaval Joshi, European equity strategist for BCA Research Inc., offers the following analysis. Tech is now a huge part of the stock market. In the post-crisis decade, he points out, the earnings yield (inverse of the price-earnings ratio) of the global tech sector has always been at least 2.5 percentage points higher than the 10-year Treasury bond yield. Lower bond yields, up to a point, do justify higher equity valuations. But that limit has now been clearly breached.  At this point, investors assume they will need an equity selloff to elicit any more support from the Fed for bonds. And they have reached a point where a further equity selloff would make sense. With the next meeting of the Federal Open Market Committee two weeks away, their resolve to test the Fed is now itself being tested. What Could Possibly Go Wrong? (Real Estate Edition)The excitement over rising yields and reflation has brought an analytical backlash. Both Albert Edwards, the famously bond-bullish and stock-bearish investment strategist at Societe Generale SA, and Joshi of BCA Research produced notes suggesting that the low for bond yields isn't yet in. In other words the deflationary slump has yet to run its course, and the rise in yields will itself provoke a final downswing. Edwards warns that "by going all in on that bet now, investors have likely gone too big, too soon, and are very exposed to a downside shock." He agrees that we end with inflation, thanks to the Fed's desperation to kindle it, but not yet. Meanwhile Joshi makes an important argument that I have heard little about. In short, he reminds us that global real estate, all bar about 10% of which is residential, is worth far more than the world's entire supply of stocks and bonds. At some $290 trillion, it's even worth far more than the world's annual gross domestic product:  This is important because housing has boomed on the back of low yields just as much as stocks — in fact, probably more. As Joshi shows, real estate prices have vastly outperformed rents, which have risen roughly in line with nominal GDP. Just as stocks' P/E multiples have been buoyed by low yields, so house prices have been supported by startlingly cheap mortgage finance:  The implication is that we are all leveraged to low bond yields. As Joshi's chart below shows, the implied rental yield paid by property has moved in line with yields on long U.S. and Chinese bonds. An increase in bond yields that in turn causes a drop of 10% in the level of global house prices isn't hard to imagine. That would be a wealth effect of almost $30 trillion, or about a third of global GDP, and a sledgehammer to the world economy:  Thus, Joshi argues that such a decline would inflict one last deflationary downdraft. That by extension means not betting all out on inflation just yet. He suggests the crucial stress point would come when 30-year yields reach 3.75%: where is the pain point? Our answer is that if inflation fears lifted the average US and China 30-year bond yield to 3.75 percent (from 3 percent now), it would constitute the change in trend that would unleash a massive countervailing deflationary impulse from falling house prices

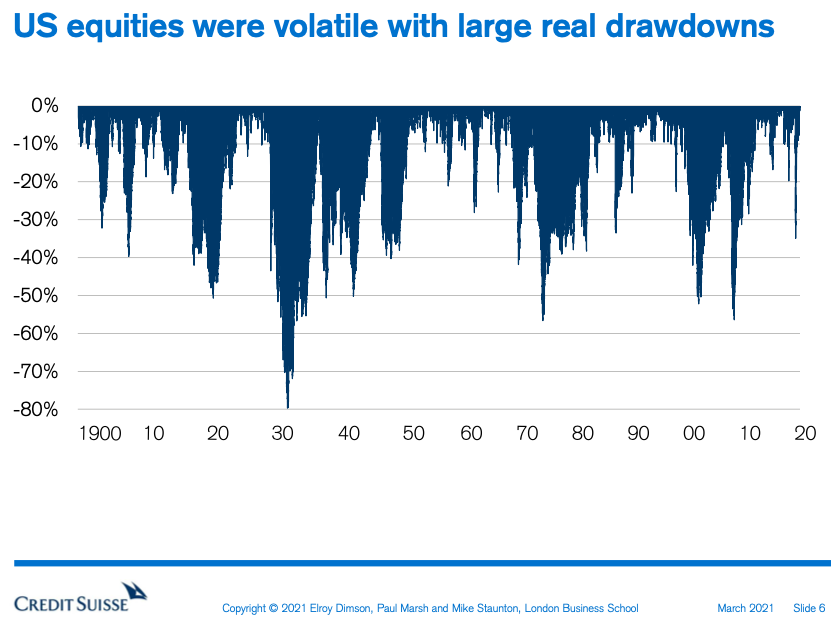

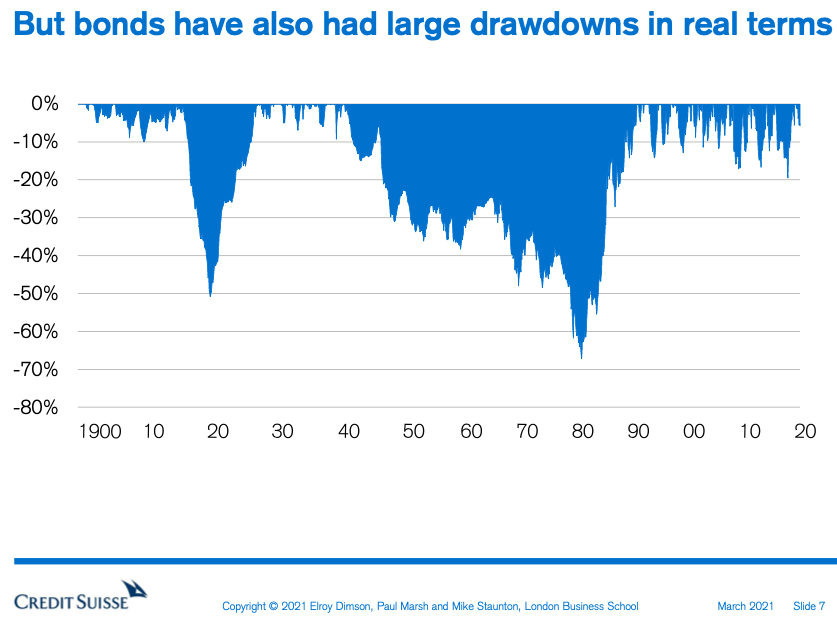

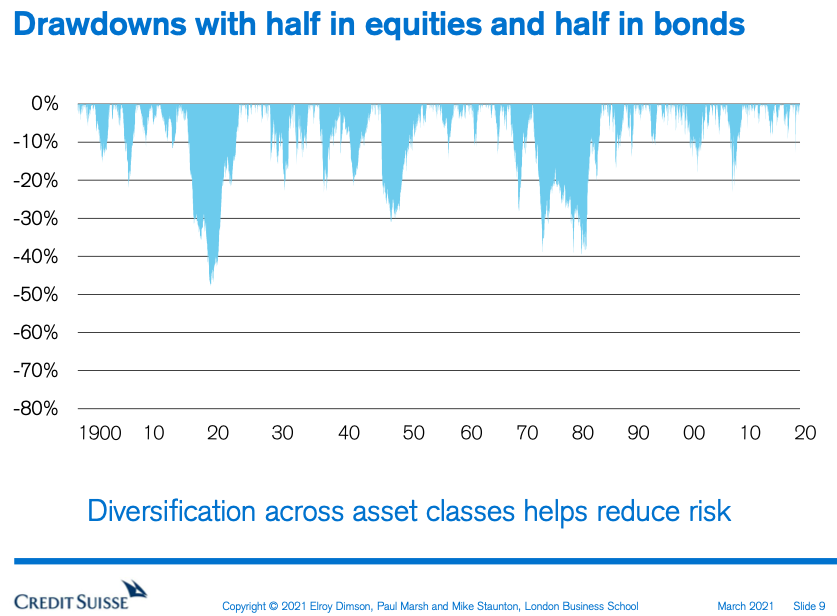

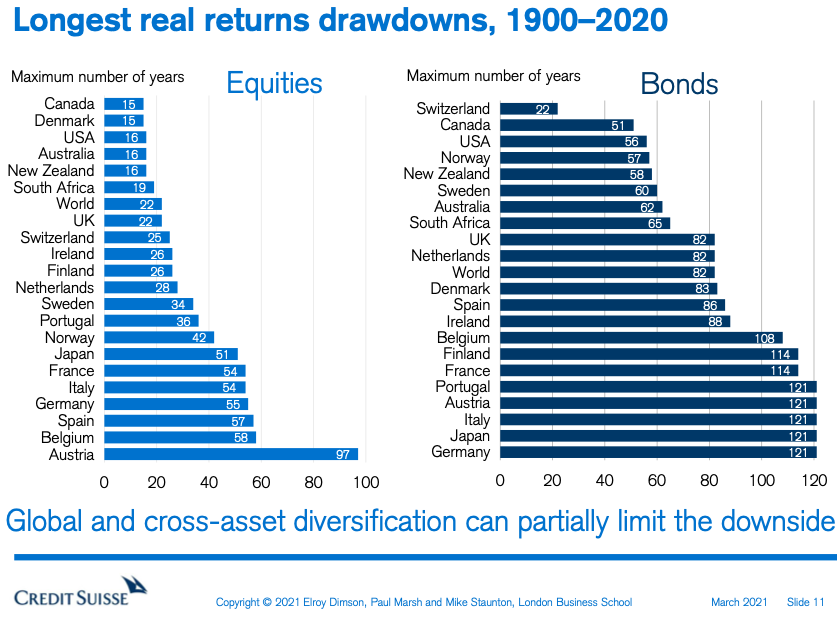

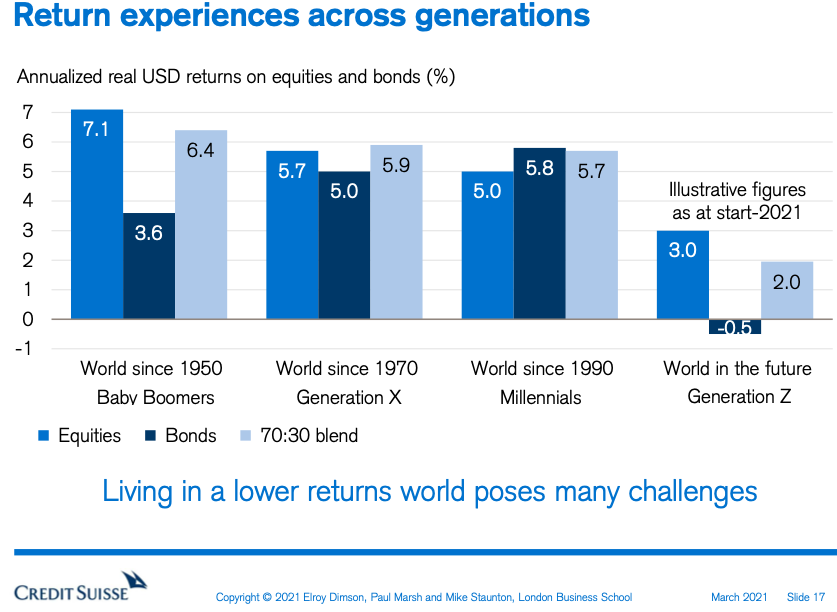

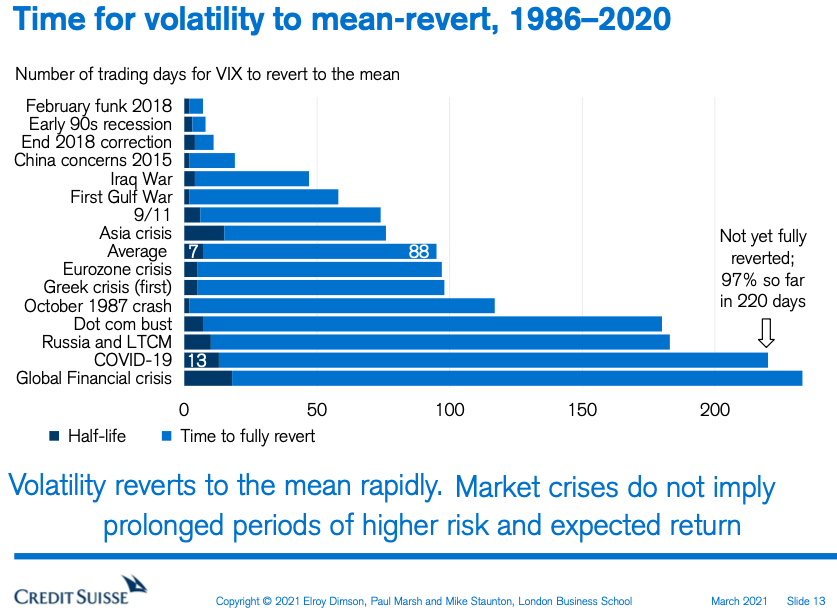

If any of this seems counterintuitive, look at the bizarre state of affairs where an entire generation seems to be unable to afford to buy a house, and adults are continuing to live in the parental home for many years after leaving school. That's a clear indicator that housing is artificially expensive. Bringing prices down would be a great way to alleviate some of the ugliness and division in society — but it's hard to see how that can happen without an accident. Lessons of HistoryMeanwhile, Thursday also saw the publication of the 2021 Global Investment Returns Yearbook, sponsored by Credit Suisse Group AG and compiled for decades now by a trio of financial historians who were all originally based at London Business School: Elroy Dimson, Paul Marsh and Mike Staunton. The Dimson/Marsh/Staunton database covers a range of countries' stock, bond and cash returns back to 1900 and is something of a gold standard for long-term investors. This year, their data is particularly useful when trying to work out what might lie ahead. If it is right that inflation is brewing, and that both stocks and bonds could fall together, life could be difficult. This chart shows how deep drawdowns have been from a market high, over time, and how long they have lasted (all are measured in real terms). This confirms that the bear market after the Great Crash of 1929 was by far the worst on record, and also shows that last year's Covid selloff saw a remarkably swift recovery:  What is interesting is to see the same exercise for bonds. Contrary to expectation, bonds have had much longer slumps before than stocks. In real terms, the bond selloff that reached its worst in 1980 was almost as bad as the 1930s decline in equities, with a maximum drawdown of almost 70%. It also went on far longer. What is also very intriguing is to see how mild the bond market has been since then. Eye-balling the chart, it looks as though we are overdue for another big retreat:  The feeling that we have been living a charmed life for the last few decades intensifies when the two markets are put together. The following chart shows what losses would have been suffered if we constantly held a portfolio of 50% stocks and 50% bonds. The 1960s and 1970s, the era of entrenched inflation, saw interminable pain. For the last 40 years, bonds have done their job as a diversifier, and saved us from ever being down as much as 20%:  As Marsh put it, diversification really is one of the few free lunches in finance. But with inflation and rising yields, that lunch is going to start commanding a price. This explains the worries about the future of "60/40" balanced portfolios of stocks and bonds. A further concern is that bond declines have shown a historical tendency to drag on far longer than equity slumps. The following chart ranks countries by length of time investors have had to go from one record high before getting back to that point. It's chilling to see that bond investors in countries like the U.K. and the Netherlands have suffered drawdowns that lasted more than 80 years. Inflation can make the work of saving for retirement vastly more difficult:  A further alarming finding amplifies the concerns over intergenerational injustice. This doesn't just spring from the housing market. Generation X (mine) has been able to make 5.9% annualized real returns from equities and bonds — not as much as our parents, and surprisingly not so much more than millennials have made, thanks to the problems of the 1970s, but still adequate. The Dimson/Marsh/Staunton projections for Generation Z, my children's generation, however, are terrifying:  One final and slightly concerning point concerns volatility. In general, volatility itself is volatile; it will make sharp spikes, terrify everyone rigid for a few days or weeks, and swiftly return to normal. Invariably, volatility has reverted to its mean in less than a year, after each of the market crises of the last 34 years. But while the Covid shock saw a spectacularly quick recovery in the price level, it has seen an unusually slow recovery in terms of volatility. It hasn't yet reverted to its mean, and has risen again this week. It now looks a good bet that this spike will last even longer than the surge of volatility that surrounded the global financial crisis, which is by far the greatest to date. Persistent volatility shows that anxiety remains, even as vaccines spread through the population's veins:  The entire yearbook is immense, and can be mined for all kinds of gems. You can get hold of a summary, which has everything I've included here, from this address. Survival TipsI now have a long list of great movie sound tracks. Among the more interesting ones are Baby Driver, The Lost Boys, Reality Bites (which gets extra points from me for starting with When You Come Back To Me by overlooked geniuses World Party), Singles, That Summer 1979 (which as the title implies, encapsulates my childhood) and Whatever Happened to Harold Smith. Among particularly famous movies, try Beverly Hills Cop, Easy Rider, American Graffiti, The Graduate (which seems a little bit like cheating but Simon and Garfunkel really were awe-inspiring) and Pulp Fiction (on which the music is fun but the dialogue is something to die for). The two that seemed to come up the most were Garden State (which has a line-up of relatively unknown but beautiful songs that all create a distinctive mood) and Grosse Point Blank, which features The Beat's ska classic Mirror in the Bathroom. I'm sure there are more out there, but I hope some of these help you enjoy your weekend. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment