| So much for tariffs.

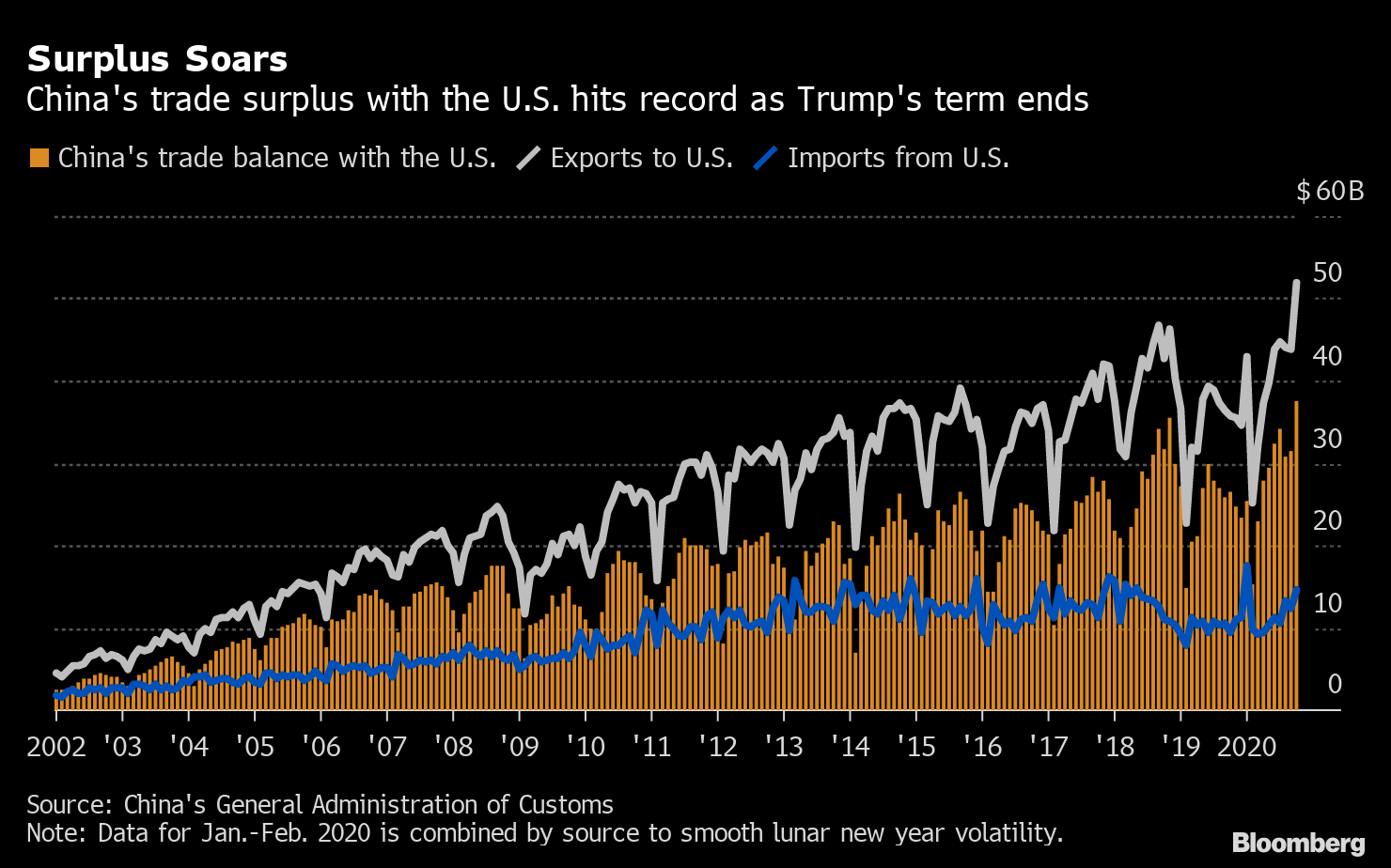

China exported an unprecedented $268 billion in goods in November, resulting in a record trade surplus — even with the U.S. That helped cap what's shaping up to be a stellar recovery for the world's second-largest economy as surging demand for masks, gloves and other personal protection equipment contributed to keeping Chinese factories clanking during the pandemic.

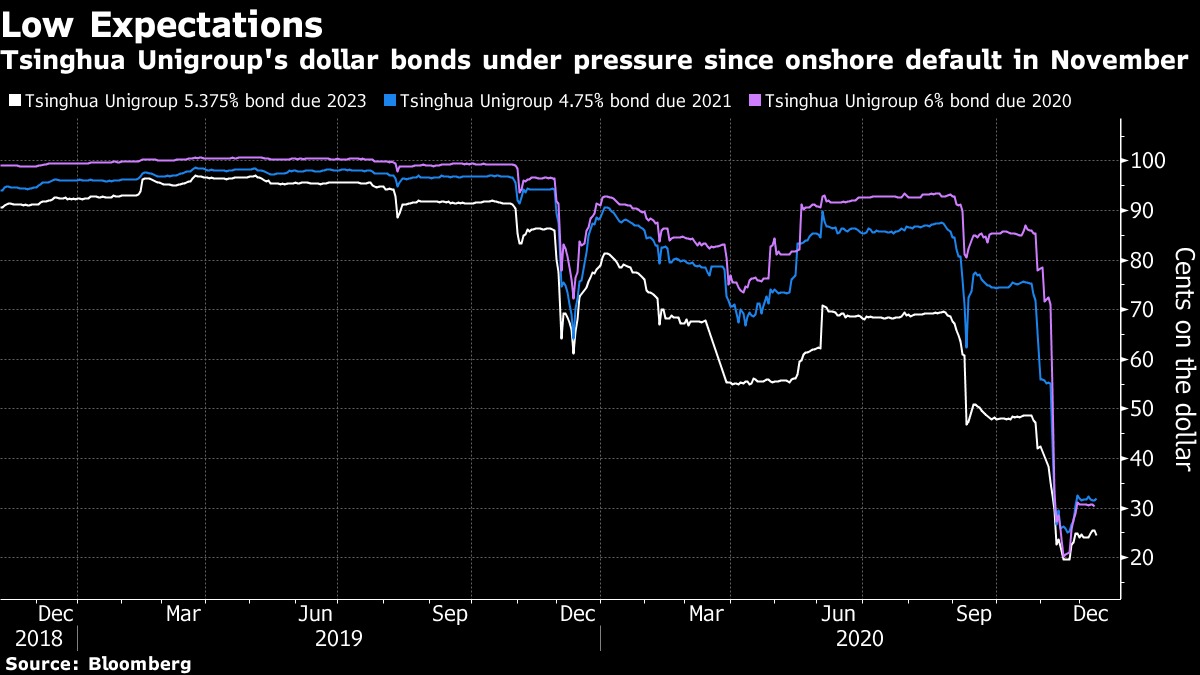

The latest statistics coming out of Beijing could bode ill for the legacy of the outgoing Trump administration, which used export-import imbalances as its primary justification for waging a years-long trade war with China to make the U.S. more self sufficient. If anything, it appears as though American farmers are as reliant on China today as they've ever been and vulnerable to any sudden changes in Chinese buying patterns.  Either way, all things U.S.-China will be one of the biggest things that President-elect Joe Biden will have to re-examine after he's sworn into office just over a month from now. Though he's ruled out immediately dismantling his predecessor's agreements until further review, the adversarial nature of the relationship is widely expected to persist under the new occupants of the White House. Big DefaultDespite the resilient economy, not all's well in China. Tsinghua Unigroup Co. failed to make payments on its debt, deepening the chipmaker's liquidity crisis. Its latest bond blowup adds to a wave of defaults in China's state sector. China has long vowed to let its weaker state-run enterprises, known as "zombie" firms, fail and use defaults and bankruptcies to resolve their debt problems, as part of a broader campaign to reinforce market discipline and boost economic efficiencies.  The missed payment also represents a remarkable reversal of fortune for a company that once stood at the forefront of China's semiconductor ambitions. About five years ago, Unigroup was one of China's most aggressive acquirers, even planning a bold $23 billion bid for memory-chip giant Micron Technology Inc. and making its then-chairman a billionaire along the way. More SanctionsSpeaking of tensions, the U.S. kicked off the week by announcing sanctions against 14 members of China's National People's Congress as the Trump administration seeks to ratchet up pressure on Beijing over its crackdown on dissent in Hong Kong. The move is part of President Donald Trump's effort to pile pressure on China's Xi Jinping and the ruling Communist Party in his final weeks in office before Biden takes over. Biden has said he expects to keep up pressure on Beijing over Hong Kong, though he's unlikely to resort to unilateral sanctions to the extent that Trump has. The silver lining: Speculation that one of China's most senior officials — Politburo Standing Committee member Li Zhanshu — would be targeted turned out not to be the case. Also, China's top diplomat, Foreign Minister Wang Yi, telegraphed some conciliatory signals by calling for cooperation with the U.S. in issues ranging from pandemic control to economic dialogue and climate change to help restore some trust between the two.  Chinese Foreign Minister Wang Yi walks by the U.S. and Chinese national flags. / AFP PHOTO / POOL / Andy Wong via Getty Images Photographer: AFP Contributor/AFP Tension-ProofMuch ink has been spilled recently about Beijing's deteriorating relations with Canberra, but that hasn't stopped Australia from raking in a windfall from China's insatiable demand for iron ore as the country cranks up construction of roads, bridges and other infrastructure projects to stimulate the economy in a pandemic-ravaged world. Australia, the world's most China-dependent rich economy, has been hit in recent months by its biggest customer with steep Chinese tariffs and restrictions on beef, seafood and wine. Ties have deteriorated since 2018 after Canberra barred Huawei Technologies Co. from building a 5G network, and relations worsened this year when Australia called for an independent probe into the origins of the pandemic in Wuhan.  A bottle of Coonawarra Cabernet Sauvignon 2018 at the Royal Star Wine showroom in Sydney, Australia, on Nov. 17, 2020. Photographer: Brent Lewin/Bloomberg Yet the exports impacted by China's restrictions to date account for just 0.3% of Australian gross domestic product. What would really sting, according to Goldman Sachs, would be if China were to ban Australian iron ore imports — something that would cut Australia's GDP growth by about 2 percentage points over 12 months and blow out Australia's budget deficit by about $9 billion. That's unlikely to happen given that Australia makes up more than half of global iron ore shipments, giving Beijing few alternatives. Meanwhile, iron ore futures continue to extend their dramatic rally. HSBC Entangled AgainIn Hong Kong, HSBC is back in the spotlight for unintended reasons. In recent days, a former local lawmaker and a church cried foul after the most widely used bank in the city froze their accounts. Ted Hui, an ex pro-democracy lawmaker who's fled to the U.K., and the Good Neighbour North District Church accused the British lender of making those moves for political reasons.  The HSBC headquarters building stands illuminated in Hong Kong. Photographer: Chan Long Hei/Bloomberg The controversy was enough to drive shares of HSBC lower in Hong Kong and marked the latest episode dragging the bank into the complex geopolitical situation in the former British colony. China's clampdown on Hong Kong has also drawn a slate of sanctions from Washington, entangling global banks in the political back-and-forth. Still, the stock has surged about 50% since hitting a quarter-century low in September on optimism the lender will reintroduce dividend payments. HSBC, which gets more than a third of its revenue from Hong Kong, has declined to comment on matters concerning individual accounts, and directed such inquiries to the police. The lender was criticized by activists in 2019, when the closure of an account linked to the city's pro-democracy movement turned the bank into a target of protesters' anger. HSBC was also rebuked by British and U.S. politicians after the bank's Asia chief Peter Wong signed a petition in support of the controversial China-drafted national security law. What We're ReadingAnd finally, a few other things that caught our attention: - Big overhang on Chinese stocks

- Pandemic bonds: As bright of an idea as insuring one's toaster?

- China's spoiled rich kids are trying to just be rich kids

- Remember HNA? Back in the news with a blockbuster deal

- Chinese cabin crew members urged to wear diapers

|

Post a Comment