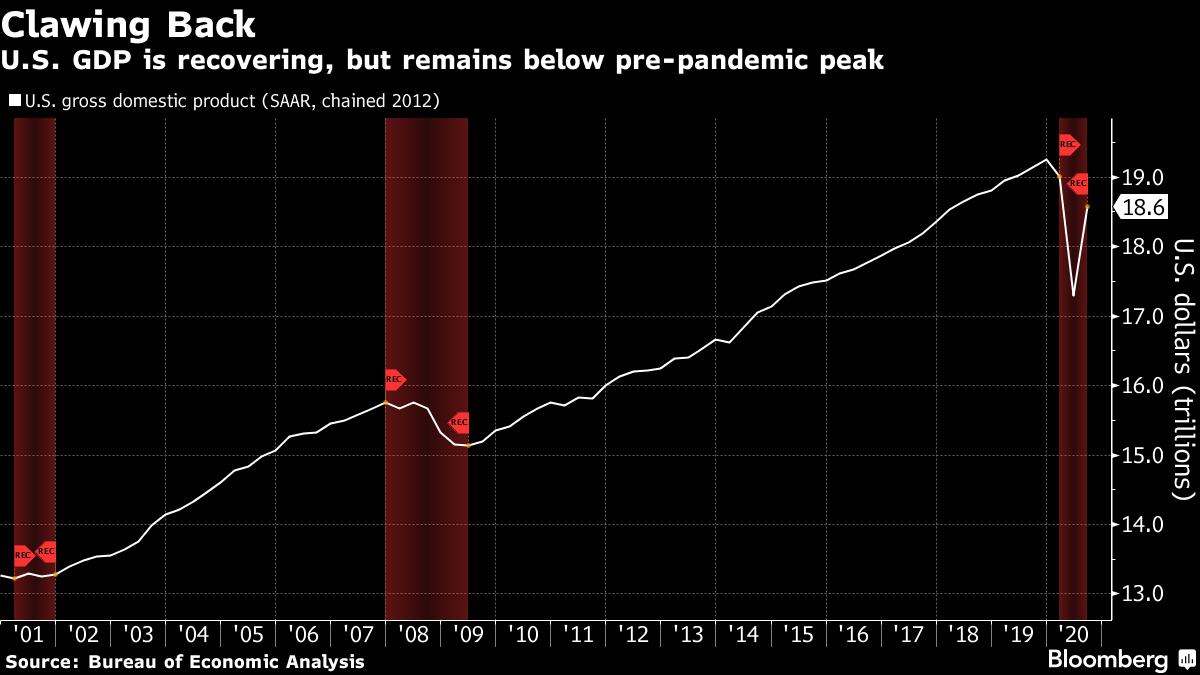

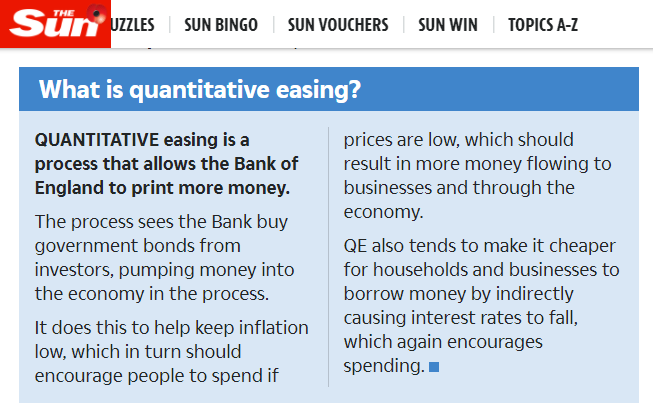

| Welcome to the Weekly Fix, the newsletter that's once and for all finally sworn off looking at poles. –Emily Barrett, now Asia FX editor, on the other side of the world. Kind of Blue*At the time of writing the outcome of the U.S. election hangs in the balance. Clearly this isn't the Blue Wave that so many traders were counting on to reward historically large wagers against U.S. government bonds. The big short is in tatters, and the buyers are back in, with the endgame to this 2020 race already looking pretty litigious. The big prize was a united government. After two days of vote tallying -- and taking into account the twist of a record number of postal votes in the pandemic -- Democrats look poised to win the presidency, and hold the House, but the Senate appears set for a narrow Republican majority. Markets are reacting to that split. Equities and bonds rallied as the races tightened, albeit for very different reasons. Conventional wisdom says that stocks like certainty, and legislative gridlock will deliver that, if nothing else. Tax increases and stricter regulations are less likely, and the Senate approvals process will ensure only the most moderate candidates make the cabinet. This outcome is a positive for equities and credit, as "you get all the good parts without most of the bad," said Lisa Hornby, head of U.S. multi-sector fixed income at Schroders in New York -- citing "more-traditional trade policy" among the advantages. What matters to bonds is that another large pandemic relief package is less possible. As the first big battleground state, Florida, fell to Trump, the U.S. 10-year yield tumbled from its highest levels since June, moving almost a quarter point before steadying around 0.75%.  Fresh from his victory in Kentucky, current Senate leader Mitch McConnell had more-positive things to say about a stimulus deal by year end, but it's unlikely to look much like the north-of-$2 trillion bid from the Democrats. "Among the potential resolutions, a Biden White House and GOP-controlled Senate formulation yields the skimpiest stimulus," DC-based Markets Policy Partners observed in their daily note, suggesting the next package might be closer to $500 billion. "This puts the ball back in the Fed's court for additional stimulus, such as increased asset purchases, which we expect to be signaled in December and enacted early next year." The potential for a more fiscally conservative path in the U.S. than previously thought buttresses the case for Treasuries in two ways. First via the lower-than-anticipated supply, as the Treasury this week slashed its borrowing estimates for the remainder of 2020 to a little over half its August projection, to $617 billion. The second rallying force is the ominous trajectory of the pandemic, as the U.S. this week became the first country to top 100,000 cases in a single day. Among the many adjusting their calls this week for a nail-biting finish was Goldman Sachs, as rates strategist Praveen Korapaty now sees room for the 10-year yield to head toward 0.60%, "particularly in the face of uncertainty related to the worsening public health trajectory and the likely challenges of passing additional fiscal relief in the 'lame duck' session." Steady FedA third reason for Treasury bears to go back into hibernation is the Fed. The central bank kept well out of the political fray this week with a policy statement so bland, the most obvious change from last month was the date at the top. But Chair Jerome Powell told reporters that he and his colleagues "discussed our asset purchases," which are currently running at a $120 billion monthly pace. He said that the central bank could shift the composition, duration, size or the life-cycle of the program to provide more support to the economy as it struggles with the pandemic. As Blue Wave hopes have ebbed, so too has some bold pricing for tighter Fed policy. Eurodollar futures traders sprang into action as the vote count progressed, paring some wagers that a surge of government spending would spur the recovery and force the central bank to raise interest rates sooner than policy makers currently anticipate. As it stands, it's unlikely we'll see any change in their median projection for interest rates to stay at the zero bound at least through 2023. David Norris, head of U.S. credit at TwentyFour Asset Management, reckons they're staying put at least for as long as last time around after the Great Financial Crisis -- which was seven years. Stealth SteepenerSo the reflation trade isn't looking healthy. Look how quickly this closer-than-expected presidential race has slapped down the yield curve. At the start of the week the 30-year yield had risen to highest point above the five year since 2016 -- the crash at the long-end has reversed all the of the past month's climb.  The reflationistas' loss may be a gain for global investors, as a flatter U.S. curve has been typically supportive of inflows to relatively higher-yielding emerging markets. Asia bond- and currency bulls have already seen some benefits -- demand for carry drove Indonesia's rupiah to its strongest level in almost four months. "This outcome is the best of both worlds," said Ken Peng, head of Asia investment strategy at Citigroup Inc.'s private-banking arm, who sees lower rates keeping the U.S. dollar on the backfoot, and boosting risk appetite.  But support for the steeper curve hasn't entirely evaporated, with some investors looking through the surprise elements of the election to focus instead on the resilience of U.S. economic data thus far, and the potential for a vaccine. Greg Staples of DWS Investment Management in New York is keeping the faith in what he sees as the underlying strength of the U.S. economy, arguing that the downturn that was feared as the first fiscal stimulus rolled off at the end of July didn't materialize. "If longer Treasury rates started drifting up for the wrong reasons, meaning portfolio managers don't want the risk, then Powell will step in and through QE try and manage that down," he said. But if they're climbing for reasons such as a steeper drop in unemployment, or rebounding activity, "he's going to let that happen because it signals that the recovery is really taking root." The U.S. economy did indeed report its fastest quarterly growth on record in the three months through September, at a rate of 33.1%. Though it says a lot about the depth of the hole the country is still in, that this hasn't returned GDP to pre-March levels.  *With apologies to Miles Davis Movers and ShakersA short selection this month, as there's quite enough moving and shaking going on with the search for a leader of the free world... Lazard CEO Seeks to Hire More After a 'Pretty Aggressive' Year RBC Names Hunter Head of Global Markets With Bowick Retiring Citadel Hires Three Fund Managers as Battle for Talent Heats Up Bonus PointsOn the anniversary Penguin's first George Orwell publication, here are its best covers Election volatility risk may have shifted to December Connaught London named world's best bar at worst possible time Climate lawsuits flood world's courts and everyone's a target The Sun scoops with the Bank of England's 150bn pound QE. And explains QE.  |

Post a Comment