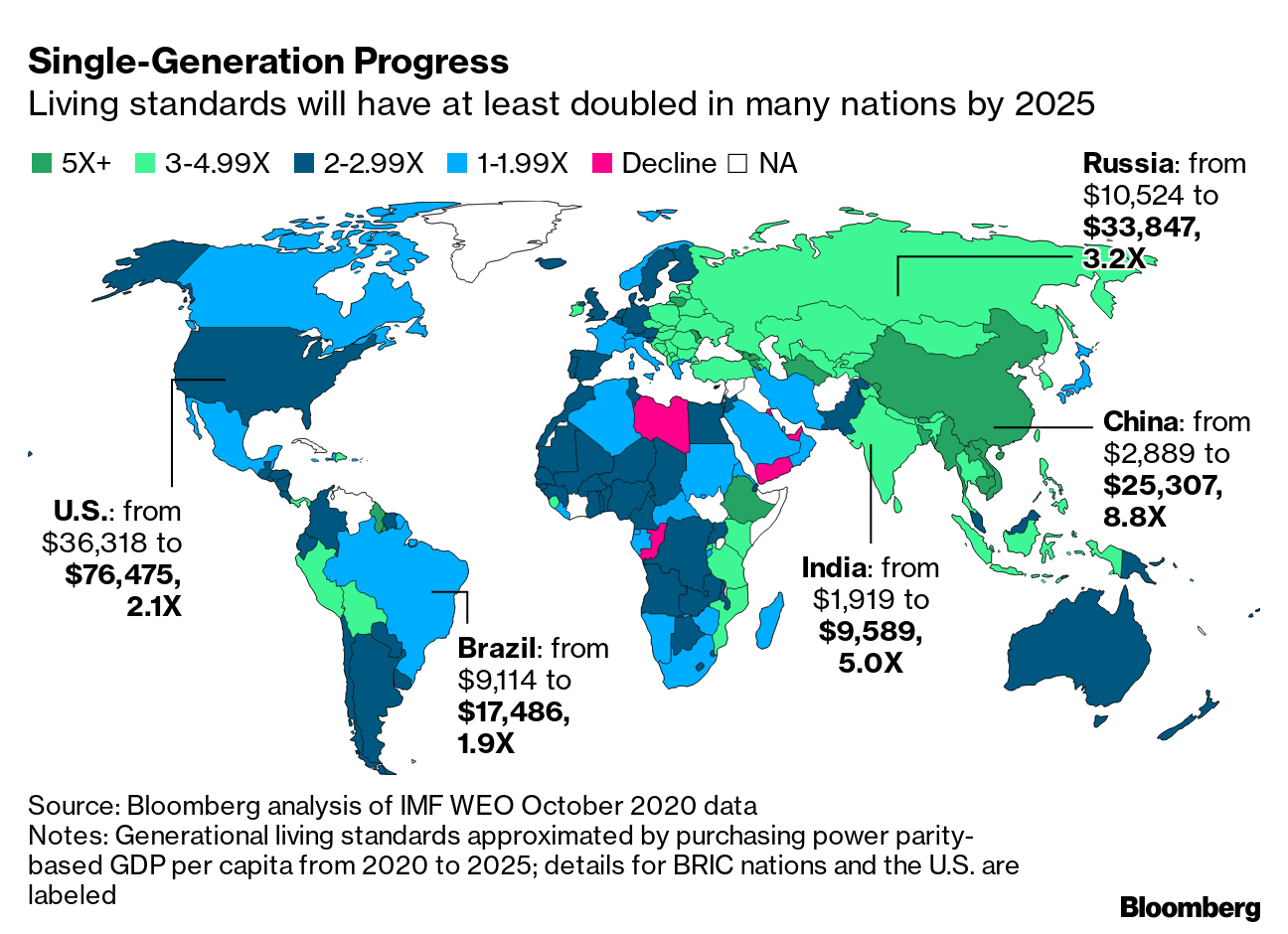

| After a Covid-induced interlude, tackling China's debt problem now appears to be back on Beijing's agenda. In the past two weeks, three state-owned firms have defaulted on bonds. One was a coal miner based in central China. Another was a carmaker, Brilliance Auto Group, which has struggled to make money beyond a joint venture it has with BMW. The third defaulter was Tsinghua Unigroup, a chipmaker laden with debt thanks to years of frenzied expansion. This quick secession of defaults has been jarring for China's bond market, which has had a relatively short history of dealing with defaults and even less experience with government-owned companies failing to pay their debts. Lending to state-owned firms has long been seen as largely risk-free, with the prevailing wisdom being that the government would pay back debts if the company couldn't. That logic seems to be on far less solid footing today than it was just a few weeks ago. The reaction in financial markets has reflected that. A number of Chinese banks have begun cutting their holdings of bonds sold by state-owned firms, worried that more defaults are coming. Confidence was so shaken that a deputy governor of Shanxi, a coal-rich region in central China, took the unusual step this week of guaranteeing publicly that all the government-owned companies from his province would make their payments. With the benefit of hindsight though, there were signs that this spate of missed payments was coming. Chinese policy makers have made it clear since 2016 that they view the country's mountain of debt, which Bloomberg Economics estimates exceeded 300% of GDP last year, as a tremendous threat. And one of the key ways they had sought to rein in borrowing was more defaults. It was only in 2014 that China's bond market had its first default of any kind. Prior to that, when companies ran into trouble, be they private or state-owned, local governments stepped in to find a way to pay creditors. While that avoided painful losses and bankruptcies, it also left reckless borrowing and lending unpunished. Since 2014, the number of missed payments has risen steadily each year. And while most of the defaults have been by borrowers from the private sector, a few state-owned firms have also failed to pay their debts on time.  But this year that trend of growing defaults went through a pause thanks to Covid-19. With much of China's economy under strict lockdown in early 2020, China began pumping money into its economy to help buffer it against the pandemic. Authorities also began asking creditors to give borrowers more leeway in repaying debts. But as the country has reopened and business activity has recovered, Beijing has begun withdrawing some of the measures taken to help buffer the economy. The defaults have also resumed -- though admittedly three in two weeks is a jarring new pace. China, it seems, is getting back to normal and that means allowing more short-term financial pain to instill discipline across the sprawling financial system. Scale of WWITensions between the U.S. and China have increased to dangerous levels and could lead the world into a catastrophe comparable to World War I. That was the dire warning former U.S. Secretary of State Henry Kissinger, who paved the way for President Richard Nixon's visit to China half a century ago, delivered this week at the Bloomberg New Economy Forum. To prevent such an outcome, Kissinger advocated an "institutional system" through which senior envoys appointed by the presidents of the two countries would stay in touch to manage issues. Beijing and Washington should also agree that no matter what conflicts exist between them that they will not resort to military means to resolve them.  Henry Kissinger, former U.S. secretary of state, at the Bloomberg New Economy Forum in Beijing in November 2019. Photographer: Takaaki Iwabu/Bloomberg Security PactAustralian Prime Minister Scott Morrison was in Tokyo this week where he and Japanese Prime Minister Yoshihide Suga signed a security agreement allowing military personnel from each nation to stay in the other's country for joint exercises and other activities. Seen from Beijing, the pact will look like an attempt to contain China's rise. Both Tokyo and Canberra have crucial trade links with China, but have also clashed with Beijing over issues ranging from territorial claims to bans against telecom equipment produced by Chinese tech giant Huawei. Canberra has especially drawn China's ire as of late, with Beijing recently limiting shipments of coal, wine and other goods from Australia. But with U.S. President-Elect Joe Biden expected to at least initially place more of his focus on repairing domestic divisions and economic damage from the pandemic, middle powers such as Australia and Japan will likely continue seeking to form a more united front when dealing with China. As Nobukatsu Kanehara, a former deputy secretary-general of Japan's National Security Secretariat, explains, China is now too big for any country apart from the U.S. to deal with on its own. Getting RicherChinese wealth has undoubtedly increased. Recently released data from the International Monetary Fund shows just how big a jump it's been. By 2025, the IMF estimates that China's per-capita GDP, adjusted for purchasing power, will hit $25,307. That would be an almost nine-fold surge from where it was at the start of the century and rank China 70th in the world, putting it close to joining the richest one-third of all nations.  What We're ReadingAnd finally, a few other things that caught our attention: |

Post a Comment