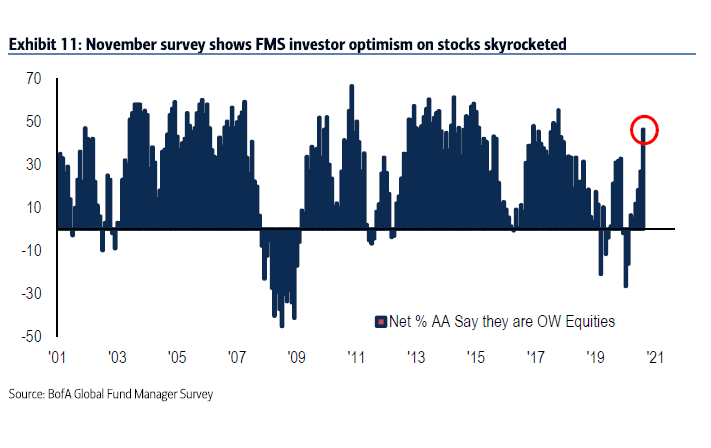

| Trump's purge continues, Pfizer vaccine passes key hurdle, and Bitcoin surges. You're fired President Donald Trump fired Christopher Krebs, the director of the Cybersecurity and Infrastructure Security Agency, after Krebs publicly contradicted the president's unfounded claims about widespread election fraud. The move comes amid a broader purge at the Pentagon. Trump continues to challenge the election result in court, with little success. His celebration after the Board of Canvassers refused to certify the result in Wayne County, Michigan was cut short when the decision was reversed. Vaccine Pfizer Inc. is preparing to seek an emergency-use authorization for its vaccine from U.S. regulators after reaching a key safety milestone Chief Executive Officer Albert Bourla said. Until a vaccine becomes widely available, there seems little alternative to more restrictions in Europe and the U.S. where case loads and hospitalizations remain high. Speaker Nancy Pelosi and Senate Minority Leader Chuck Schumer asked Senate Majority Leader Mitch McConnell to resume talks on stimulus as world leaders, speaking at the Bloomberg New Economy Forum, called for more fiscal measures to help the pandemic-stricken economy. Higher Bitcoin is trading above $18,000 this morning as the recent resurgence of the cryptocurrency continues. The digital token has gained 150% this year, and even Bridgewater Associates' Ray Dalio is wondering if he's missing something. Some of the gain can be attributed to Bitcoin's move closer to the mainstream as companies such as PayPal Holdings Inc. allow it to be used on their platform. Volatility remains a feature though, with the cryptocurrency trading within an almost $1,000 range this morning alone. Markets mixedFears about the continued rise in Covid infections is being tempered by optimism about the progress of vaccines among equity investors. Overnight, the MSCI Asia Pacific Index added 0.3% while Japan's Topix index closed 0.8% lower. In Europe, the Stoxx 600 Index was 0.3% higher at 5:50 a.m. Eastern Time with traders favoring cyclical stocks. S&P 500 futures pointed to small gain at the open, the 10-year Treasury yield was at 0.859%, oil was higher and gold was lower. Coming up... U.S. housing starts and building permits data for October is at 8:30 a.m., with Canadian CPI for the month also at that time. The oil market expects an increase in stockpiles to be announced when the latest U.S. inventory data is published at 10:30 a.m. Today's sale of $27 billion of 20-year Treasuries at 1:00 p.m. is the largest ever of the tenor. Georgia is expected to complete the hand recount of votes from the Nov. 3 election. Lowe's Cos Inc., Target Corp., TJX Cos Inc. and Nvidia Corp. are among the companies reporting results. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Joe's interested in this morningIf there's one word to describe both the economy and the stock market over the past six months, I might go with 'underestimated.' Basically at every turn, data has come in significantly better than economists have expected, corporate earnings have been better than analysts expected, and the stock market has performed better than investors expected. This can be seen in all kinds of ways. For example on corporate fundamentals, in Goldman Sachs' latest Weekly Kickstart note, David J. Kostin notes: "67% of S&P 500 firms beat consensus EPS estimates by at least one standard deviation in 3Q, the highest share since at least 1998." But perhaps the period of underestimation is coming to an end. Or at least starting to taper a little bit. Yesterday we got retail sales data that was the slowest in six months. Of course a slowdown is to be expected, as noted by economist Tim Duy. However not only is the pace of retail sales growth slowing down, it also came in well below economist expectations. Excluding auto and gas activity, retail sales grew just 0.2% on a sequential basis versus 0.6% that economists had penciled in. We see this phenomenon starting to emerge across the eco landscape overall. Citi's Economic Surprise Index, which measures how the data is coming in relative to consensus expectations, has begun to roll over sharply. It's not a bad thing per se. A surprise index naturally is going to mean revert, but it does suggest that forecasters have become more realistic, and that upside suprises are getting more rare.  Meanwhile we also got the latest installment of the Bank of America Global Fund Manager Survey yesterday, and it too showed that investors finally believe in the bull market. The share of survey respondents who say they are overweight on equities is now at multi-year highs.  None of this is bad per se, or evidence that the good times will come to an end. But between economists catching up to the improved macro picture and investors piling into stocks, it appears at least that the skeptics are disappearing and that the underestimation phase of the recovery is coming to an end. Joe Weisenthal is an editor at Bloomberg. The world's most influential leaders will be there. Will you? Click here to join Bloomberg New Economy Forum for a virtual Global Town Hall on November 16-19 and be part of change in real time. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment