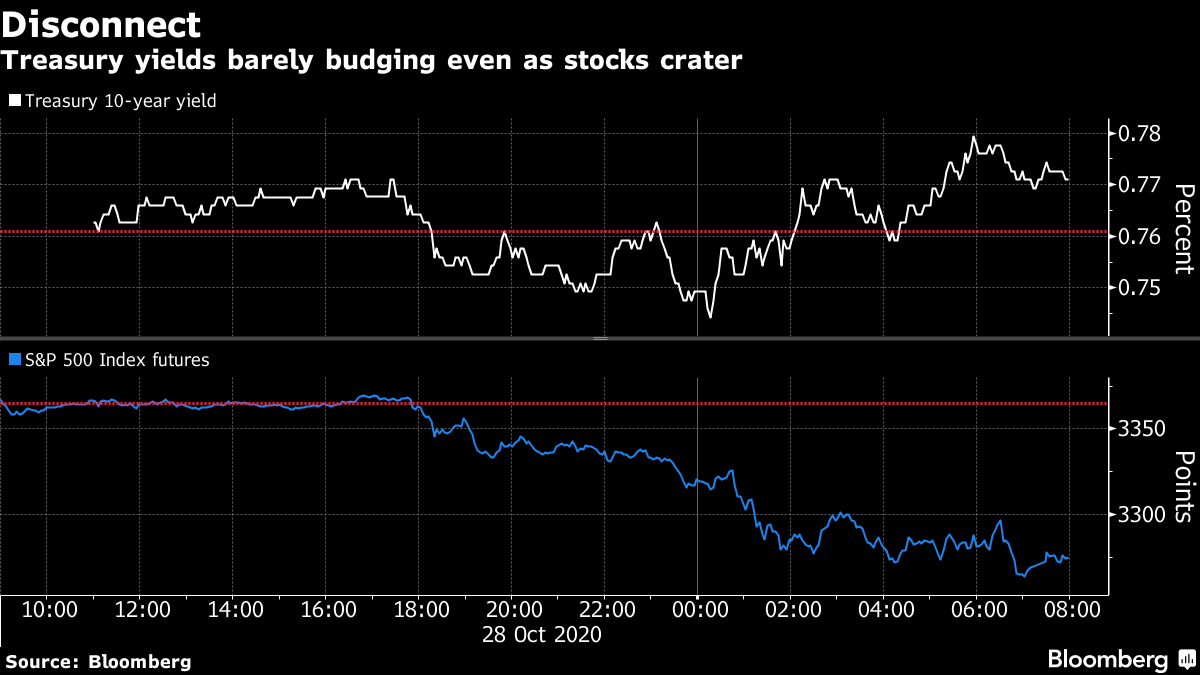

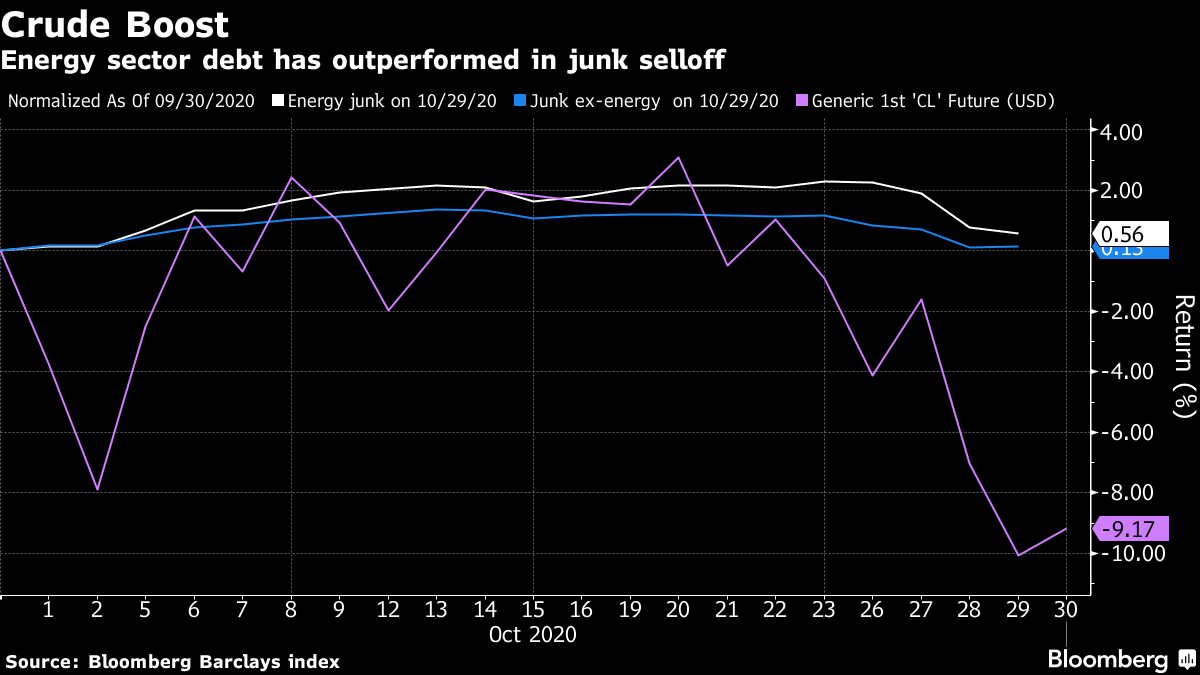

| Welcome to the Weekly Fix, the newsletter that thinks this monetary versus fiscal relationship is about to get really complicated. –Emily Barrett, now Asia FX editor, on the other side of the world. The VoteThe theory that the U.S. election will clear the way for a deluge of fiscal spending that will propel yields higher may still hold, but... pandemic. The virus showed us yet again this week that it's in charge. Global yields had only just started climbing, with polls suggesting Democrats have a shot at a clean sweep of the White House and Congress, and an unfettered decision on a large spending package. Then, a surge in infections on both sides of the Atlantic and the prospect of renewed lockdowns for Europe's largest economies drove benchmark rates back from four-month highs. The reversal was bad news for leveraged investors, who've never had a bigger bet on losses in bond futures. But they can take heart that the countermove is already looking played out. The U.S. 10-year benchmark actually closed Wednesday's grueling session -- which lopped 3.5% off the S&P 500 -- a basis point higher, and it's just a few steps below last week's peak.  It's tempting to say this is yet more evidence of the death of the Treasury hedge, except that other traditional haven assets have also been slow to catch much of a bid, with the yen finding resistance around 104 to the dollar and gold falling. The reality is the big risk event is barely three trading sessions away, and, for bond bears, it would seem perverse to throw in the towel on what could be the trade of the year. Polls -- so far anyway -- still signal a Democratic victory in the presidential vote. The Senate race appears pretty tight. Ultimately, the case for higher yields hinges on fiscal stimulus, and it's hard to argue that's not going to happen. Amid the crush of headlines next week, we have the Treasury borrowing estimates and refunding announcement, which could well show the government looking to raise hundreds of billions of dollars of debt in the three months to December. But let's spare a moment for the Treasury bulls, because if we learned something from the last time around, it's that market forecasts are written in sawdust...or maybe hanging chads. It's fair to say that, with the pandemic not under control -- see the White House Chief of Staff's comments -- and the arrival of a vaccine still TBC, the size and timing of another relief package will be key to the path of the economy and all who sail in it. BMO's Ian Lyngen stated the bear case and its discontents succinctly: "At the risk of oversimplifying the issue, there is a perception that 2021 cannot be worse than 2020 – we hope this holds... An attempt to breach 1.0% 10s is certainly well within the range of conceivable outcomes – albeit one that relies on the relatively smooth election process that delivers results quickly and with limited uncertainty. Admittedly, such a scenario next week is not a forgone conclusion by any means." That last qualifier invites us to stare into the dumpster fire of a contested election, which could easily see yields dive. The Morning AfterO to be a fly on the wall in the next Federal Reserve meeting right after the election. If the much-discussed "Blue Wave" should materialize, there'll be more focus on the long end and how best to keep those borrowing costs in check. So far the overriding message from the Fed is that it's not eager to swing to the rescue again. Policy makers have spent the past several weeks repeating with various degrees of exasperation that it's the government's turn. Former NY Fed President Bill Dudley phrased it bluntly in a Bloomberg column entitled: "The Fed is Really Close To Running Out of Firepower": "No doubt, Fed officials should still commit to using all their tools to the fullest. But they should also make it abundantly clear that monetary policy can provide only limited additional support to the economy. It's up to legislators and the White House to give the economy what it needs — and right now, that means considerably greater fiscal stimulus." But don't be too sure that the Fed will sit on its hands after the election, say Jefferies' economists Aneta Markowska and Tom Simons. "In September, the Fed highlighted three risks to growth: lack of fiscal support, a new wave of COVID infections, and a tightening of financial conditions. All three risks have materialized."  The tightening isn't profound at this point, but the economists highlight another concern for policy makers -- the credibility of their new inflation-targeting strategy, announced with some fanfare just weeks ago. Breakeven rates -- which are market-implied expectations of the path of consumer-price inflation -- are headed lower again. The 10-year rate is hovering around 1.7%, as much as 10 basis points from its 2020 peak last month. That's well shy of the 2% inflation target for the decade to come, suggesting that investors need more evidence of the Fed's ability to put its words into action. Jefferies thinks the Fed is most likely to skew its asset purchases to longer-dated bonds. Alternatively, Chair Jerome Powell could signal it's buying more corporate bonds. ContrarianSince the last election has taught us to be wary of polls and look out for contrarian market signals, let us turn briefly to the high-yield market. Our reporter James Crombie points out that the energy sector has outperformed the broader asset class in this month's selloff, even as oil prices have tanked. That could be a sign of faith in a victory for President Trump, given that this is the corner of the junk bond market most likely to benefit from a second term. That said, energy is still down more than 10% year-to-date, the only sector to post a loss, amid a wave of bankruptcies and distress.  Junk bonds overall haven't exactly thrived throughout Trump's White House tenure. U.S. high-yield bond returns are running well below the average of 50% for each of the last eight presidential terms. The past four years have generated gains of just over 22%, the lowest since the second term of George W. Bush, according to Bloomberg data going back to 1983. Obama's first term was the most lucrative for high-yield bulls, returning well over 100% as the economy recovered from recession. The market does look on track to grow, however, as Bloomberg Opinion's Brian Chappatta notes. Ratings firm Moody's Investors Service released a report this week showing total debt from U.S. companies considered potential "fallen angels" leapt to a record high of $254 billion in the third quarter, from $217 billion at the end of June. Be warned, though, that the prospects for recovery on default at the lower end of the quality spectrum are miserable, as reported by Jeremy Hill and Max Reyes. Their story on the new era of U.S. bankruptcies noted that creditors are likely to be emerging from debt workouts with a few cents on the dollar, a far cry from the 40 cents they could claim in recent years. And this year so far has seen 199 bankruptcy filings by companies with more than $50 million in liabilities, according to data compiled by Bloomberg. That's the most for any comparable period since 2009. Encore, ECBAnd finally -- investors appreciate a straight talker. Christine Lagarde didn't mince words in Thursday's European Central Bank press conference: there's "little doubt" more policy action is coming in December, and the ECB will consider all tools. "Buy absolutely everything that isn't nailed down already," said Matthew Cairns, a strategist at Rabobank International. As usual, the party is in the peripheries, with Italian yields declining and Spanish and Portuguese bonds rallying. Traders have already pulled forward what had started to look like overly-aggressive bets on rate cuts, and money markets are now priced for the central bank to drop the policy rate another 10 basis points by June.  Societe Generale economists expect the ECB to deliver a package of 750 billion euros in additional asset purchases as well as a 10 basis-points rate cut and a new batch of targeted loans. The ECB's action can't come soon enough for markets roiled by a resurgence of coronavirus cases and fresh lockdowns. But it is disconcerting, to say the least, that the central bank has to reload its bazooka to prop up the economy, despite the fact that negative interest rates, a massive asset purchase program and several rounds of cheap loans have already deployed. Bonus PointsOdd Lots has the skinny on what to expect from rates markets heading into election day Melbourne's lockdown has lessons for the world, and Dr. Fauci has praise Trump's narrowing path to victory goes through Obama country Follow U.S. early voting stats Lost, confused? Try finding your way through this |

Post a Comment