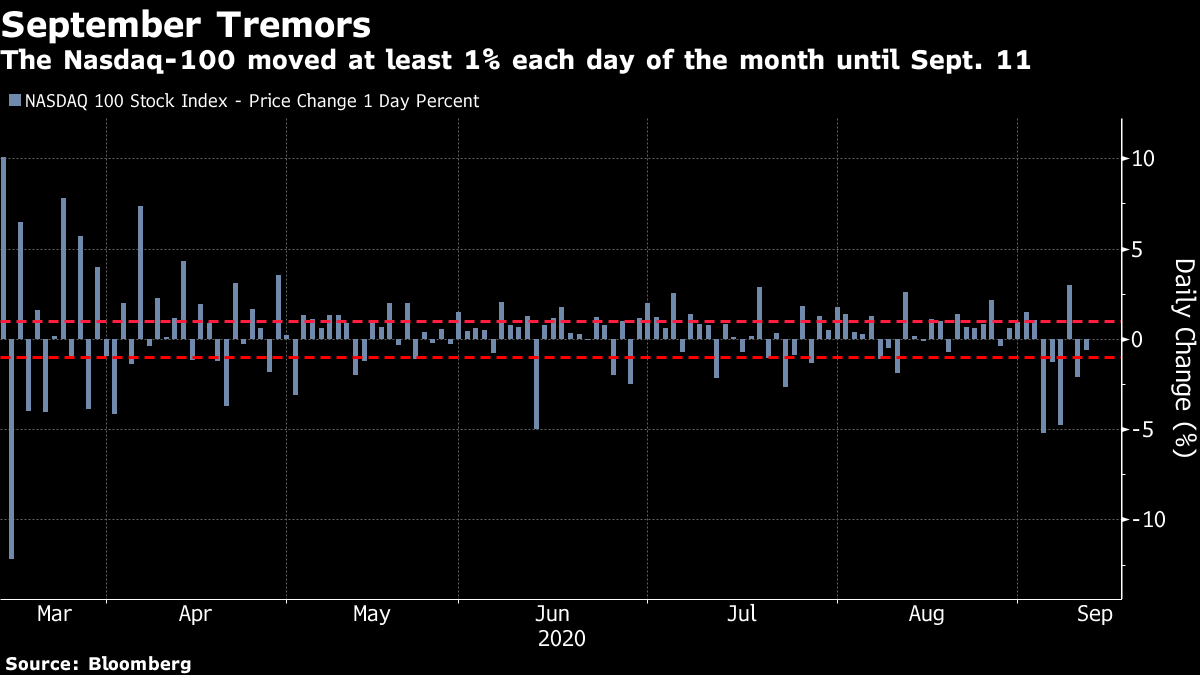

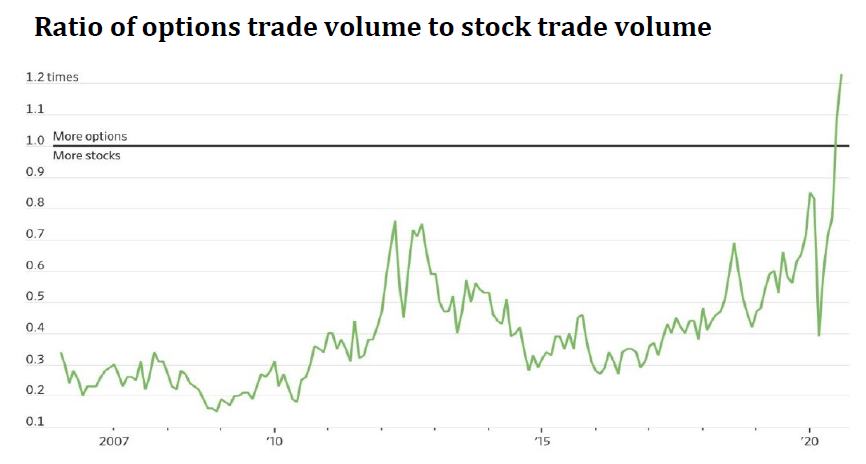

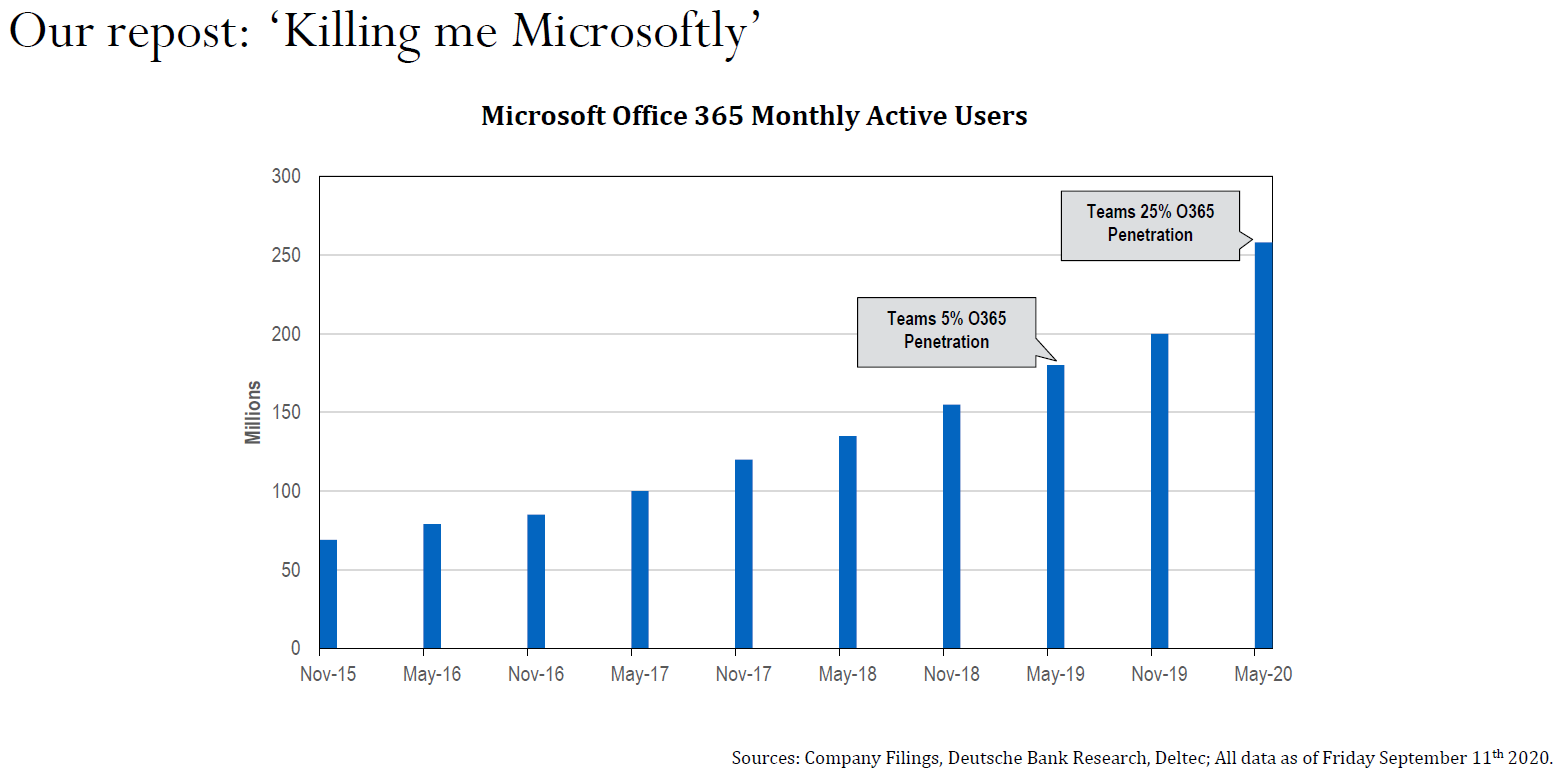

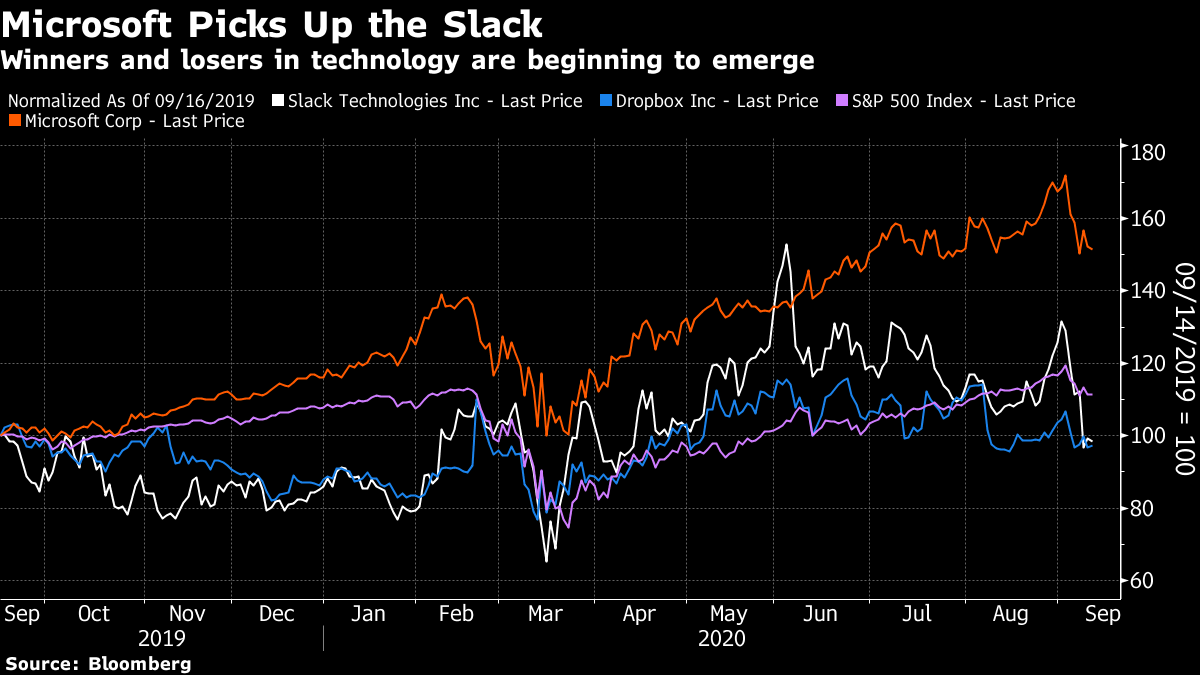

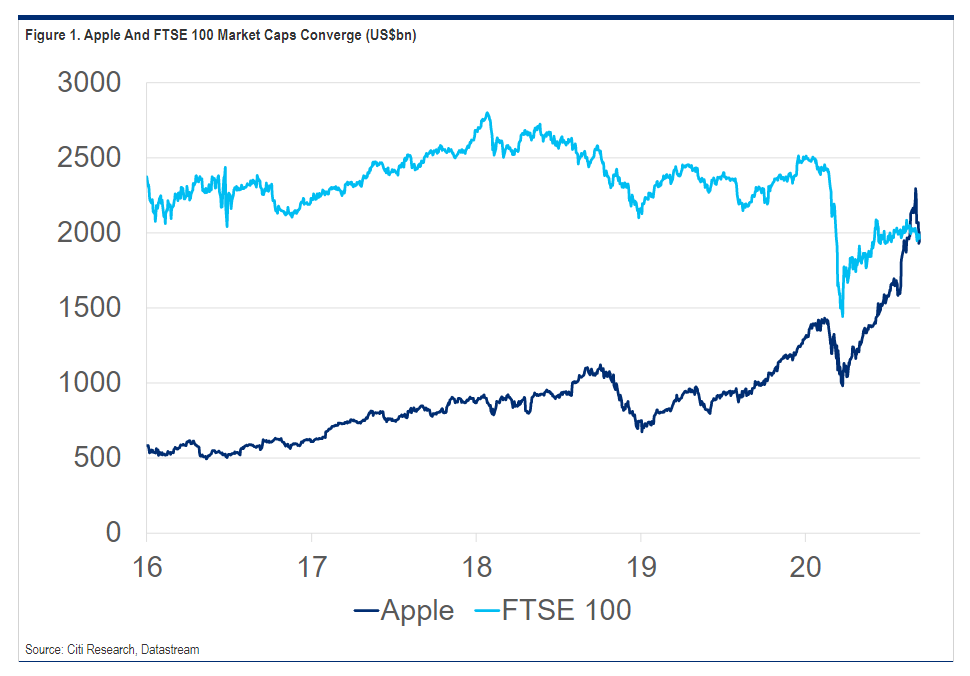

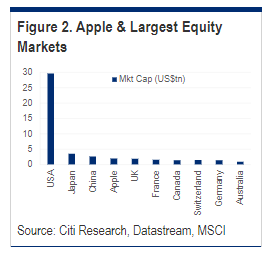

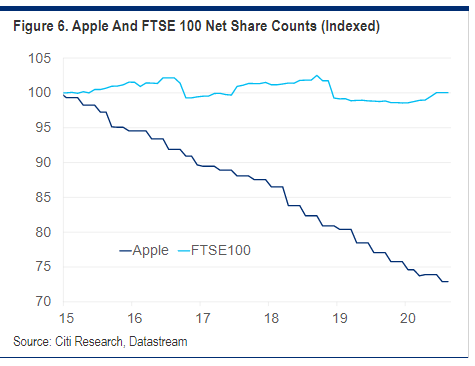

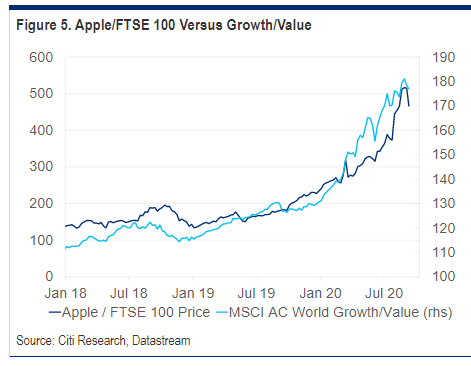

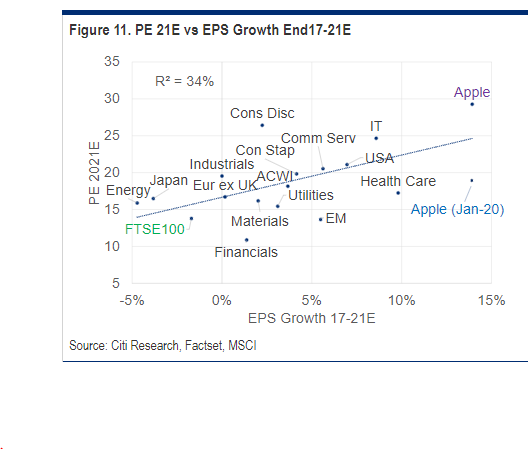

Don't Get Too Comfortable Is it safe to put a price on technology again? After great excitement, the solemn date of Sept. 11 proved to be the first trading day of the month when the tech-heavy Nasdaq-100 didn't move by more than 1%, in one direction or another:  It is just possible that a lot of speculation, largely placed by making bullish bets on individual stocks in the options market, has now unwound. However, it would be unwise to bet on it. As this chart from Deltec Bank & Trust Ltd. shows, trading in options has in the last two months outstripped trading in underlying cash equities for the first time on record. There aren't too many good precedents for this, then. It would probably be wise to assume that there are more shoes to drop before calm is restored:  The volatility and excessive speculation of the last few months are obvious. As with the great tech bubble 20 years ago, this is the unsurprising result when a lot of easy money meets a plausibly exciting narrative. But while trades have obviously been taken to excess, it doesn't necessarily follow that the entire market is overvalued. Resorting to some basic arithmetic on the cash flow generated by companies helps to draw some distinctions. Some stocks, such as Netflix Inc. or Tesla Inc., have an exciting growth story but are burning cash. Others, like Microsoft Corp. and Apple Inc., are turning into licences to print money, growing steadily and producing lots of cash. The latter are a better long-term bet than the former. In the following chart, also from Deltec, we can see the growth of Microsoft Office 365's monthly active users. It was doing very well before lockdown, and working from home has only sped the process, as more and more people have used its Microsoft Teams product:  Deltec therefore suggests threading a way through the tech mess by loading up on stocks that are producing strong cash flows and "winning" the battle to help everyone work from home, while shorting companies that are losing out to them. Examples include Slack Technologies Inc. and Dropbox Inc., which were lagging Microsoft heading into the crisis, briefly caught up in the rebound earlier this year, and have now dropped back to a point where they are lagging the S&P 500 over 12 months:  Rob Buckland, Citigroup Inc.'s chief global equity strategist, offered another way to crunch the numbers for Apple. Incredibly, the iPhone maker is now bigger than the FTSE-100, by market cap:  Indeed, Apple is bigger than every world stock market bar the U.S., China and Japan, according to MSCI indexes:  So, Buckland tries to decompose the valuations of Apple on the one side, and the FTSE-100 on the other. First of all, we discover that at the most basic level of arithmetic, Apple has been using all that cash to raise its earnings per share, by buying back stock — a phenomenon that Buckland himself christened "de-equitisation" about 15 years ago. The treasurers of the 100 biggest British-listed companies haven't been able to perform any such trick, and so over the last five years their share count has stayed static while Apple's has been cut by a quarter. It's that much easier for Apple to keep rising if there is always someone there (Apple) to buy on the dips:  Next, the FTSE-100 is now plainly a "value" stock, if treated in aggregate, and in current circumstances that isn't a good thing to be. The big U.K.-based multinationals include no big tech names, but lots of miners, energy groups, banks and tobacco. All of these sectors look cheap compared to their fundamentals, and in every case for good reason. As a result, a comparison of Apple's performance relative to the FTSE-100 with growth's performance relative to value over the last five years is startlingly similar. As a general rule, we can expect value to start to do well again when growth is no longer thought to be scarce, and when real yields are rising. In current circumstances, that is another way of saying that we cannot expect value to start doing well again until there is confidence that the pandemic has been decisively put to rest. And that is another way of saying that this pattern will endure for a while:  Finally, Buckland tried a very interesting exercise mapping the last five years' growth in earnings per share against forward multiples for Apple and the FTSE-100, along with a range of global sectors. As a general rule, higher growth should justify a higher price-earnings multiple, so it isn't surprising that there is a discernible relationship. The FTSE-100 has declining earnings, and a low multiple which, judging by the "best fit" that Buckland finds, leaves it slightly cheap. Meanwhile Apple shows up as having been notably cheap at the beginning of this year, but does look expensive now:  Assuming none of the big companies in the FTSE-100 can come up with a product as dominant as the iPhone any time soon, what can be done? Buckland suggests they are in a strange position where the market is prodding them to do almost exactly what politicians hoping for an economic recovery would prefer them not to do: Finally, what messages are markets sending to CEOs? Investors have significantly rerated Apple. Its out-sourced business model is very profitable but requires little capex. It employs remarkably few people, just 132,000. That's $15m of market cap per employee. Apple generates extraordinary levels of free cashflow which can then be used to buy back shares and enhance future growth rates. Alternatively, the FTSE 100 does a lot more capex, $108bn vs Apple's $8bn. Companies in the UK benchmark employ 4.6m people (so each employee valued at just $426k) and generates much more sales ($2tn vs $275bn at Apple). But the equity market has responded to the latest bout of QE by rerating Apple not the FTSE 100. This may encourage CEOs of the UK's biggest 100 companies to adopt more Apple-like business models, so shed employees and reduce capex. Policymakers should take note. Presumably, they want CEOs to do exactly the opposite. Note also that the new breed of ESG investors might also prefer them to move in this direction. The FTSE-100 is full of companies that don't tend to look good on ESG criteria, which favor big Apple-like companies that aren't labor-intensive and don't invest a huge amount in capital and equipment. Apple has reached the kind of valuation where it is no longer an obvious buy. Still, such companies should continue to do well — and that might not be helpful for hopes of a swift economic recovery, in the U.K. or elsewhere. That leads us to another repetitive issue for the U.K.: Brexit Is Back With a Bang For reasons best known to itself, the U.K.'s government has decided to start another fight over Brexit, the long-running saga of the country's decision to leave the European Union. By bringing a bill that would revoke parts of its agreement signed with the EU over how trade with Northern Ireland would be regulated after Brexit, and admitting that this would breach international law, it has brought back all the pathologies that dominated British markets and politics for all of last year. It has also enraged its counterparts in the EU, with which it has to negotiate a new trade agreement by the end of this year. In consequence, the pound has dropped toward the bottom of the range in which it has traded against the euro since Britain voted to leave in 2016:  Politically, there may be a judgment that being aggressive with the EU will show the working-class voters who flocked to Prime Minister Boris Johnson's Conservatives in last year's election that he is trying to fulfill his promises. The political logic is similar to President Trump's continuing attempts to build a border wall with Mexico, and spar with China. But there are serous issues here. As with the last tortured 12 months before the December 2019 general election, there are threats of rebellion from Conservative MPs over the government's announcement that it will deliberately break conditions on the treatment of trade with Northern Ireland agreed to less than a year ago. However, these aren't the same Conservative rebels who tried to stop Brexit from happening, almost all of whom are now out of the party, out of parliament, or both. Rather, opposition is now led by enthusiastic proponents of leaving the EU. For example, Lord Howard, a former Conservative leader said the admission that the government planned to breach international law were "words which I never thought I would hear uttered by a British minister - far less a Conservative minister." He added: "How can we reproach Russia or China or Iran when their conduct falls below internationally accepted standards when we are showing such scant regard for our treaty obligations?" This is strong stuff, and very relevant. The point of leaving the EU is that the U.K. can set itself up as "global Britain" and make new trade agreements with countries around the world, without having to go through the Brussels bureaucracy. Getting such accords with anyone will be much harder now that the government proposes to breach a vitally important trade agreement less than a year after a signing it. There may be some clever game theory going on; if so, it is an extremely dangerous game. As for the pound, a weaker currency might help a little to alleviate the problem of leaving a large free trade bloc. But if the British government really does go through with the strategy it is now advertising, the chances are that it will leave the bloc without a deal and therefore that the worst will finally come to the worst, in the eyes of the currency markets. If, as is perhaps on balance more likely, the forces of reason within Britain manage to force a climbdown and a messy compromise (which is how the current agreement on Northern Ireland came into being in the first place), then sterling is nicely positioned for a strong rise. Survival Tips Sometimes you have to admit defeat. I find the whole process by which it appears that Oracle Corp. is to end up owning TikTok so bizarre that I cannot come up with anything to say about it. Oracle is about helping productivity in the workplace, and TikTok is about diminishing productivity more or less everywhere. I don't see the synergy. Having failed to come up with anything in the way of worthwhile analysis, I can at least offer this guide on how to TikTok. Meanwhile, the worst thing about the whole episode is that it leaves no doubt at all that I'm getting older. The kids love TikTok. Whereas when I watch this highlights reel of great TikTok memes from quarantine, I feel more and more like my own grandparents. Maybe it's best to grow old gracefully. Have a good week. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment