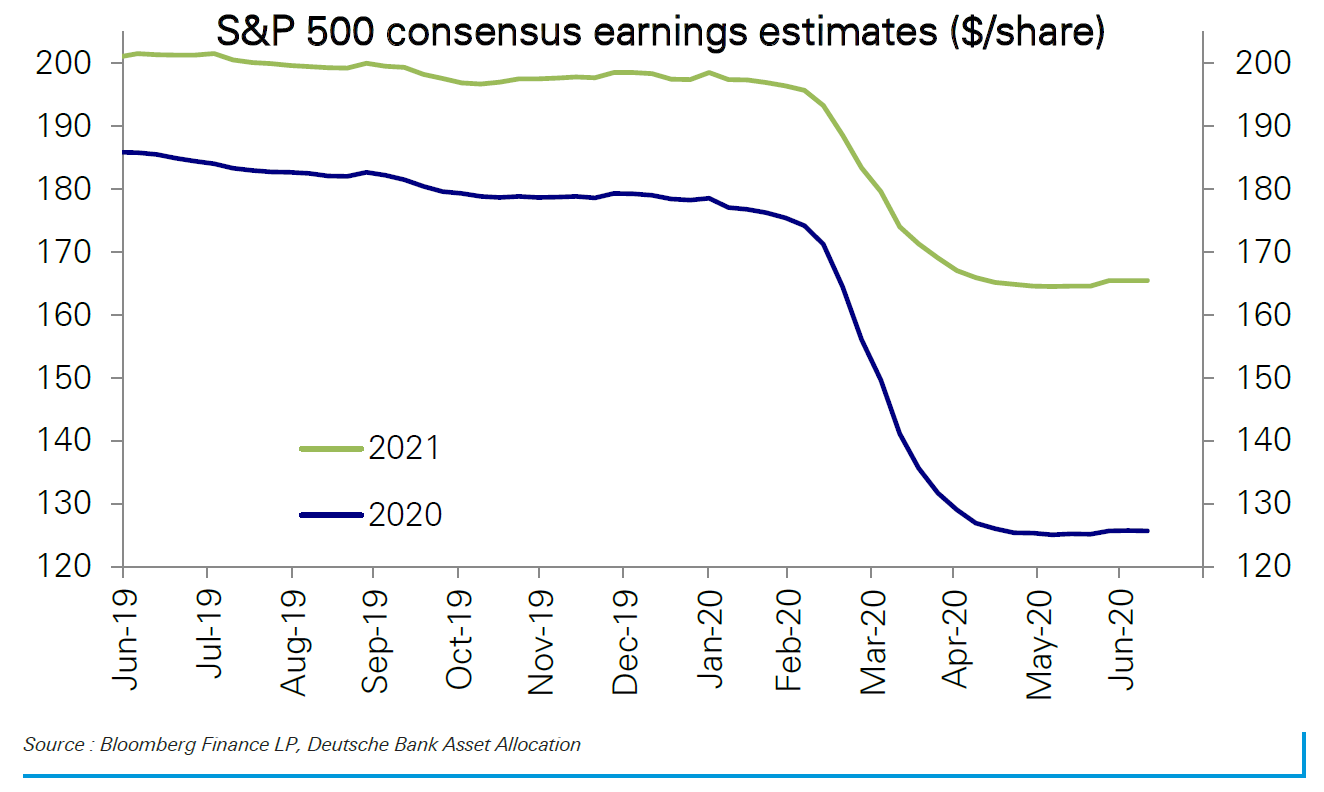

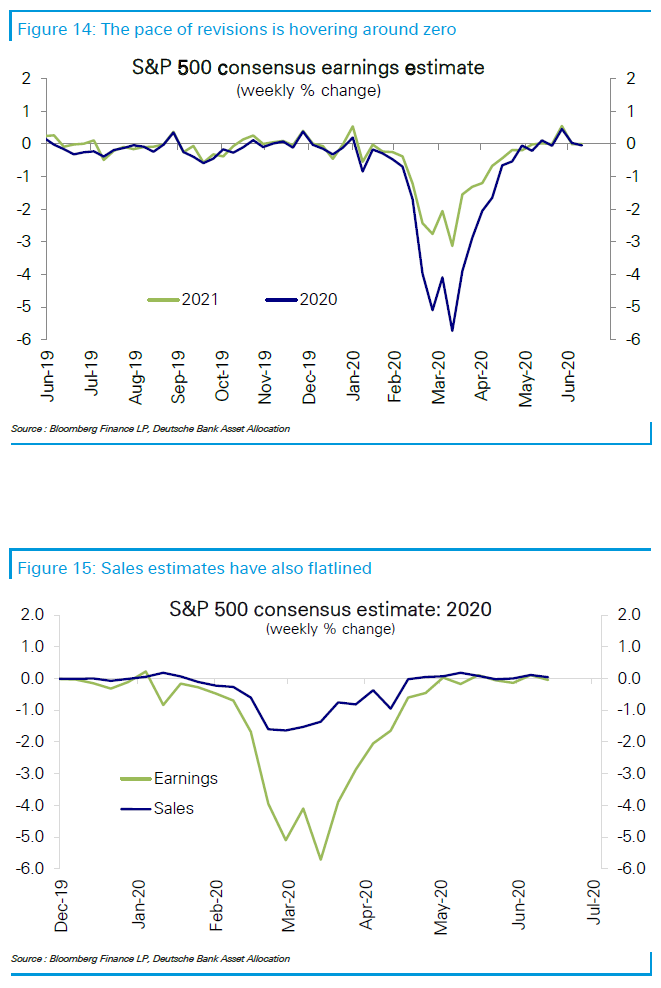

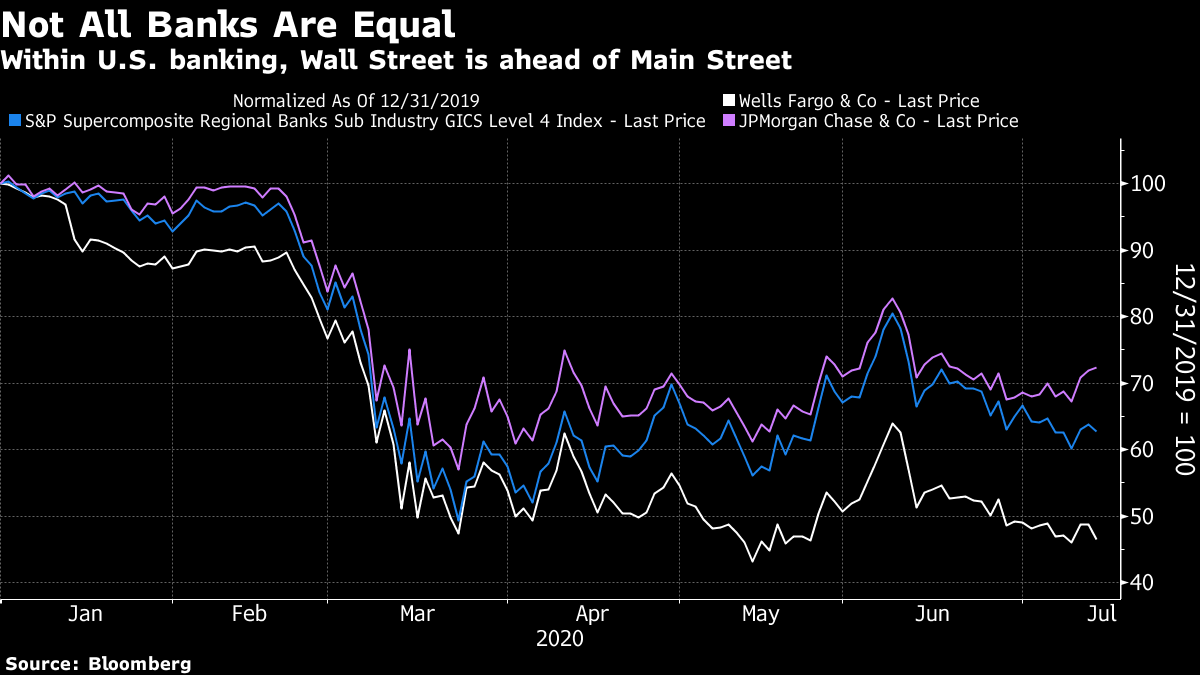

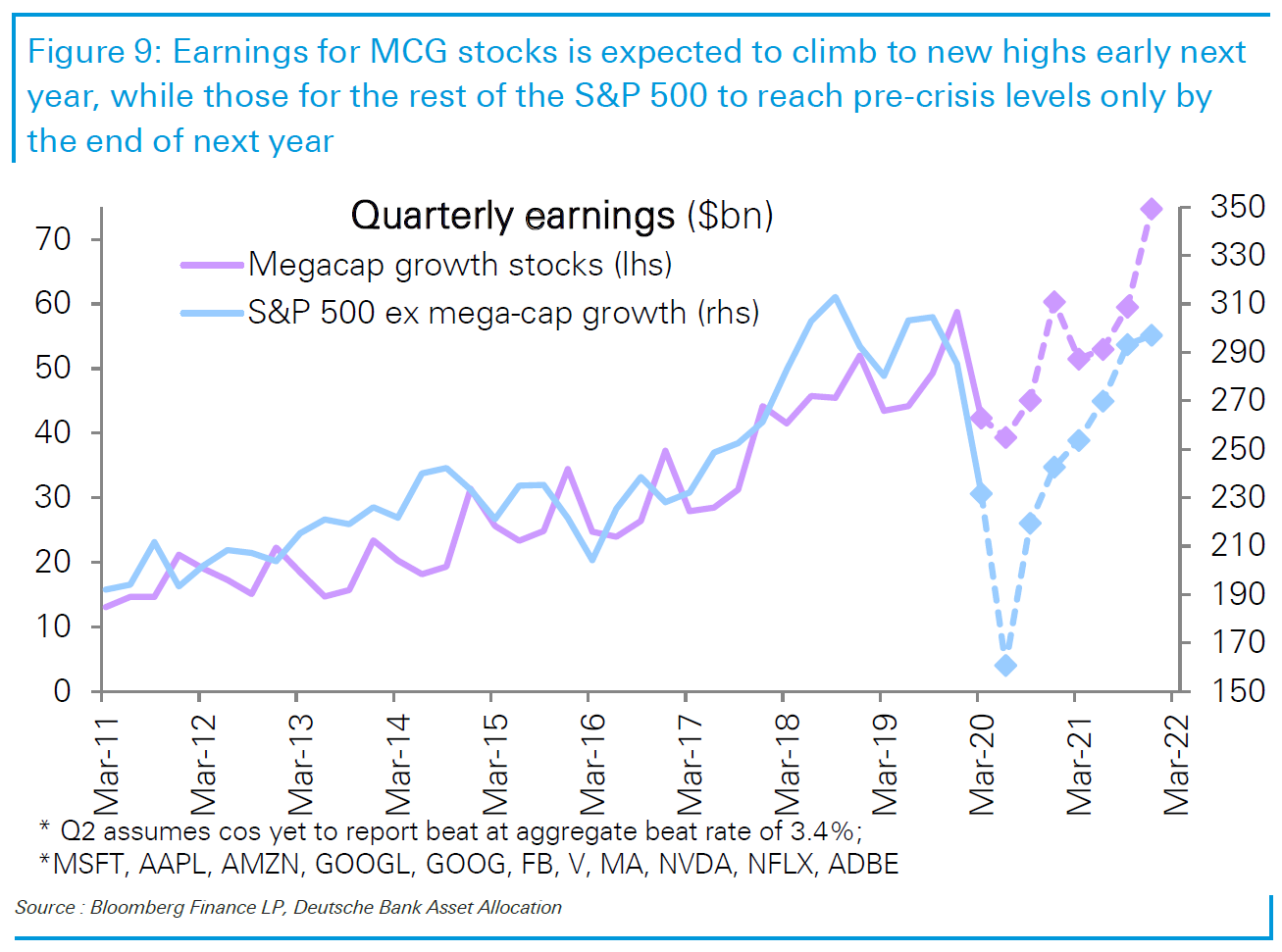

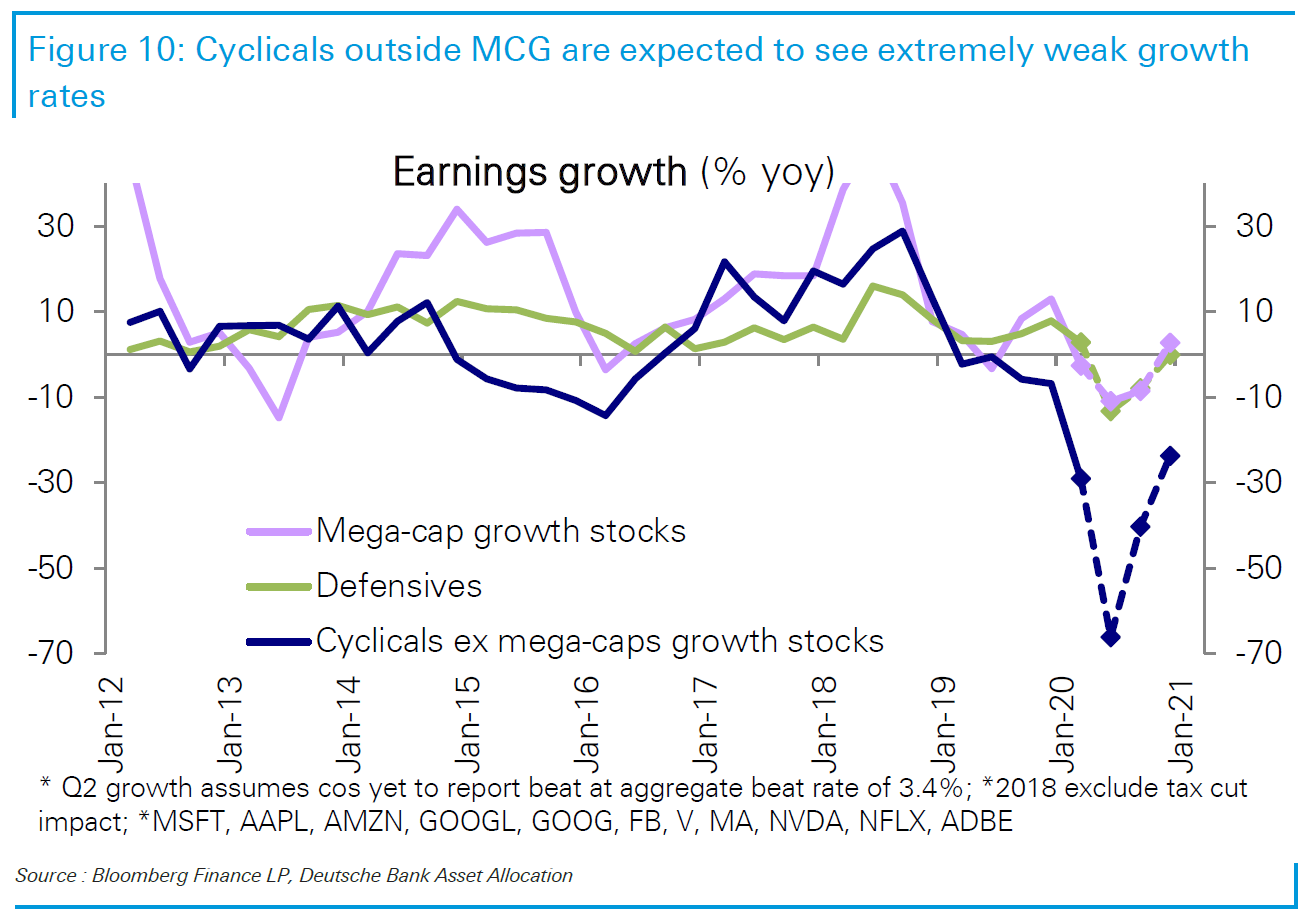

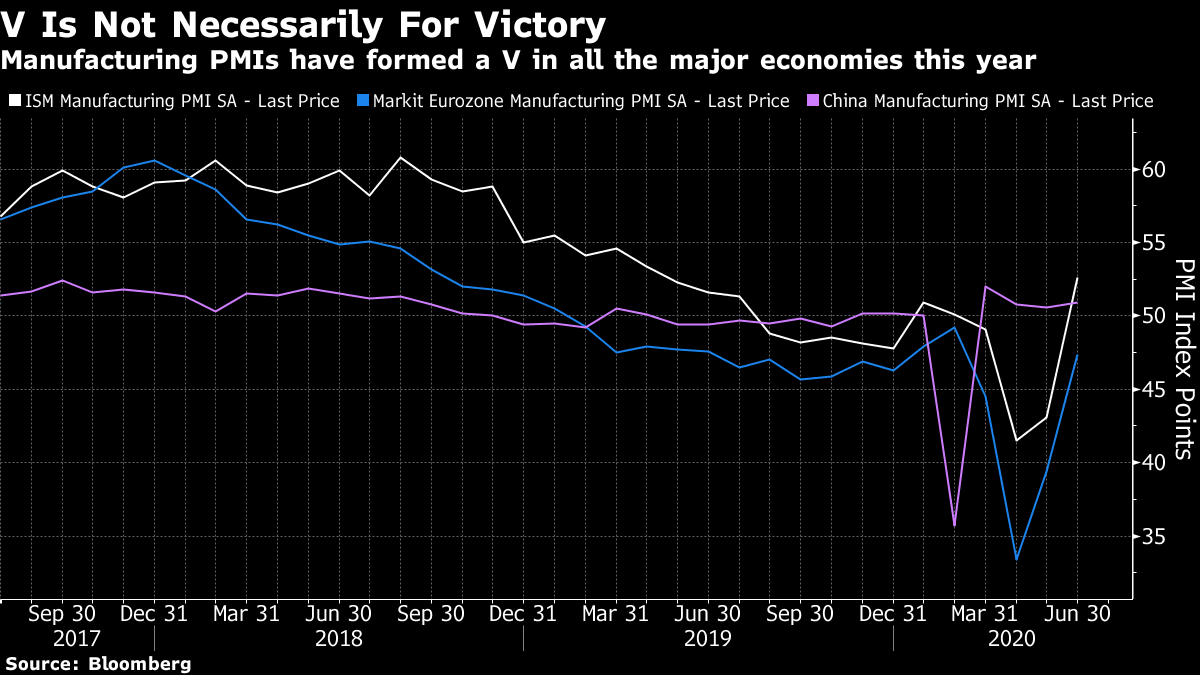

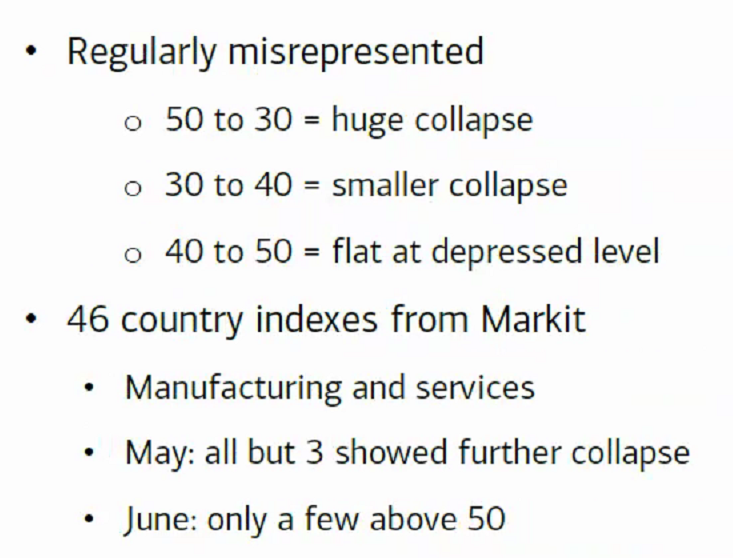

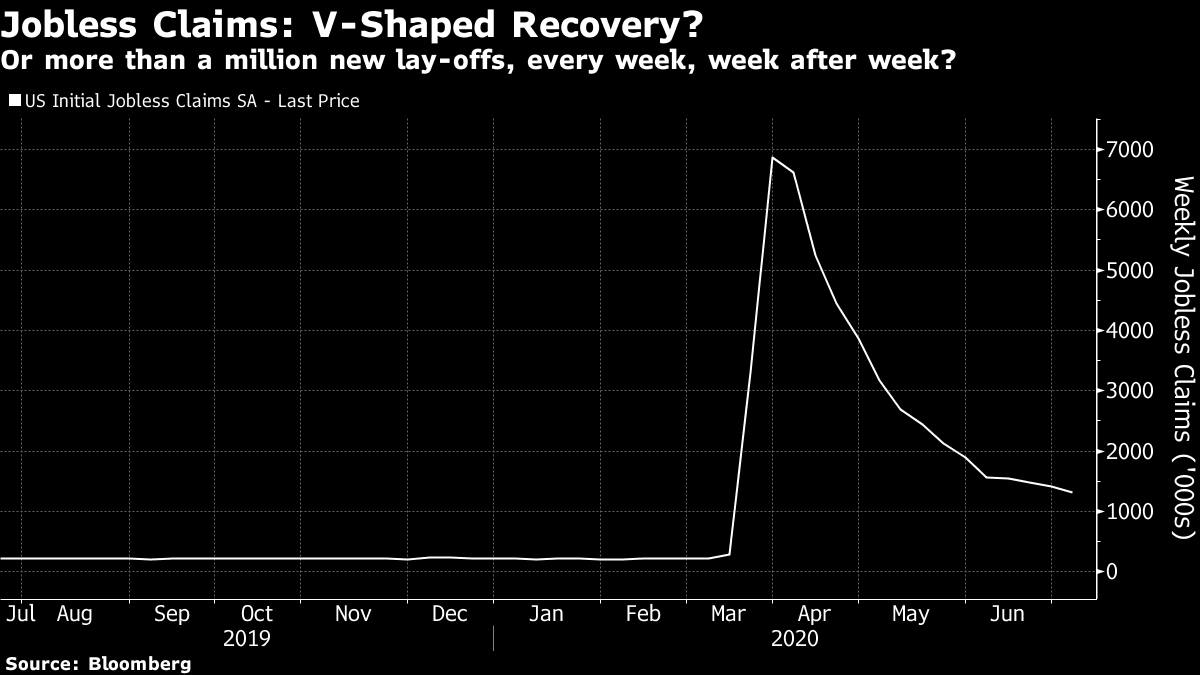

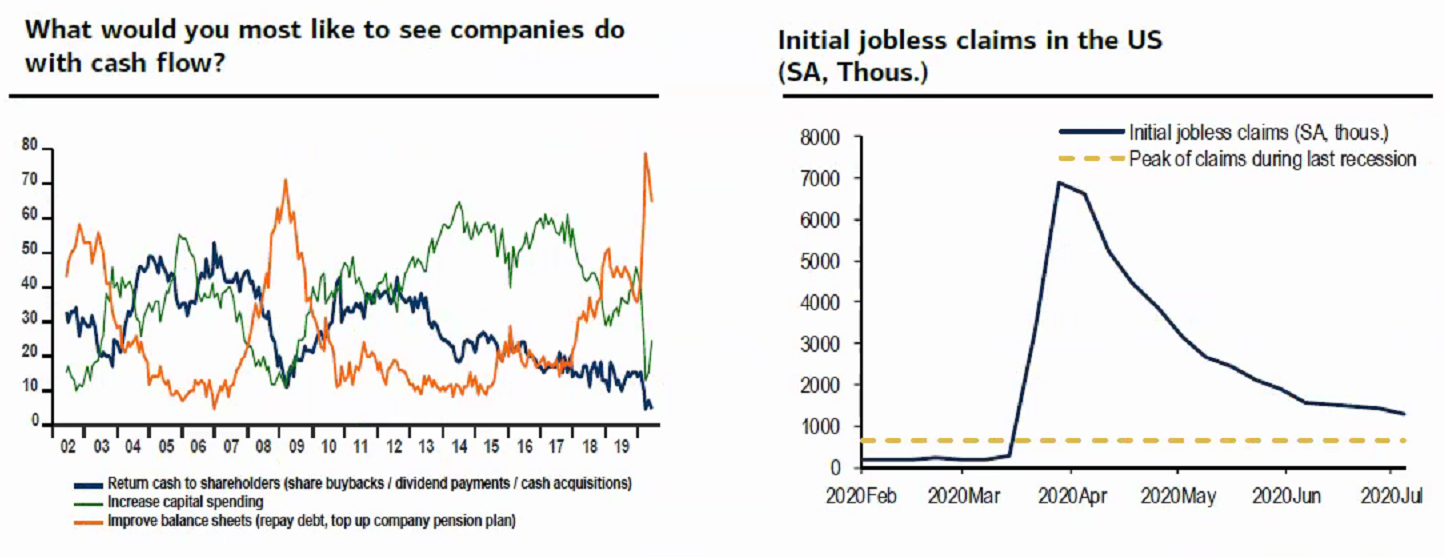

Let It All Sink In This has been one of those annoying times when far too many things happen at once. Should you be interested in the latest positive news on Moderna Inc.'s quest for a coronavirus vaccine, you can find the New England Journal of Medicine piece about it here . As Bloomberg News reported , it produced antibodies in all patients tested, so this is encouraging. That came out after the market closed, along with the news that 87-year-old Supreme Court Justice Ruth Bader Ginsburg is in hospital once again (news that might yet lead to profound political ramifications). We also now have confirmation that the U.S. has ended Hong Kong's special status and will treat it like mainland China . There will be sanctions on officials responsible for the clampdown in the city — a serious but expected development in the deterioration in the relationship between China and the West . Earlier in the day, the U.K. reversed course and cancelled plans to use Chinese telecoms equipment maker Huawei Technologies Co. for its 5G network. With news likely to come on all of these fronts, along with some potentially profound economic developments in the European Union by the week's end, people will have plenty of excuses to make whatever investments they want: buy, sell or hold. Judging by past performance, the Moderna news has a decent chance to swamp everything else, but don't bet everything on that. For the time being, let me focus on corporate earnings figures for the second quarter, and what they portend for the economy. We know they are going to be terrible. Given the extent of the shock that hit the global economy during the period, it will be difficult to gauge their terribleness with precision. Some gauge of the entire year is more meaningful, and the calls that accompany earnings announcements will give us much more of a clue about that. As this chart from Deutsche Bank AG's investment strategist Bankim Chadha shows, analysts effectively stopped trying to adjust their forecasts about two months ago:  There has been almost no change in earnings estimates for weeks, or in sales estimates for 2020:  Chadha suggests, very reasonably, that this should be interpreted bullishly. The stasis in earnings projections set in before the U.S. started to reopen its economy, and long predates increasing concerns about the end of lockdowns. U.S. economic surprises had never been so great and so positive as they were toward the end of the quarter. As brokers' analysts couldn't be bothered to update their forecasts then, we should therefore be primed for some positive surprises. Yes, the Covid news has grown much darker of late, and this may prompt managements to make more bearish forecasts — but the actual numbers should look solidly better than expected. One counterargument is the risk of "kitchen-sinking." Everyone and his dog expects this to be the worst quarter for corporate profits in living memory, and with good reason. So this is the time to whack everything possible into loss reserves, admit defeat on every embarrassing investment, and so on. We got a hint of that Tuesday as Wells Fargo & Co., the U.S. retail banking colossus still trying to rehabilitate itself after a mis-selling scandal, inflicted a loss on itself for the first time since the crisis year of 2008 thanks to a $9.5 billion provision for bad loans. The market punished Wells Fargo on the day, but if loan losses prove less severe than anticipated, those reserves could help make future profits look more palatable. Plenty of other companies will face similar decisions over the weeks ahead, which could make results that much harder to decipher. As it was, the market rose, taking its cue more from JPMorgan Chase & Co. — a Wall Street barometer that benefited from higher volatility — rather than Wells Fargo, a retail bank that's more of a barometer of Main Street. Investors are getting used to ignoring Wells Fargo, as the stock's performance so far this year shows, . Meanwhile, JPMorgan has fared somewhat better than the broader mass of U.S. retail banks, not all of which have Wells Fargo's baggage:  For the rest of the season, the critical results to watch will come from two groups: the acronym stocks (or Fangs) that enjoy huge market capitalizations and are viewed as immune to the Covid disaster; and the most cyclical industrial groups, which are viewed as most exposed. The Fangs are expected to deliver decent results, and it would be a major blow if any of them fail to do so; while the cyclicals will probably give the best evidence of the near-term trajectory of the world economy and stock market. Chadha illustrates this nicely. The Fangs are forecast to produce results barely dented by the pandemic for the second quarter, and to be back at a high by the end of the year. The rest of the S&P 500 will be forgiven if it still isn't back to peak earnings by the end of 2021:  He may well be right that the cyclicals have been given an easy bar to clear. In the following chart, Chadha breaks down expectations further. For the next year or so, the Fangs are predicted to produce earnings growth exactly in line with traditional defensive stocks, which gives a good clue as to the expectations surrounding them. Investors think they are defensive on top of all their other wonderful attributes. Meanwhile, cyclicals excluded from acronyms are expected to have a torrid time:  These two groups will matter most for differing reasons. We need to know whether the Fangs are really defensive; and from the cyclicals, the market wants to know how bad the damage from the pandemic's recurrence in the U.S. will be. If they can resist throwing the kitchen sink at a bad quarter, the market is hoping that they will validate the positive feeling engendered by the now somewhat dated macro surprises. But that leads to another issue: Levels vs. Changes Amid rapidly changing economic conditions, it is easy to see things that aren't there. In particular, it is easy to over-interpret dramatic changes. Indeed, the effect of the pandemic on perceptions may have rendered some of the most deep-rooted and trusted economic data unreliable. That was the bottom line of a presentation by BofA Securities Inc.'s chief economist, Ethan Harris. The measure he looked at is the Purchasing Managers Index, or PMI, published at the beginning of each month in a range of different countries and over history a very good leading indicator. In the U.S. and elsewhere, it has been as V-shaped as it gets:  The spike in PMIs has naturally spurred confidence in a V-shaped economic recovery. The problem is this isn't what they show. In fact, the PMIs are alarmingly bad; so bad that they may have developed a flaw. The question supply managers are asked is whether conditions are better or worse than they were the previous month — not, importantly, compared to the average or the beginning of the year. After the sudden stop seen in many states in the U.S., it is very surprising, and positive, that the PMI never dropped below 40. But given that the lockdown conditions started easing many weeks ago now, the great majority of companies should have found June much better than May. The fact that the PMI only just got above 50 in the U.S., and is still below that level in the euro zone, is therefore consistent with an economy bumping along the bottom. Despite the V-shaped recovery in the PMI itself, the continuing reading of barely above 50 suggests an L-shaped economic recovery. This is Harris's own summary of what we should take from recent PMIs:  This in turn seems very strange, however. Activity is plainly returning, and is greater than it was at the lows in March and April. We might not be bouncing back as fast as some say, but it is very hard to believe that the PMI for June should correctly have been put below 50 in most of the world. Harris suggests that the supply managers taking the survey may themselves be confused, and comparing current conditions with the norm, or with last year, rather than with the previous month, and that therefore a strong economic leading indicator may now be less reliable. For an example of a measure of a level, rather than a change, which is also being misperceived, try initial jobless claims. Our first and natural response to the following chart, which shows weekly claims over the last 12 months, is that it shows an inverted V:  That is true, but bear in mind that this a flow statistic, not an absolute level. Claims were stable at a low level before ballooning very suddenly with the beginning of the lockdown period. What this chart shows is that each week since then, at least a million new people have been laid off. That number has reduced each week, which is good. But it is a measure of flow, and shows that the increase in joblessness remains heavy. Harris adds as evidence of continuing concern that investors in BofA's monthly survey of fund managers are still overwhelmingly asking companies to put any cash flows they have toward fixing balance sheets rather than investing for the future.  Combine this with the fact that weekly jobless claims are still running at a higher rate than they did at the peak of the last recession, and his point that data are being misread appears well made. Just as the initial sell-off was unduly extreme, belief in the rebound rests as much on optical illusions and misperceptions as on reality. Survival Tips Photography is an under-appreciated art. Many great photographers did their best work in Mexico, much in my thoughts at present, where the light is virtually perfect. So if you want to look at images far more worthy of your attention than the charts I hurl at you, try some of the masterpieces of Manuel Alvarez Bravo, Tina Modotti, Edward Weston or a contemporary street photographer proudly continuing their tradition, Keith Dannemiller. His 2016 exhibition Callegrafia made contemporary Mexico City come alive like nothing else I have ever seen. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment