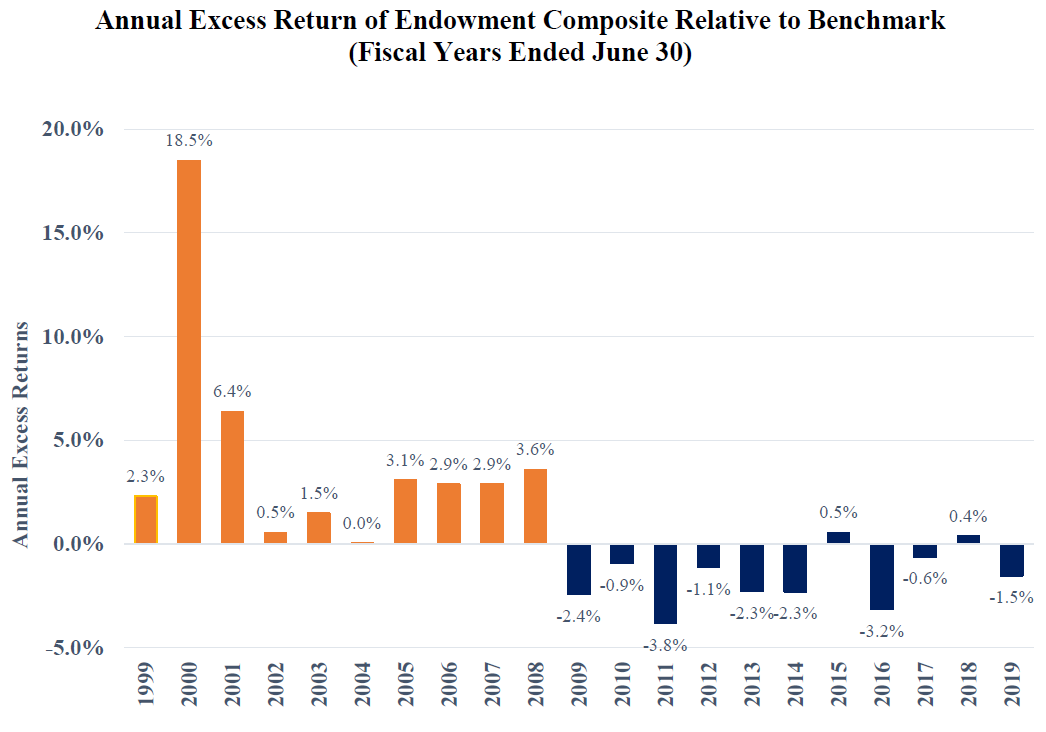

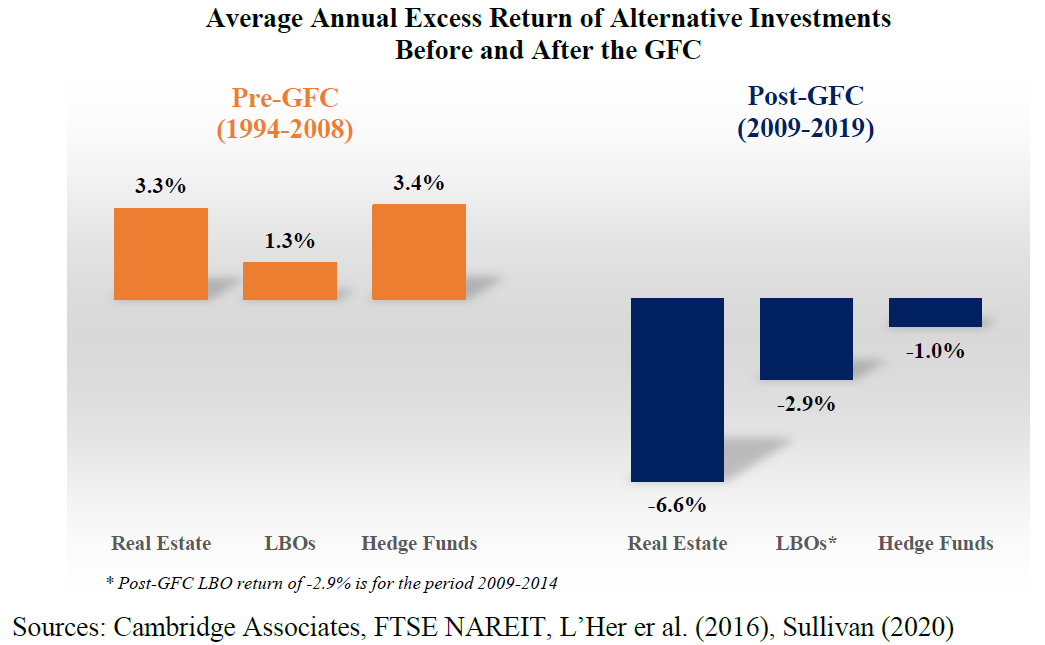

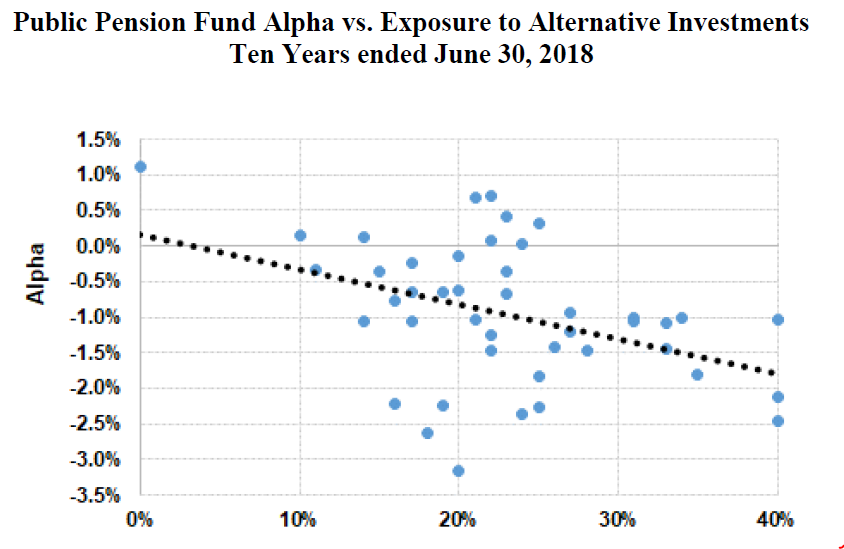

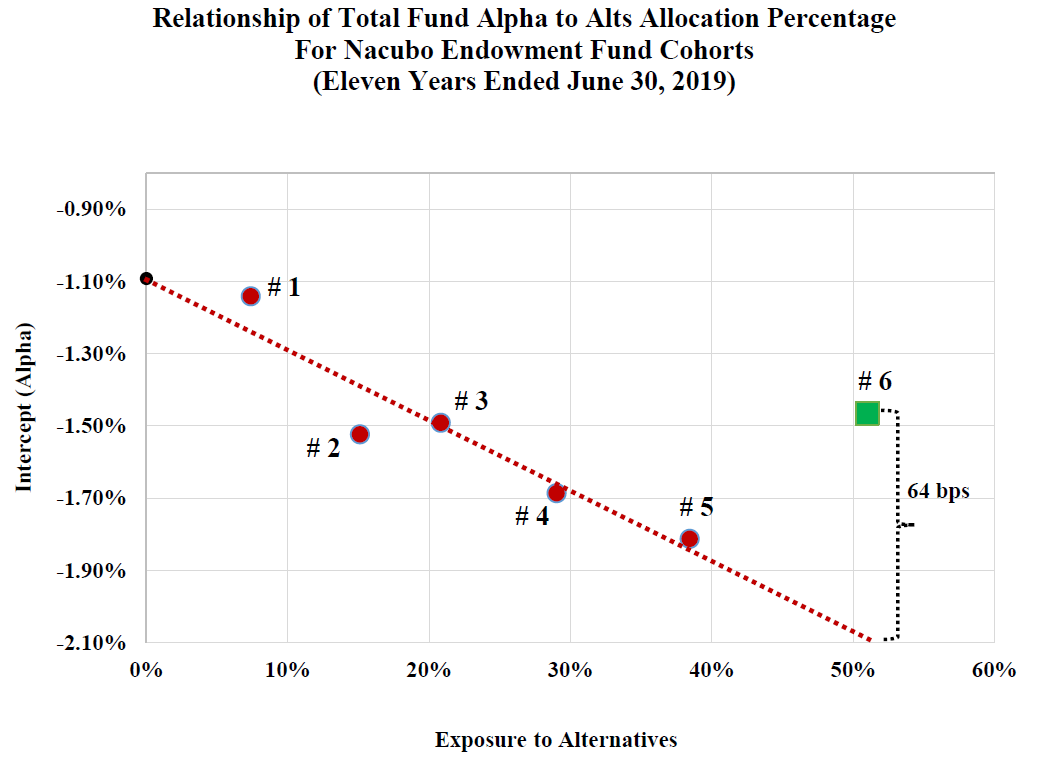

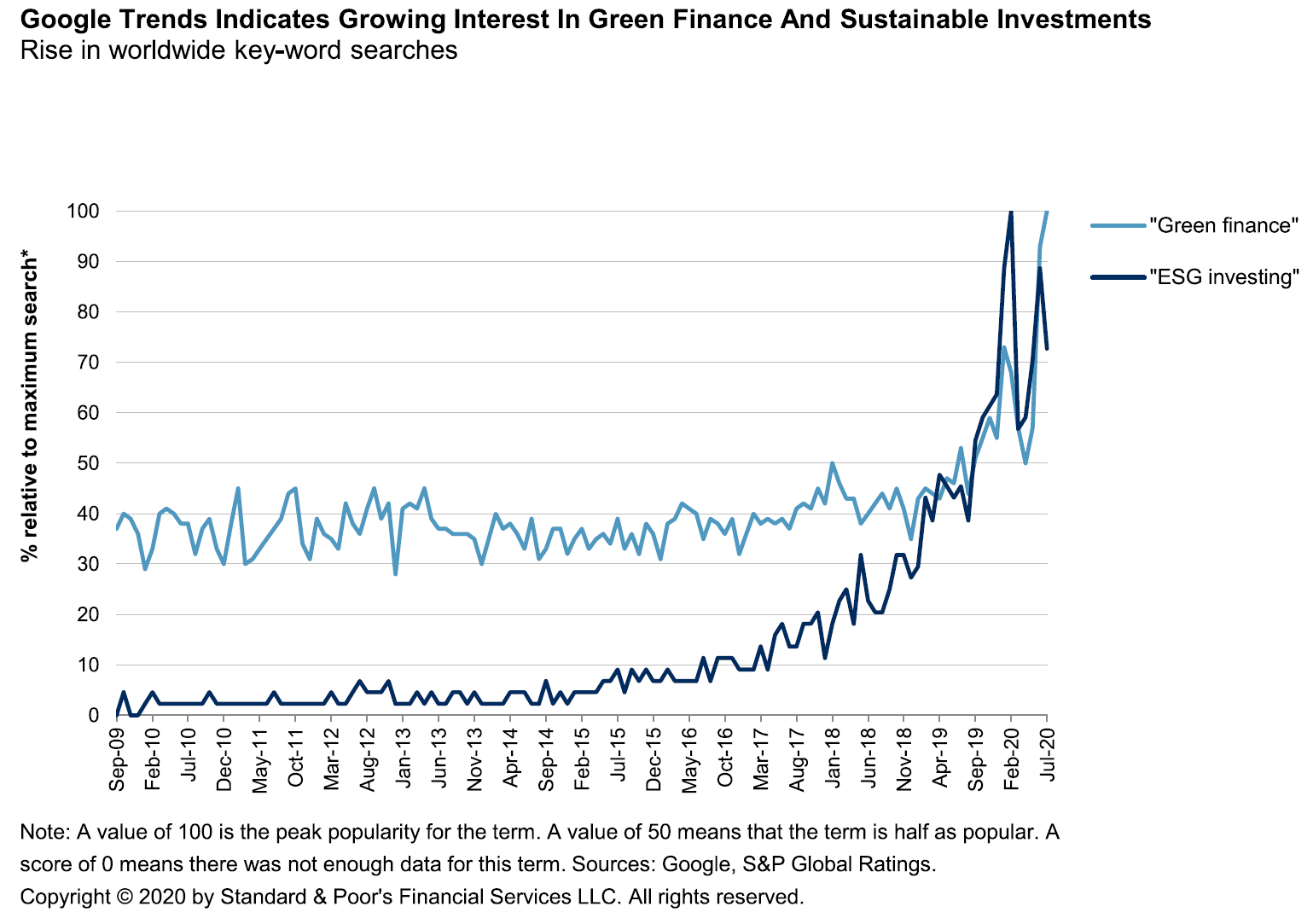

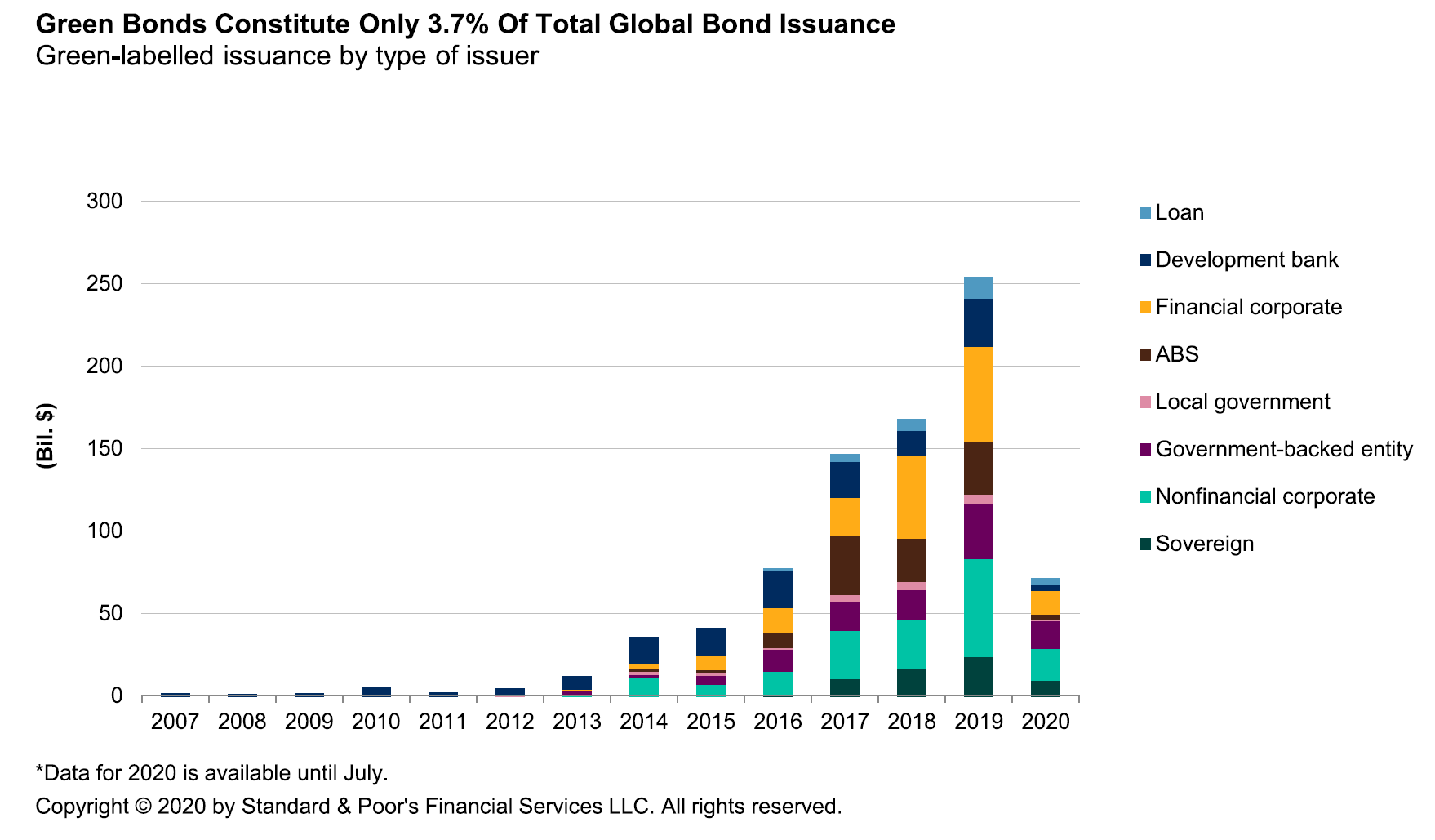

Assume a Vaccine There is an old joke about economists, and how badly they compare with real scientists. A physicist, a chemist and an economist are shipwrecked on a desert island, with nothing to eat, other than a crate of tins of baked beans which has also washed up on shore. But there is no tin opener. What to do? The chemist suggests leaving the tins to soak in the water until the metal erodes. The physicist wants to heat them up until they burst open. Then comes the economist's turn: "Assume a tin opener…." Economists produce great models on the basis of interesting assumptions, but they don't necessarily match conditions in the real world. We can all work out that a tin opener would help. The point is to produce one. By the same token, a number of optimistic commentary underpinning markets at present seems to be based on a new premise: "Assume a vaccine..." That at least is what appears to be going on as the S&P 500 posted a new Covid-era high, putting it in positive territory for the year, only to give it up again within minutes. The action in the index over the last three days both demonstrates the importance of psychological landmarks for markets, and the possibilities of vaccines. The end-2019 level is marked in red:  Two separate vaccine stories justified the early excitement. Moderna Inc. reported positive results for its latest phase of tests, while Robert Peston of ITV News in the U.K. said there would also be good news to come in The Lancet on the vaccine being developed by Oxford University. Naturally, any positive development is beneficial for us all, in ways that go far beyond financial prices. But there is a reason why research like this is usually carried out in the relative privacy of academic journals with an intense peer review process. The information is technical, and it comes nowhere close to proving that there is a vaccine ready for us all to take any time soon. There are also reasons to question how effective any vaccine can be. Immunity might not last long. That at least was the implication of this study from King's College, London, reported here, which found steep falls in patients' antibody levels within three months of infection. Meanwhile, accounts of patients who have already had Covid-19 suffering it again call into question whether the pandemic can be trusted to die down once "herd immunity" has been achieved. Beyond that, the call by a group of world leaders for "vaccine equity" should be a reminder that discovering a workable vaccine is only the first step. There was enough difficulty earlier in the pandemic when it came to sharing out mundane items like masks, gowns and ventilators; that is as nothing compared to the challenge of distributing a vaccine, for which the demand will be global, and on which the inventors will reasonably expect to make a profit. Note finally that there is a reason why the process of developing a new vaccine tends to be slow and drawn-out. It has to be. The intensity of pressure for an early vaccine, and the scale of the money at stake, heightens what many public health workers regard as the true "nightmare scenario" — a botched vaccine, that goes out before it is ready, has side effects, and convinces the public that the anti-vaccination movement was right all along. That's a disaster scenario. Piecing together all of this evidence to work out how long it is likely to take before we can distribute a vaccine capable of ending the outbreak is a feat beyond anyone in the field of pharmaceuticals or public health, and there is certainly no way normal financial investors can undertake that task. It remains good news if vaccine development proceeds well. But pressing "buy" every time a piece of unreviewed academic research comes out isn't a good idea. Do this, and the chances are that you create an opportunity for someone else, not yourself. The Endowment Effect Looking to the longer term, the chances are that this crisis will have some winners to go with the losers in the investment world. University endowments often give us a handle on the future, and they suggest problems for alternative assets. Led by Yale University's endowment under its Chief Investment Officer David Swensen, the big U.S. colleges moved into alternative assets, such as private equity and hedge funds but also esoterica such as farmland, forestry and litigation finance. The logic was that it was hard to do better than the market if that market was liquid and well understood, but there might be opportunities in less liquid places. This policy did spectacularly well for a while, turning Swensen, who suggests that retail investors should restrict themselves to index investing, into one of the world's most famous money managers. The returns of the biggest endowments have looked lackluster of late. Now, an excellent research paper by Richard Ennis, which can be found on SSRN here, shows that there was a clear turning point, that came in June 2008 — the eve of the GFC. Ennis builds a composite of 43 major U.S. college endowments, and maps how they did each financial year (ending in June to match the end of the academic year) since 1999, compared to a simple benchmark based on stocks and bonds. They did far better than the benchmark in the first decade of this century, with massive outperformance as the dot-com bubble was bursting. And they have done terribly compared to the benchmark, with only minor respites, during the post-crisis decade.  A culprit can be found easily enough. Real estate, LBO funds and hedge funds did fantastically in the years to 2008, compared to stocks, and have done worse ever since:  Ennis also charts the "alpha' (the degree of outperformance of a basic market benchmark) recorded by public pension funds since the crisis. They have increasingly tried to follow the lead of endowments into alternative assets. The numbers suggest that so far, at least, they shouldn't have. The higher the exposure to alternatives, the worse the performance:  Ennis's paper is worth reading in full for anyone interested in endowments or alternative assets — as is this excellent summary of his findings by Larry Swedroe. For now, one last chart gives important extra detail. Using data from the National Association of College and University Business Officers, endowments are divided into cohorts by size. The first is the smallest, and each successive one is bigger. In general, the relationship is clear: As endowments get bigger, their weighting in alternatives increases, and their returns get worse. But there is an exception:  The really big endowments managed to do better than anyone else bar the smallest, despite a massive anchor-like weight in alternatives. This could imply skill. The people who run the largest university endowments tend to be intimidatingly intelligent. It might also imply some kind of first-mover advantage. Maybe Swensen and the other early movers established relationships with good private equity and hedge fund managers, and can use their size to get better terms. Or put differently, there was a great opportunity in alternative investments about a quarter of a century ago, and Swensen and others saw it and took it. All the best investors are opportunists. Doubtless this crisis is also creating an opportunity somewhere. It's worth watching the endowments to see if they spot it before the rest of us. Silver Linings The last great set piece of this week will come when European Union leaders meet for a summit to thrash out a plan for a post-Covid development fund. Whether or not this a true "Hamilton moment," it is an exciting opportunity to bring Europe closer to a workable common fiscal policy. At stake are much the same notions of sovereignty that animated the debates around the founding of the U.S. Meanwhile, an intriguing report from Standard & Poor's, available here to S&P Capital IQ subscribers, suggests that one side effect of any development fund could be to super-charge the availability of low-risk green bonds. As this chart from the study shows, interest in and appetite for green finance, in which bonds would specifically support environmentally friendly infrastructure, has increased dramatically during the crisis:  This means that the EU could find it much easier to raise finance for its proposed recovery fund if some of the money can be labeled as "green" or "ESG." And that is exactly what is planned. To quote S&P: The EU is intending to use its post-pandemic recovery plan to reinforce its fight against climate change. About 30% of the "Next Generation EU" 750 billion euro fiscal plan to aid the post-Covid-19 recovery would target climate-friendly projects, according to European Council President Charles Michel's latest proposal. This translates to a potential of 225 billion euros of additional green financial instruments, refinforcing the EU Green Deal's pledges. The effect of 225 billion euros ($257 billion) on the green bond market would be enormous. It would greatly expand issuance, but also give it a backbone of "safe assets," underwritten by a strong sovereign, that could help broaden demand:  There are many reasons to hope that the EU can thrash out a workable recovery fund over the next few days. The possible side effect of a big boost for financing green infrastructure is one of them. Survival Tips Podcasts can be great for your sanity. I'm often asked for recommendations. So here are some of my favorites that aren't directly about markets and investing. I enjoy Cautionary Tales, a series of narratives about disasters and what we can learn from them, including dramatizations and special effects, which is fronted by former colleague Tim Harford. In the same vein, and from the same stable, Against The Rules is the venture into podcasting by the peerless financial journalist Michael Lewis. The first season focused on diminishing respect for referees, while the most recent is on the importance of coaching. I like Talking Politics, in which a group of academics at Cambridge University interrogate the most important problems facing the world with wry humor and great intellectual rigor. Their subjects also range into economics and culture. Further off the beaten track, The Last Days of August is a minutely researched and sensitively told attempt to explain why a successful young porn star took her own life in 2017. Finally, time to declare an interest and suggest this podcast is a "must listen." The immense accounting scandal at Germany's Wirecard AG was first revealed several years ago by my former colleague from the Financial Times's Lex column, Dan McCrum. He has been subject to immense pressure, including an investigation by the German financial regulator. At present, he is taking a well-deserved victory lap, and spends 20 minutes or so in this podcast recounting the whole extraordinary story. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment