America expands testing, Hong Kong dollar-attack plan met with skepticism, and gold tops $1,800. Another turnThe recent U.S. trend of the coronavirus spreading among young people while the death toll drops could soon reverse. Yesterday set new records for infections and deaths across the U.S. as the Trump administration began the process of leaving the World Health Organization. The federal government has responded by ramping up testing in Louisiana, Texas and Florida as health officials try to get a firmer grasp on how the pandemic is evolving. Germany saw the infection rate drop further, Beijing reported no new cases for a second day and Tokyo saw new infections slow. Dollar attackSome of President Donald Trump's aides are reportedly looking to undermine the Hong Kong dollar peg to the U.S. currency to punish China for recent moves to reduce freedom in the former British colony. The idea has been met with skepticism from traders and analysts who think it would be difficult to implement and would probably risk hurting U.S. interests at least as much as China's. There was little reaction in the currency market with the Hong Kong dollar remaining at the strong end of its range, while the Hang Seng Index closed 0.6% higher. One impact was felt in the price of HSBC Holdings Plc which dropped more than 4%. Crude goldGold spot prices rose above $1,800 an ounce for the first time since 2011 this morning as investors continue to favor the traditional haven. Flows into bullion-backed exchange traded funds have already topped the full-year record set in 2009. In the dirtier, if significantly more useful, world of crude oil, today's U.S. government inventories report is expected to show stockpiles swelled. That, coupled with continued demand concerns over the lingering threat from the coronavirus, means prices remain stuck in a holding pattern close to $40 a barrel. Markets slip againWednesday is seeing a continuation of the drift lower in stocks as the route to the full reopening of the U.S. economy remains unclear. Overnight, the MSCI Asia Pacific Index slipped less than 0.1% while Japan's Topix index closed 0.9% lower. In Europe the Stoxx 600 Index was down 0.7% by 5:55 a.m. Eastern Time with banks the biggest drag on the gauge. S&P 500 futures pointed to a small loss at the open and the 10-year Treasury yield was at 0.648%. Coming up...U.S. crude inventories data is published at 10:30 a.m. Atlanta Fed President Raphael Bostic is the sole monetary policy speaker today. President Trump holds a press conference with Mexico's Andres Manuel Lopez Obrador later. The Supreme Court will issue its final opinions of the current term. Bed Bath & Beyond Inc. reports earnings. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Joe's interested in this morningHere are two charts that perfectly symbolize the maddening contradiction of the market right now.

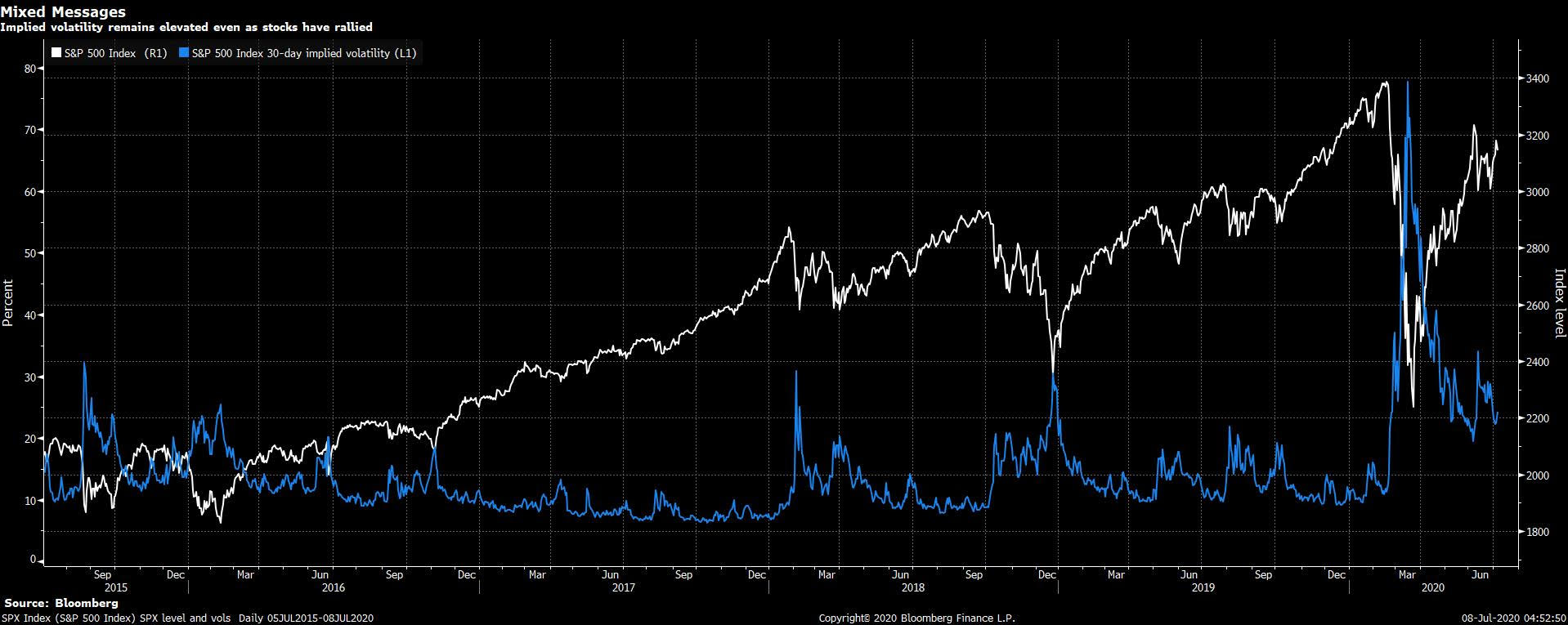

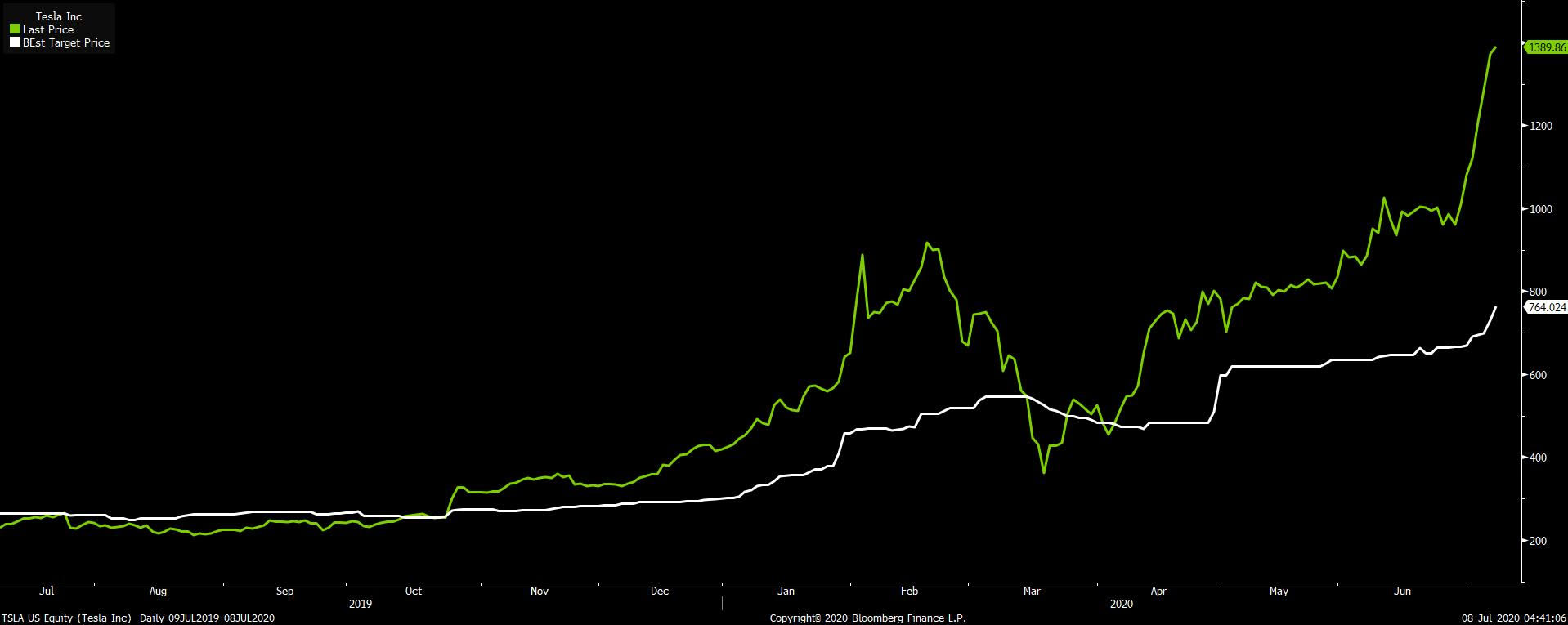

The first comes from Yakob Peterseil, which shows that even as the stock market has absolutely soared since late March, the VIX remains quite elevated. In other words, despite the huge rally, people main extremely anxious. As you can see, the gauge is still at levels that would be near the peak of the last give years (excluding this spring).  Ok, so people are nervous. But they're also euphoric? As Joe Easton and Esha Dey note, Tesla's stock is just blowing past analyst estimates every day. It's surreal. Wall Street analysts have a price target on the stock north of $700, and yesterday it hit nearly $1400.  Just to drive the scale of the Tesla rally home, not only has it soared past analyst expectations, but the stock has added the combined market value of GM, Ford, and Fiat Chrysler in just the last week.

Is this a market characterized by excess pessimism and fear of the next shoe to drop, or by wild-eyed exuberance? You can make any argument you like.

Joe Weisenthal is an editor at Bloomberg. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment