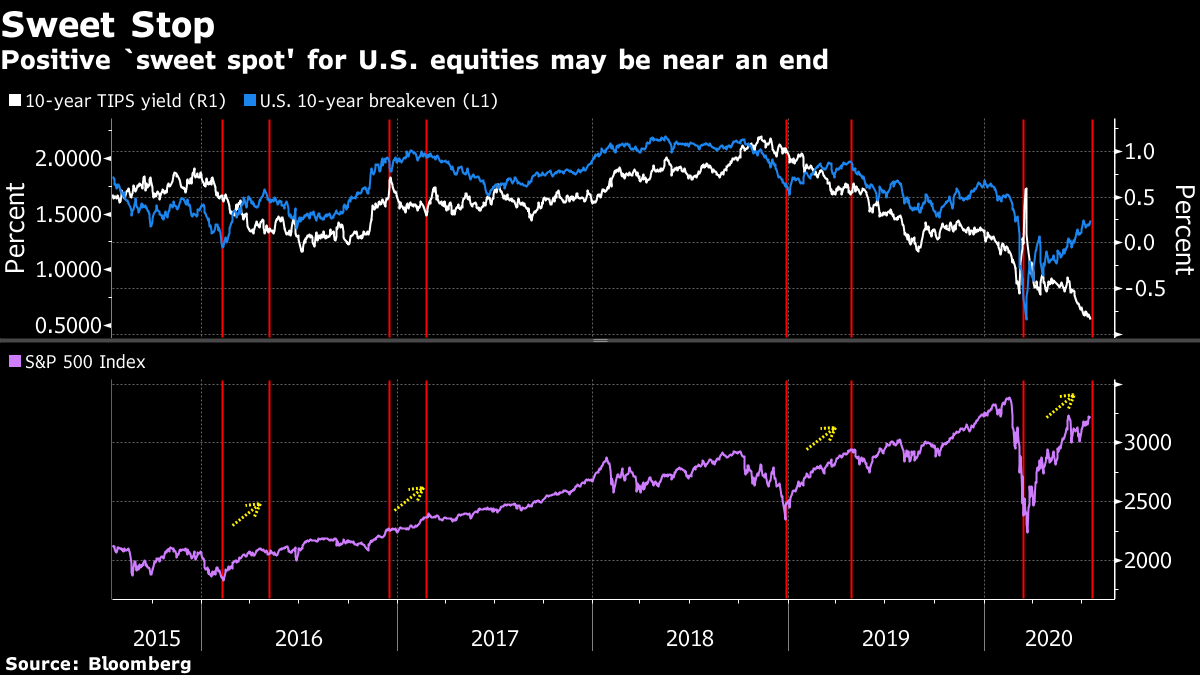

| Want the lowdown on what's moving European markets in your inbox every morning? Sign up here. Good morning. A landmark stimulus agreement, coronavirus vaccine hopes and lots of earnings. Here's what's moving markets. Deal Leaders of 27 European Union countries reached a unanimous agreement on 750 billion euros ($860 billion) in coronavirus recovery funds, divided into grants worth 390 billion euros and low-interest loans worth 360 billion euros. Reaching the deal took more than four days of acrimonious negotiations and represents a victory for German Chancellor Angela Merkel and French President Emmanuel Macron, who had drafted its first version. Almost a third of the funds are earmarked for fighting climate change. "I believe this agreement will be seen as a pivotal moment in Europe's journey," European Council President Charles Michel said. High Bar Virus statistics overnight hold some hope with California's hospitalization growth reducing and daily case growth in other hot spots like Florida and Arizona slowing too. Still, in New York, Governor Andrew Cuomo threatened to close bars and restaurants if large street gatherings continue and if social distancing and mask regulations aren't enforced. In Asia, Japanese Prime Minister Shinzo Abe told members of his ruling Liberal Democratic Party that there's no need to declare a state of emergency now. This all follows excitement in the treatment space Monday as a vaccine in development by the University of Oxford and AstraZeneca Plc showed promising results in early human testing. But despite initial optimism, the benefits didn't appear to match the bar set by other programs, analysts said. Nasdaq Jumps It was all about tech on Wall Street Monday as the Nasdaq 100 index had its best gain in three months to close at a record high. The stay-at-home trade drove a rise in the Fang bloc of megacap technology companies including Amazon.com Inc., while other pandemic beneficiaries such as Zoom Video Communications Inc. also gained. Later on, tech investors also digested numbers from International Business Machines Corp. that beat analysts' estimates on second-quarter revenue. Cloud sales are helping to offset coronavirus-fueled declines in the consulting services business, sending IBM shares higher in late trading. Here in Europe, stock futures are higher this morning. Not Done A day after the U.K. suspended extraditions and arms sales to Hong Kong due to human rights concerns around China's national security law, Prime Minister Boris Johnson is under pressure from his U.S. allies and British lawmakers to further toughen his stance on China. U.S. Secretary of State Mike Pompeo will meet members of Parliament who want to see sanctions on Chinese officials and get the Asian superpower cut from Britain's nuclear power program. The MPs will try to get him to carry their demands to his meeting with Johnson, according to people familiar with the matter. Coming Up… It's a busy morning of earnings. UBS Group AG reported second-quarter net new money that beat analyst expectations and said that share buybacks may resume in the fourth quarter. Novartis AG narrowed its full-year guidance toward the lower end of its previous range while booze maker Remy Cointreau SA boosted guidance and chocolatier Lindt & Spruengli AG beat sales estimates. Up next, we'll get an update from TalkTalk Telecom Group Plc, while Valeo SA is among companies expected to report after markets close. The U.K. is due to release its long-delayed report on Russian interference in the country's democracy. What We've Been Reading This is what's caught our eye over the past 24 hours. And finally, here's what Cormac Mullen is interested in this morning The likely end of a "sweet spot" combination of rising inflation expectations and falling real yields is going to make it a much tougher environment for U.S. equities. The drivers of the rebound -- unprecedented monetary and fiscal support, better-than-expected economic data and a rush of cash into high-flying technology shares -- had their powerful impact juiced by this mix. Ten-year breakevens, a gauge of inflation expectations, have more than doubled since hitting an 11-year low in March. And, yet, U.S. real rates have continued to slide -- the yield on 10-year Treasury Inflation-Protected Securities is trading at the lowest since December 2012 -- thanks to massive monetary stimulus from the Federal Reserve. U.S. stocks tend to rise when that happens as investors warm to better prospects for prices without an accompanying spike in rates. But inflation expectations remain modest overall, and at risk from a downgrade in growth expectations as positive economic data surprises peak. Furthermore, the pace of real rate declines is likely to slow as expectations for the Fed to introduce negative rates have cooled. There is no longer much doubt that officials will do what it takes if market stresses reappear, which could ironically lessen the likelihood they have to act. Given such a Fed "status quo" and a likely dialing-back of growth forecasts, the positive backdrop of sliding real rates and climbing inflation expectations could well be close to an end. And that will make it harder for equities to push ever higher.  Cormac Mullen is a cross-asset reporter and editor for Bloomberg News in Tokyo. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment