| Want to receive this post in your inbox every morning? Sign up here Less-terrible data expected, Trump escalates fight with China, and the U.S. continues to throw cash at the vaccine hunt. Numbers Weekly initial jobless claims will show a drop to a still-terrible 2.4 million, according to the median estimate of economists surveyed by Bloomberg when the number is published at 8:30 a.m. Eastern Time. While there is little upside in claims remaining in the millions for a ninth week in a row, there may be a ray of light in May PMI data at 9:45 a.m. It's forecast to show an improvement, while remaining far below the 50 level that would point to an expansion. Already today, PMI data in Europe was an improvement on April's numbers, showing that the region's worst phase on the economic front may be behind it. Blame game President Donald Trump upped his attacks on China as the coronavirus continues to take a heavy toll in the U.S. Unusually, he targeted President Xi Jinping, without naming him, saying the disinformation comes "from the top." The White House released a broad critique of Beijing's economic and military polices without detailing any specific response from. The deterioration of relations between the world's two largest economies ahead of the start of China's annual parliamentary session on Friday has observers worried the progress that led to the signing of the phase-one trade deal will be completely lost. Vaccine hunt AstraZeneca Plc received more than $1 billion in U.S. government funding or development of an experimental coronavirus vaccine, as the race to secure supplies accelerates. China's president has already said that any vaccine developed in the country would be made available as a global public good. Total confirmed cases of the virus passed 5 million, with deaths exceeding 328,000. More than 1.5 million of those cases are in the U.S. Markets drop Investors are taking a dim view of the worsening rhetoric between the U.S. and China, bringing a halt to the recent rally in equities. Overnight the MSCI Asia Pacific Index slipped 0.4% while Japan's Topix index closed 0.2% lower. In Europe the Stoxx 600 Index was down 0.7% by 5:50 a.m. with banks seeing the biggest falls. S&P 500 futures pointed to some red at the open, the 10-year Treasury yield was at 0.666% and oil rose for a sixth day. Coming up... As well as claims data, the April Philadelphia Fed business outlook is at 8:30 a.m. Existing home sales and the leading index for April are at 10:00 a.m. New York Fed President John Williams, Fed Vice Chair Richard Clarida and Fed Chairman Jerome Powell all speak later. Best Buy Co. Inc., Medtronic Plc and Nvidia Corp. are among the companies reporting results later. What we've been reading This is what's caught our eye over the last 24 hours And finally, here's what Joe's interested in this morning In Washington D.C., talks for a new round of stimulus are picking up. One point of focus is what happens with the expanded Unemployment Insurance provisions this time around under the CARES act, where some laid-off workers are able to temporarily get more take-home pay than they did while on the job. Critics say that this creates a disincentive to work, and that the enhanced UI will impede the economic recovery, as workers choose to stay home instead of taking job opportunities available to them.

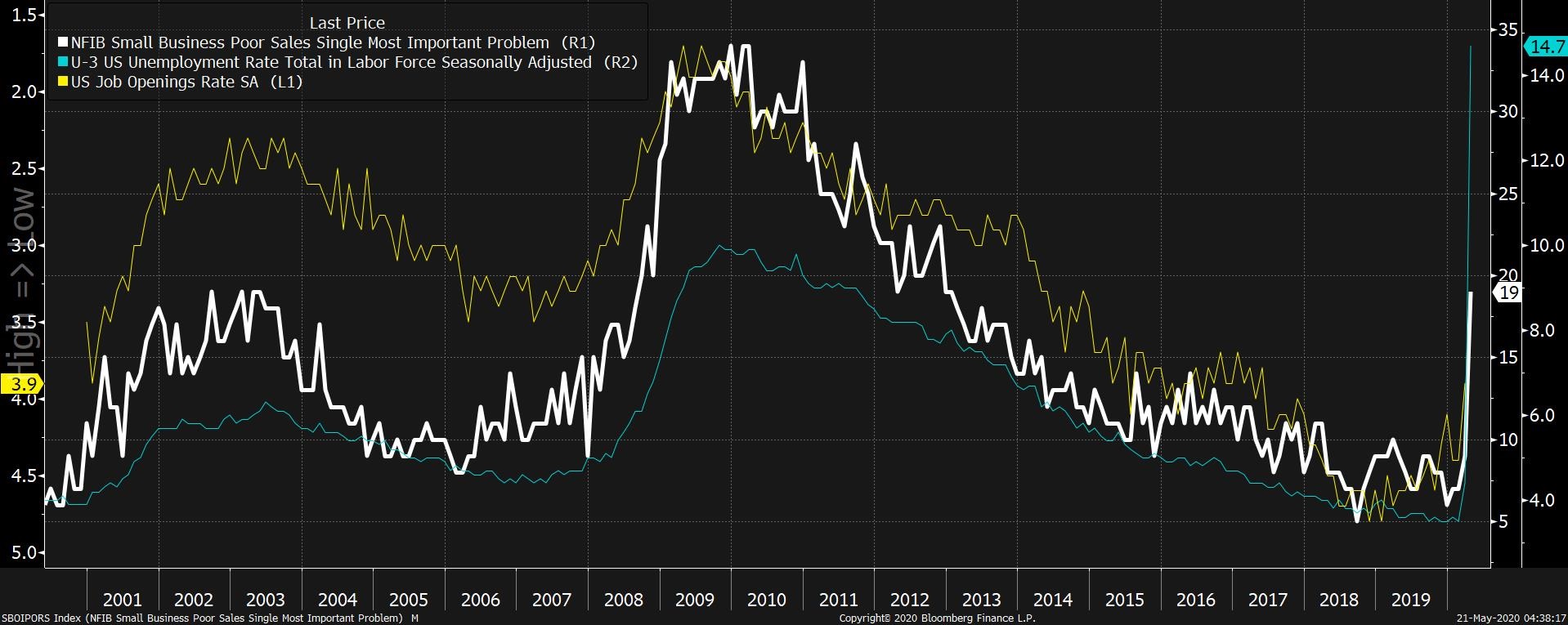

You can understand the intuition. Rationally, some people would choose to make more money and not risk getting sick, than going to work to make less money and risk getting sick. But while it might make sense on some micro-economic level (with some individuals and some companies), this logic falls apart on the macro level when thinking about the recovery overall. That's because the most important thing for a robust jobs recovery is for there to be lots of jobs available. And the most important thing in ensuring that there are lots of jobs available is robust household demand for goods and services from businesses. And the most important thing in ensuring that there's robust demand for goods and services is that household incomes remain strong. And one way the government is keeping up household incomes is via the expansion of the Unemployment Insurance program, which in normal times doesn't fully replace lost income. As Renaissance Macro Research recently put it, "allowing this program to lapse w/o some replacement would hurt demand and in turn, reduce the need to hire more in the first place." Ok, that all sounds nice and good, but is there actually any evidence of this? Check out the chart below. In the monthly NFIB Small Business Optimism Survey, one of the questions they ask companies is to identify their single biggest business problem right now. The bolded white line is the percentage of businesses citing "poor sales" as their biggest challenge. The white line corresponds nicely with the yellow line which is just the rate of job openings in America, as measured by the JOLTS survey. It makes sense. As revenue becomes less and less of a problem (as it did for most of the last decade), the rate of job openings increased right alongside it. Finally, the teal line is the unemployment rate, and again, it aligns nicely. As job openings increase, the unemployment rate came down. Again, it makes sense, but think back to 2009 and 2010 when there were a lot of fights about the Unemployment Insurance expansion. If there had been a situation where lots of people were turning down job offers, we'd expect to see a gap where job openings were rising, but the unemployment rate wasn't falling. Instead it's moved all in a line.  Bottom line: To get people back to work in droves, we need job openings. To create job openings, we need businesses to not be worried about revenue. And to ensure they're not worried about revenue, household income and demand needs to hold up. If the next round of fiscal stimulus does a poor job of replacing lost household income, you can forget about a return to a strong labor market. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment