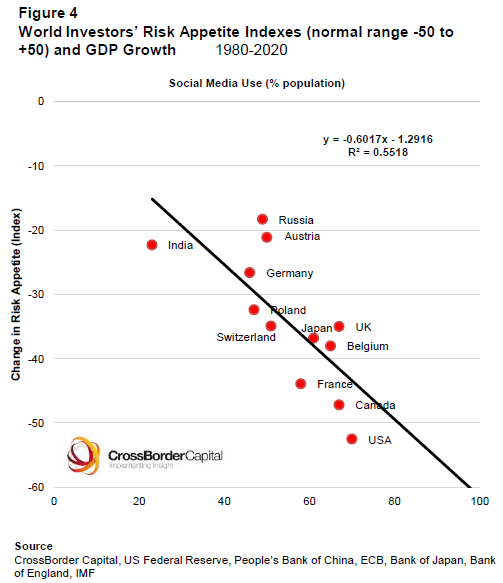

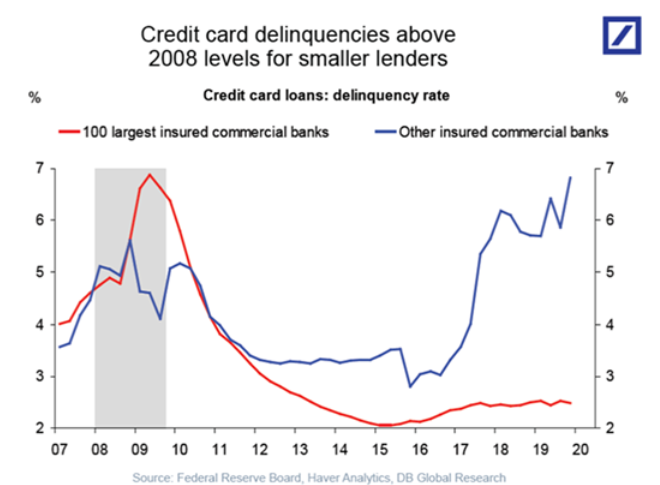

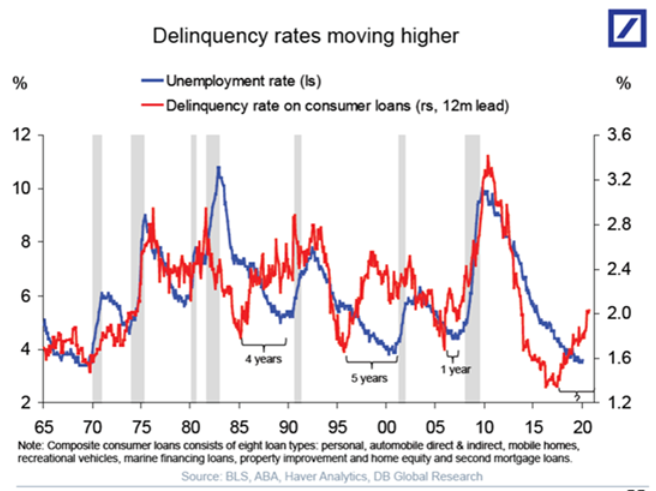

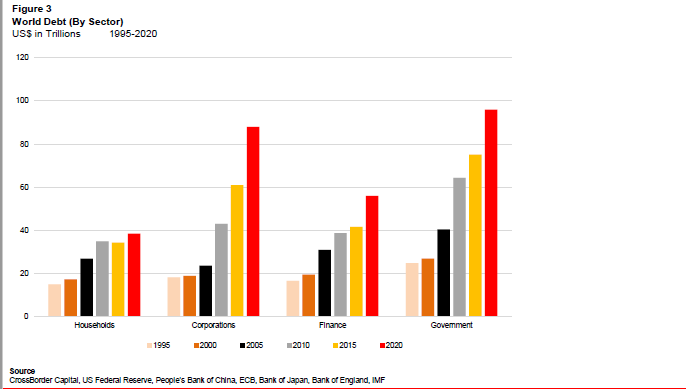

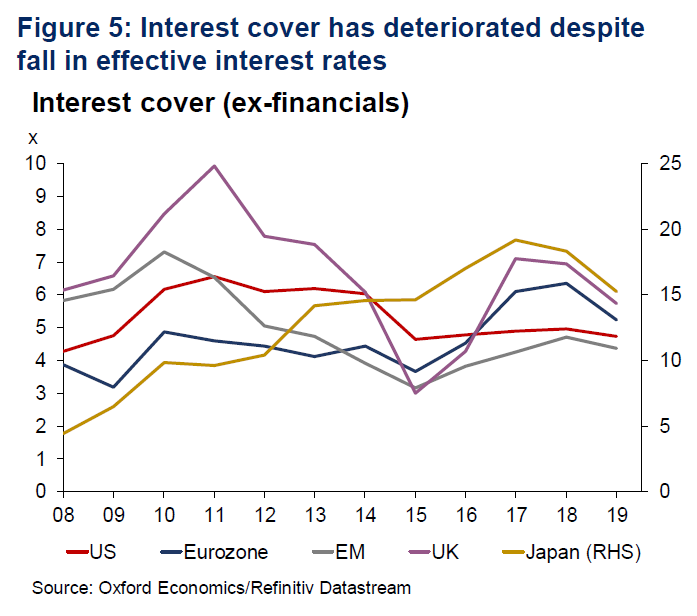

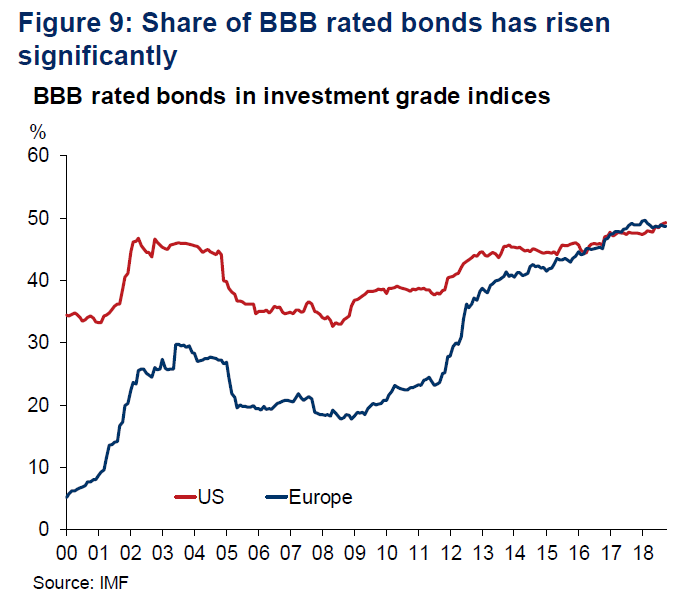

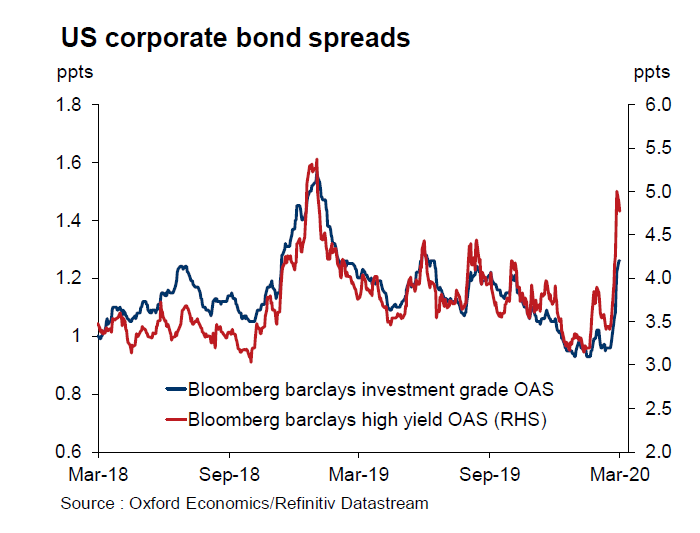

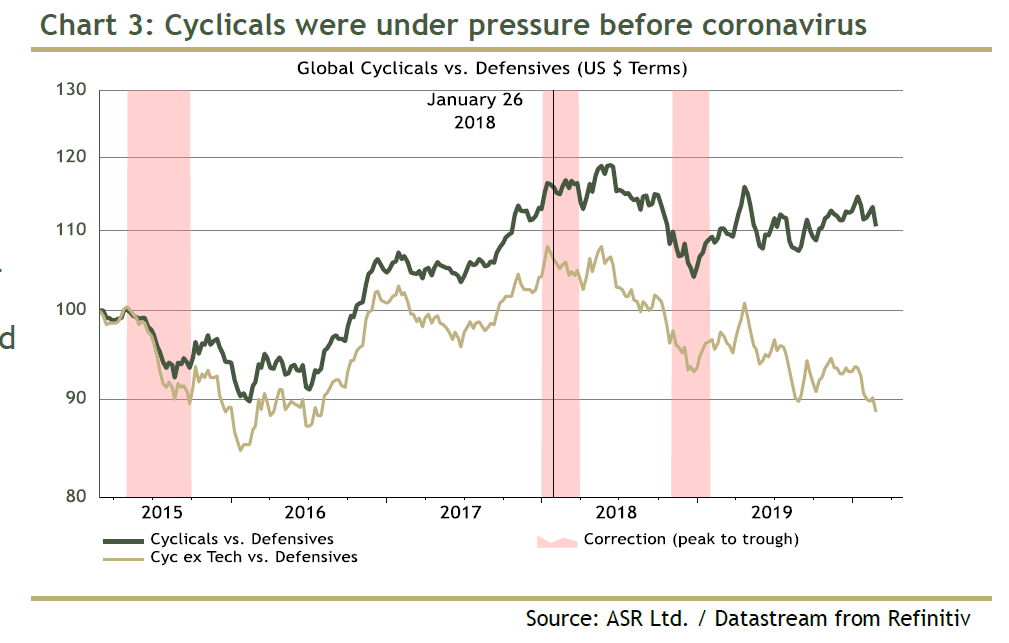

What Are You Afraid Of? What are you afraid of? It is a vital question that often helps with introspection and self-confidence. When it comes to markets, we can work out what is so frightening with hard quantitative evidence, and without having to delve into the subconscious. And the outcome is, I'm afraid, frightening. We are afraid of several things. In ascending order of severity and descending order of immediacy, I currently see at least three levels of fear: The Impact of Coronavirus on Our Lives This fear grows as it becomes more personally relevant. It involves no thought to the long-term economic consequences. Instead we worry about the immediate impact: panic-buying and hoarding, quarantine, and abandoned travel. In the U.S., this fear continues to rise, and has done so without a break for more than a month. The last few days, with news that there have now been 22 confirmed coronavirus cases in New York, where many traders live, has brought this fear to a new high. We can see this from the results of a trade which buys the S&P 500's food retailing sub-index, while selling short the hotels and cruise lines sector. This trade has returned 70% since the beginning of February, with the gain accelerating Thursday:  While the market as a whole has oscillated over the last month, this trade has not; investors have grown ever more certain that this epidemic will have a serious effect on their lives. The fact that they have this kind of fear in the short term makes them more prone to all the ills of crowd psychology. Personal proximity — and the coronavirus now has bridgeheads in many financial centers — will skew judgments. Proximity to social media is also a problem, which means that fear engendered by the epidemic is likely to have a greater impact. As the following fascinating chart from CrossBorder Capital Ltd. of London shows, the more a nation is saturated by social media, the more it will tend to become risk-averse. That means Americans, hosts to by far the world's biggest capital markets, have much less appetite for risk than they used to.  So that is the first level of fear — that we fail to shake the disease, it runs out of control, and we suffer a much diminished quality of life as a result. A Credit Crisis The particular fear that took hold Thursday is that the disease will cause a credit crisis, along the lines of the seizure of the global financial system in 2008 (if not necessarily that severe). If such a crisis were to occur, lasting economic damage could be done even if the disease subsequently came under control faster than expected. The risk of such a thing is perceived to have increased this week. The Federal Reserve's emergency rate cut, announced Tuesday, was presumably intended to combat such a risk, and yet financial conditions have since tightened further. The Bloomberg Financial Conditions index, which smooshes nine metrics from different asset classes, is set so that 0 marks the dividing line between accommodative and tight conditions — and it shows that the financial system has just endured a sudden and dramatic tightening:  This spells problems in particular for banks. They hit rock bottom exactly 11 years ago, on March 6, 2009, when the S&P 500 briefly hit the ominous number of 666. After that, they were able to show that they were operating profitably, which offered them the chance to repair their balance sheets. The best measure of confidence in banks is the multiple that investors will pay for their official book value — assets minus liabilities on the balance sheet. On 666 day, big lenders in both the U.S. and the euro zone traded at barely 40% of their book value, implying radical lack of confidence in the quality of their assets. U.S. banks staged a good recovery, but the last week has brought the KBW index of major U.S. lenders back to only a whisker above book value. As for the euro zone, its banks are perceived as chronically wounded, and now trade for barely half of book value.  Looking at the performance of equity, the euro zone's banks again give reason for deep concern. The euro zone's sovereign debt crisis eased after then-head of the European Central Bank Mario Draghi promised to do "whatever it takes" to save the euro, and this marked a trough for banking stocks. Amazingly, almost eight years later, bank shares are almost back to their level when Draghi made his promise. Again this speaks of deep fears of another full-blown credit crisis, and also puts great pressure on Draghi's successor Christine Lagarde to do whatever it takes (and not just say what she wants and hope for the best).  Tightening credit is threatening through a number of channels. In the U.S., there are signs of stress in consumer lending. Away from the biggest banks, there are also fears that consumer debt is precarious. As this chart from Deutsche Bank AG shows, credit card delinquencies are rising, and smaller banks appear to have a problem on the same scale that confronted the bigger banks at the height of the last crisis:  Deutsche Bank also shows that delinquencies on consumer loans are rising disquietingly in the U.S.:  But the greatest credit issue, across the world, concerns the corporate sector. Non-bank companies have drastically upped their leverage since the last crisis, as treasurers have taken advantage of historically low interest rates. This CrossBorder Capital chart shows the trend clearly:  Even with low interest rates, however, the prolonged drought of profitability is making it harder for companies to service debts. As Oxford Economics Ltd. shows, interest cover has been slowly declining:  Credit quality has also deteriorated in the eyes of the rating agencies, with now roughly half of investment grade debt in both Europe and the U.S. scored at the lowest available BBB level:  Meanwhile the spread of high-yield bonds compared to investment grade has also risen recently:  There is also reason to worry about international debt. According to the Bank for International Settlements, some $17 trillion is owed by non-U.S. corporations without what CrossBorder Capital describes as "obvious U.S. dollar access." It is hard to see how this will be refinanced without resort to further quantitative easing, just as some of the worst pain for individuals and small businesses to emerge from the virus may require helicopter money drops. None of this makes a credit crisis inevitable, and it should certainly be possible to avoid a crisis on the scale of 2008. The scale of the fear should increase the scale of the subsequent recovery if credit issues can be eased. But the fear that the coronavirus will be the trigger to spark the next generalized credit crunch is widespread, and is rational. Long-Term Global Recession The greatest fear that markets are dealing with is of a serious global recession, either caused or made worse by the coronavirus. Cyclical stocks were already under pressure before the current bout of instability began, as this chart from London's Absolute Strategy Research Ltd. shows:  The moves of the last few weeks only make sense if markets are bracing for a serious recession. (To be clear, it is always possible that markets have stopped making sense.) Any assertions about the bond market tend to be out of date as soon as they are written. The following chart shows 10-year Treasury yields dropping below 1%, and taking real yields (compared to inflation expectations) sharply negative. At the time of typing this, the bond-buying has renewed in the Asian session and the 10-year yield is approaching 0.8%. This is quite without precedent in the long history of the bond market. It makes sense to fear that there is a bond bubble which will subsequently burst — but the fear driving that bubble is of deflation and economic slump:  If bonds are now positioned for a global slump, note that commodities and emerging market stocks, the assets seen as most tied to global growth, have been consistently sending negative signals for the best part of a decade. They suggest fear of an unraveling globalization, which was intensified by the trade hostility between the U.S. and China, and has now been given a sharp extra push by the virus. Bloomberg's broad commodities index has set fresh post-crisis lows this week, while emerging markets continue to lag behind developed markets severely.  To answer the question, then. The market is afraid of spending time in quarantine eating canned food, while credit seizes up and banks collapse, followed by a long and enduring global deflationary slump. If we can manage to avoid all of that, and the odds are that we can, then there will be a lot of money to be made, although not by buying bonds. And we should all be happy to avoid such an alarming fate. But we need to have some confidence that we will do so; the nature of the virus threat is such that it will take a while to be sure.

To accentuate the positive, there is at least one positive sign as the weekend approaches. A month ago, The Economist masterfully signaled the peak of the virus in China by featuring it on the cover. Let's hope that its latest cover has performed the same trick again, this time for the disease's global spread. Arguably, this cover isn't quite frightening enough to signal peak global fear, but it's a step in the right direction:

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment