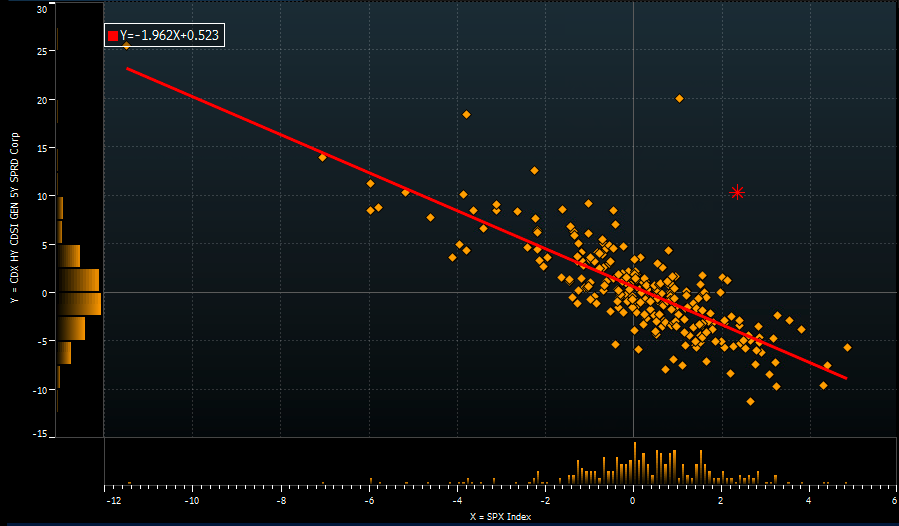

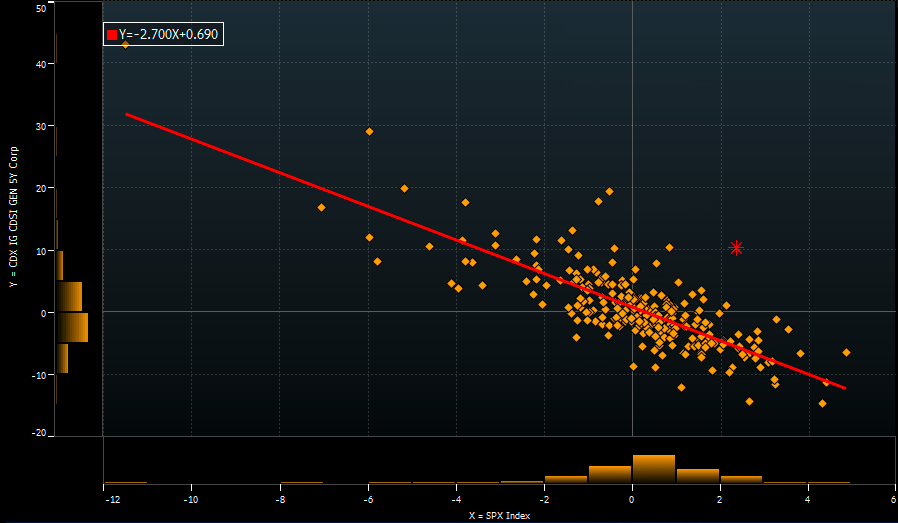

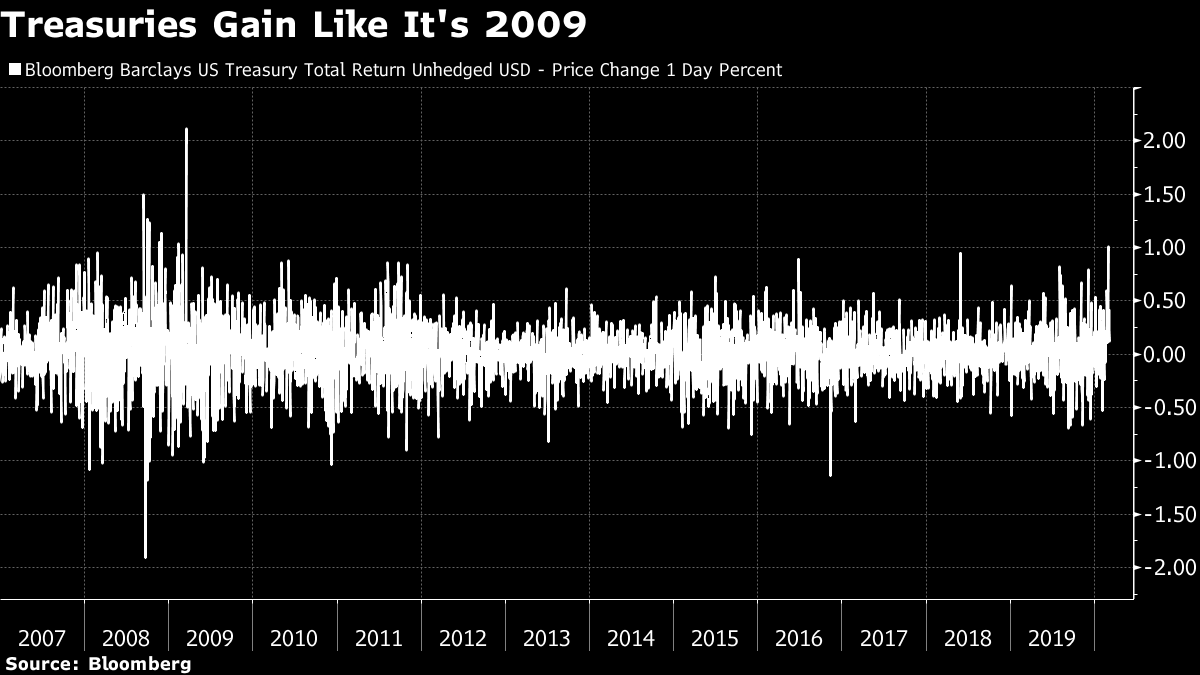

| Welcome to the Weekly Fix, the newsletter that isn't going to talk about the Fed's emergency rate cut because you know that already. –Luke Kawa, Cross-Asset Reporter CDX Gon' Give It To Ya "Stocks are still up on the week." As of Thursday's close, this is true for the S&P 500 Index. It's also one of the last refuges for the optimists out there. That's because the credit market has been sending a decidedly different message. Check out the divergence between high yield CDX and U.S. stocks this week (red dot):  Bloomberg Bloomberg High yield and investment grade CDX spreads are at their highest levels in over a year, and have widened materially this week. In the case of the junk, an optimist's explanation might be "well, that's down to energy – an increasingly small part of the S&P 500, so it shouldn't ring alarm bells." High-yield CDX had its biggest daily widening since 2015 on Thursday. But it's fairly rare for the S&P 500 to be up 0.8% or more in a week with investment-grade CDX at least five basis points wider. The last time that happened was in September 2018. In other words, the top of the 2018 markets before that year's fourth-quarter rout in risk assets.  Bloomberg Bloomberg We Are the <1% Well, that happened. Ten-year Treasury yields are trading with a 0-handle for the first time ever. The decline in Treasury yields leaves the 10-year more than four standard deviations below its six-month average, also a record.  On Wednesday, the Treasury market posted its best daily return since 2009.  Bruno Braizinha at Bank of America had this perspective, earlier this week: When we abstract from the near-term noise and volatility and refocus on year-end scenarios we find two limiting cases:

(1) a U.S. recession scenario with the pricing of the Fed to the Zero Lower Bound, which implies 20 basis points for two-year Treasuries and 50-80 basis points for 10-year Treasuries; or

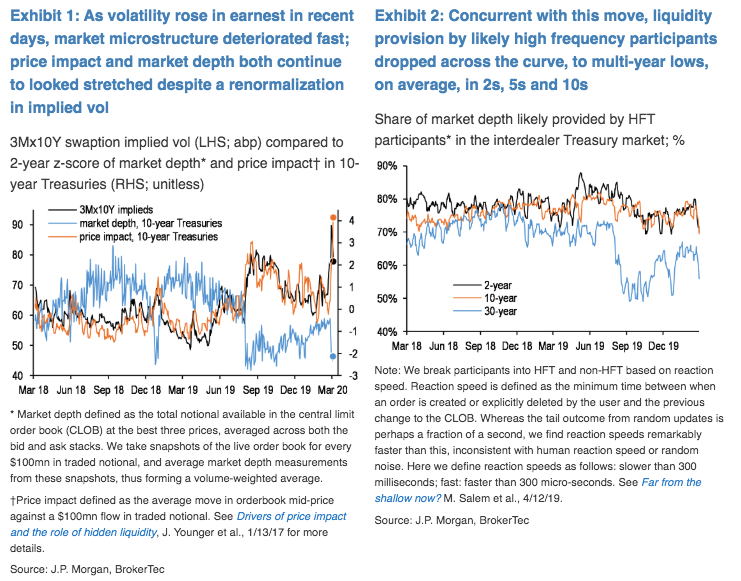

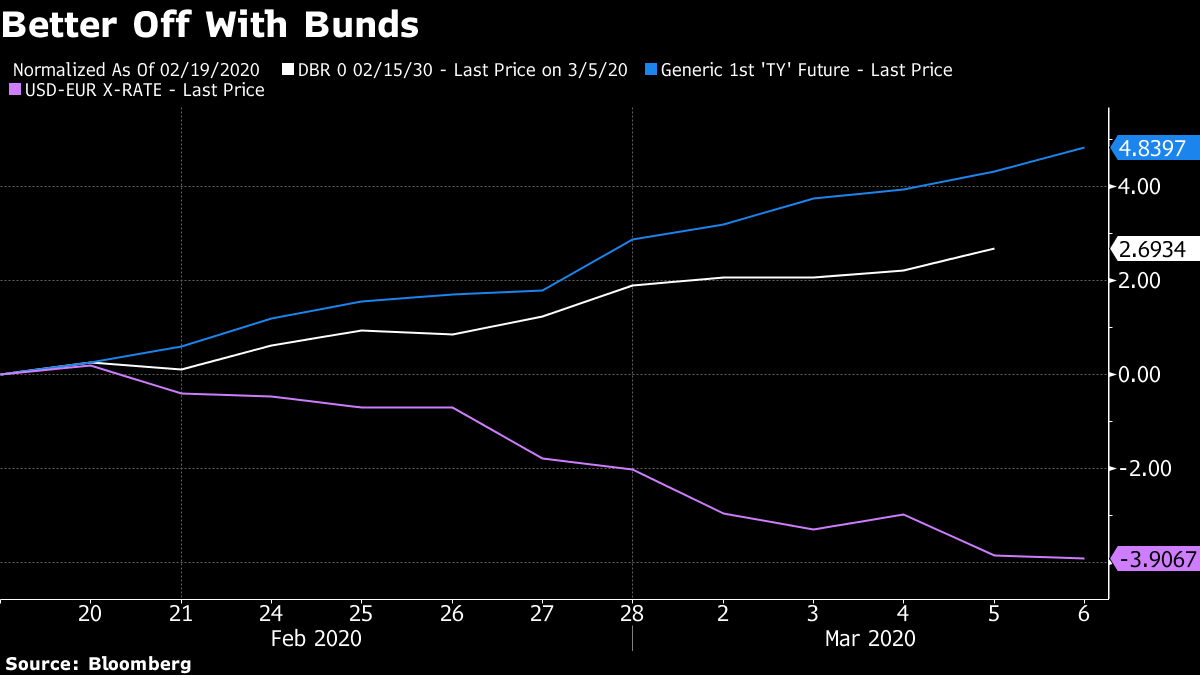

(2) an upswing back to trend growth as the coronavirus outbreak dissipates, which likely implies a Fed on hold after a 50 basis-point cut (two-year Treasuries around 1.1%) and 10-year Treasuries in the 1.5-1.7% range. A 50/50 weighting of these scenarios implies a 1-1.25% range for 10-year Treasuries at year-end. With forwards currently around 1.1%, the market seems to be assigning a marginally higher probability to the bullish rates scenario (bearish risky assets) for end-2020. Basically, Treasuries are trading like an option approaching expiration, and the directionality is clear. And JPMorgan Chase analysts discuss the magnitude of the move in U.S. Treasuries and how it has affected market liquidity: Late last week, market depth plunged across the curve, in some cases past the lows of August 2019, towards multi-year. Consistent with this, and against a sharp rise in trade volume, price impact – a measure of the magnitude of price moves per fixed unit volume – has surged to multi-year highs. Since then depth has remained suppressed and price impact has continued to surge, despite a partial renormalization in implied volatility.  JPMorgan JPMorgan Perspective is everything. One man's trash is another man's treasure, as the old adage goes. To adapt this to fit the current scenario, one foreign investor's Treasury rally is trash. The latest leg of an unprecedented surge in U.S. debt has actually been terrible for European investors that bought on an unhedged basis. Here's a look at the price returns in the 10-year Treasury future versus the German bund. U.S. dollar weakness (or euro strength) has eaten all of the outperformance.  Meantime, the record low 10-year Treasury yield strongly undermines the argument of those worrying about a dearth of demand of U.S. debt. But in an environment in which the euro can rise 90 basis points in a day against the dollar (which it has done three times in the past six sessions) and the 10-year Treasury yield is south of 90 basis points warrants reflection. It's uneconomical to buy Treasuries relative to German bunds on a hedged basis, and the dollar's retracement may foster creeping doubts about the wisdom of taking on currency risk when fleeing to safety is top of mind. The euro's strength during risk-off episodes, could prove ephemeral. But also, maybe not? As this newsletter has long discussed, it's a beloved funding currency, and the unwind of carry trades could foster a euro bid for longer than some might think. Another area worthy of further study is the potential for the U.S. dollar to be more risk-on than a risk-off currency, as market watcher Karthik Sankaran has suggested; it could be that U.S. exposures to foreign markets are much more likely to be hedged than foreign exposures to America. |

Post a Comment