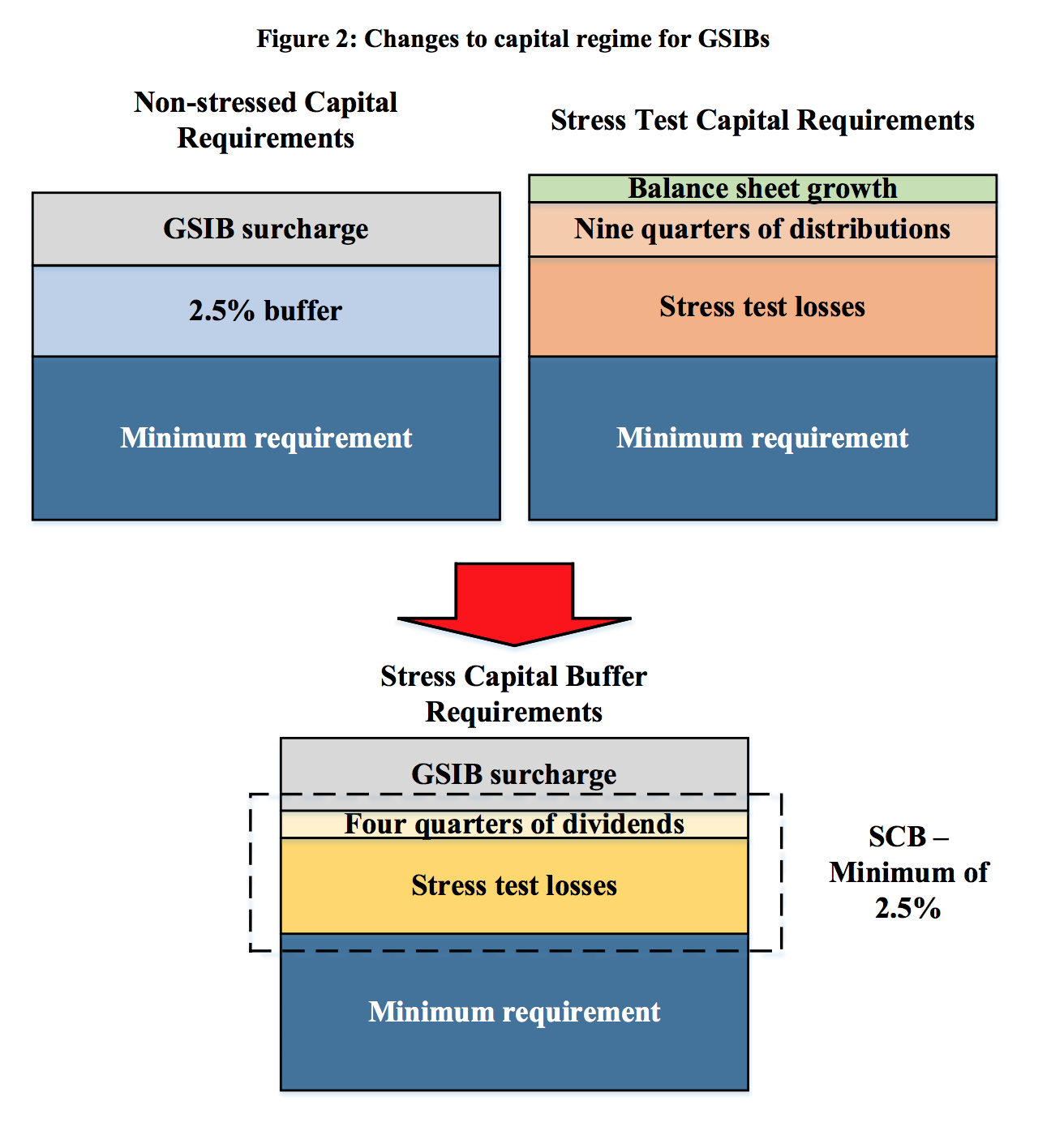

Capital The first rule of bank capital is that banks need to be solvent. Traditionally banks make a living by borrowing a lot of short-term money (deposits, etc.) and investing it in long-term assets (loans, etc.). If the bank owes depositors $100 and only has $95 worth of assets, that is bad, in a fairly straightforward way. You do not want that to happen. But the long-term assets can lose value: If you have a bank with $100 of assets and $99 of liabilities, and the assets lose 2% of their value, then the bank becomes insolvent. The way to prevent this is to require that banks have a certain amount of equity capital: You write a rule like "a bank with $100 of assets can only have $92 of liabilities," requiring the rest of the assets to be funded with equity. Then if the assets lose 8% of their value, the bank will still be solvent; it will still have enough enough assets ($92) to pay off its depositors. So the second rule of bank capital is that banks need to be well-capitalized: Being solvent ($1 more assets than liabilities) is not enough, you need to be solvent by a big enough margin that, if things go wrong, you'll still be solvent. But then you have a question of how to enforce this rule. You've got a bank, it has $100 of assets and $92 of liabilities. The assets lose some value—the market goes down, it made some bad loans, whatever. Now it has $98 of assets and $92 of liabilities. It is solvent, but it is undercapitalized. There is a rule saying that banks need to have at least 8% capital, and the bank is below 8%. It has broken the rule. Something must be done, but banks are fragile creatures. You could shut the bank down or fire its executives or fine it a lot of money, but all of those things will probably make the problem worse: Creditors will panic and withdraw money, forcing it to sell assets at a discount, possibly making it insolvent, which is the thing that the capital requirements were meant to prevent. You could force it to raise capital, but "please invest in this undercapitalized bank" is not a hugely attractive sales pitch. Just in general "undercapitalized bank" is not an attractive thing to say; it has the air of a self-fulfilling prophecy. If a bank goes out and announces "uh we only have 6% capital and we have to have 8%, we're aware of the problem and are working on it," there is a good chance that investors will flee the bank and the problem will get worse. That is, in theory, bank capital is a buffer to keep banks solvent in bad times. But in practice people worry that banks would not be able to use that buffer, that a bank that is down to its last percentage point of capital is already toast. This is the same problem as the first problem—"a thinly capitalized bank that loses money will become insolvent, which is bad" is identical in form to "a just-about-well-capitalized bank that loses money will become undercapitalized, which is bad"—and you solve it the same way. By requiring more capital. So the third rule of bank capital is that banks need to be, uh, extra-well-capitalized? That is not the technical term. Being well-capitalized (meeting the capital requirements) is not enough, you need to be so well-capitalized that, even if you lose some plausible amount of money, you will still be wellcapitalized. If you are particularly tidy-minded you could imagine this process repeating indefinitely ("well if an extra-well-capitalized bank loses money it will become only just-about-well-capitalized, which is bad"), but in practice it doesn't. Three rounds—solvency, capital adequacy and a buffer—are basically enough. In practice regulators take a sort of business-cycle approach: When times are good, you require banks to have (1) their capital requirements plus (2) enough extra capital so that they'll still meet their capital requirements when times are bad. When times are bad, you just require them to meet the basic capital requirements. The banks are adequately capitalized in bad times, and in good times they are so well-capitalized that they'll be adequately capitalized in the bad times. That's the theory. The actual measurement of all of these things is complicated and contested: How do you decide how much capital a bank needs to have to be well-capitalized? (In various different overlapping redundant ways.) Or how do you decide how much more capital a bank needs to have to be extra-well-capitalized? In the U.S., there are roughly two approaches to that one: - Plan out a series of scenarios that might cause the bank, or the banking system more broadly, to lose a lot of money. Project what effect those scenarios would have on the bank's income and asset values, and do the math to see what the bank's capital position would be in those scenarios. Require the bank to have at least enough capital, now, that if those scenarios occurred it would nonetheless still be well-capitalized.

- Just add 2.5% to the regular capital requirements, good enough.

The first approach is called "stress testing" and it is kind of the state of the art these days. The second approach is called the "capital conservation buffer" and, you know, it is also fine, it has its reasons. There are benefits, in complex capital planning, to sometimes using crude approaches. The key idea is to use both: Banks have to have enough capital to pass the stress test, and they also have to have at least the regular amount plus 2.5%. You want redundancies in the system. Yesterday the Federal Reserve Board "approved a rule to simplify its capital rules for large banks." Basically instead of two rules—stress tests and the capital conservation buffer—there will be one rule: "The 'stress capital buffer,' or SCB, integrates the Board's stress test results with its non-stress capital requirements." There's a picture:  In broad strokes it's still the same idea. You have to have your basic amount of capital, plus (1) whatever you'd lose in a stressed scenario but (2) at least 2.5%. There are some changes in the details. Instead of assuming you pay out dividends for nine quarters and then have a disaster, the stressed scenario assumes you pay out dividends for four quarters. "The Fed's stress tests would assume lenders restrain growth in their balance sheets during stressful periods, which doesn't happen under current rules." You add the GSIB surcharge—basically, a bigger capital requirement for bigger banks—to the stress losses. Everything in bank capital is controversial so this is controversial. Usually the controversy is that some people want higher capital requirements and other people want lower capital requirements. Here, pleasantly, part of the controversy is about whether this is a higher or lower capital requirement. Here is Randal Quarles, the Fed's vice chair for supervision, praising the rule: As a result, the SCB rule adopted today will lead to an increase in the Board's common equity capital requirements for large banking firms, as measured through the cycle, of approximately $11 billion, including an approximately $46 billion increase for the U.S. global systemically important banks. And here is Fed Governor Lael Brainard criticizing it: The SCB rule will reduce current required tier 1 capital by roughly $100 billion or 7 percent for large banks overall. The SCB rule will reduce current required common equity tier 1 (CET1) capital by $60 billion or 5 percent, and the rule could be expected to reduce current actual CET1 capital by $120 billion or 10 percent overall. You can get more details from the Fed's staff report, and there are different definitional disputes (what kind of capital? what kind of big banks?) that could lead you to disagree on the results, but the basic disagreement seems to be located in Quarles's use of the phrase "through the cycle." Under the new rules banks will need to have more capital than they were required to have, on average, from 2013 through 2019, but less capital than they were required to have in 2019. "How to Hedge a Coronavirus" The answer is "buy S&P puts," come on: Universa, managed by Mark Spitznagel, a protégé of "The Black Swan: The Impact of the Highly Improbable" author Nassim Nicholas Taleb, managed a little over $4 billion in assets as of the end of 2018. Claude Bovet, founder of Lionscrest Capital and a long time investor in the fund, estimates that Universa's tail risk hedging strategy, representing part of its capital, earned more than 1,000% in a matter of days. "It was a great month for us," says Mr. Spitznagel, who declined to disclose a dollar figure on those gains. He did point out, though, that the fund's positions are "convex to the market." In other words, its strategy of using options and similar instruments can register profits that escalate in much more than a linear fashion, suggesting a handsome payoff indeed. … Universa hedged without timing the market or taking a risk, which holds a lesson about risk, reward and complacency. While many reasonable investors were tempted to sell tech stocks or bet against them—2,000 people had died by the day they peaked—Universa ignored the headlines and focused only on what the numbers said. They told it that insurance was cheap. "If you have a position that can lose 1 to make 100, like Universa's tail hedge at any point in time, you don't care about your timing of a market crash, you just don't want to miss it," says Mr. Spitznagel. I will leave it to you to evaluate "always buy S&P puts" as a financial strategy, but I do want to say it's a great public-relations strategy. When the market crashes, you will get written up in articles with headlines like "How to Hedge a Rampaging Swarm of Killer Bees" or whatever is crashing the market, and you will sound almost eerily prescient. (How did you know about the bees?) When the market doesn't crash, no one will think to write about you at all. Convexity! You'll be wrong most of the time, but people will only hear about you when you're right. Elsewhere: "Short Sellers Made Over $50 Billion During Coronavirus Sell-Off." One way to hedge the coronavirus, in hindsight, was to short Tesla Inc. stock, which was "the most profitable short since Feb. 24" by dollar value. I do not think that anyone shorted Tesla to hedge against the coronavirus; nor do I think that the coronavirus outbreak provides much validation of a Tesla short thesis. But sometimes things work out. Expectations Jefferies Financial Group Inc. has a target return on equity of 9%. If it achieved a 9% "return on tangible deployable equity" in 2019, its executives would get a nice bonus. If it missed that target, but managed at least a 6% return, they'd get half their target bonus. If it achieved a 12% return, they'd get an even bigger bonus. It managed a 5.89% return on equity, oops, no bonus. Just kidding no they got the bonus anyway: WeWork's dramatic fall should have deprived top executives at Jefferies Financial Group Inc. their bonuses. That was until the bank's board stepped in and authorized $10.7 million in cash payouts to Chief Executive Officer Richard Handler and three of his deputies, according to a regulatory filing Tuesday. Jefferies wrote down the value of its stake in WeWork by $182.3 million last year after the co-working company's attempted initial public offering backfired spectacularly. The charge cut an earnings ratio used by the board to determine bonus payouts for senior bosses, effectively denying them their payouts. But the board, which for years has said there should be a strong link between executive compensation and performance, said the "massive collapse" of WeWork's valuation was "completely unanticipated and dramatic." You might think that investing a lot of shareholder money in a catastrophic money bonfire would be the sort of core error that might cost financial-services executives their bonus, but the board points out that they did a lot of things right too: Defending the payouts, the board listed other accomplishments, including hiring a new class of investment bankers that's 49% female and the fact that the firm didn't face a major lawsuit or significant regulatory scrutiny in 2019. Ignoring those achievements "would neither provide the right incentives nor recognize what was a successful year," the board said in the filing. Here's the filing. Honestly it's fine? No sensible human could resist making fun of this a little, but I basically sympathize with the board here. Jefferies had "a banner year with respect to executing on our plan to transition our business to a highly focused pure financial services platform," and "continued to take market share from our competitors," and sure yes not being sued a lot is pretty good, for a financial services firm in the U.S. in 2019. The board thinks the executives did a good job on almost every aspect of their performance, with WeWork being an anomalous debacle. If you are partly in the business of investing, even if you work hard and are smart and have a good process, sometimes you will have a dud; if you are only partly in the business of investing, perhaps that dud should not define your year. Still it is funny for a financial firm to be like "well our executives were pretty bad at investing this year but they didn't get sued much and that's good enough for us." Reasonable! Possibly correct! But funny. Fund names The Securities and Exchange Commission has a rule about investment fund names, which is helpfully called the Names Rule. It is considering revising that rule, and has asked the public for comments, so if you have any comments about how investment funds should be named, now is your chance. For instance it is an empirical fact that hedge fund names typically include "nautical terms, alcoholic drinks, and cities in New England," but now is your chance to have that tendency enshrined in law. "No hedge fund shall have any name other than the name of a city, town, neighborhood, island, hill or street in New England," the SEC could perfectly well say. Or "Hedge fund names shall be taken from Greek, Roman, Norse, Egyptian, Babylonian or Hindu mythology, but in no case shall any hedge fund be named after anything in Tolkien, and Star Wars names shall be felonies." Let's make this happen. Oh fine no actually the rule is about mutual fund names, and it's pretty boring. From the request for comments: The Names Rule generally requires that if a fund's name suggests a particular type of investment (e.g., ABC Stock Fund, the XYZ Bond Fund, or the QRS U.S. Government Fund), industry (e.g., the ABC Utilities Fund or the XYZ Health Care Fund), or geographic focus (e.g., the ABC Japan Fund or XYZ Latin America Fund), the fund must invest at least 80 percent of its assets in the type of investment, industry, country, or geographic region suggested by its name. It would be funny if funds named for New England cities had to invest 80% of their assets in companies from those cities. Here is a weird problem with the Names Rule: The number of index-based funds is growing. While funds are subject to the Names Rule, indices are not investment companies and not subject to the Names Rule. The staff has observed that index constituents may not always be closely tied to the type of investment suggested by the index's name. This raises questions under the Names Rule when the fund name includes the name of the index. If you are a mutual fund manager and you run the XYZ Latin America Fund, you have to invest 80% of your assets in Latin America. If you are an index provider and you set up the QRS Latin America Index, you can do whatever you want: You are not an investment adviser, you are not a fiduciary, you are not investing anyone's money, you are just writing down a list of companies. If your list is only 50% Latin American, that's your business. But if you are a mutual fund manager and you run the XYZ QRS Latin America Index Fund (indexed to the QRS Latin America Index), you have a strange semantic problem: Do the words "Latin America" in your fund name refer to the geographic region (in which case you have to invest 80% of your assets in the region), or are they part of the phrase "QRS Latin America Index" and refer only to the index (which is only 50% Latin American)? It is hard to imagine that this is a huge problem, exactly, but it is on the SEC's mind. David vs. Goliath We talked last year about a federal financial fraud case against Live Well Financial Inc., a reverse mortgage originator that allegedly used third-party pricing services to inflate the valuations of mortgage bonds it owned, and then used those inflated valuations to borrow a lot of money that it couldn't pay back. As bond mismarking cases go it was fairly colorful; Live Well CEO Michael Hild allegedly called the mismarking scheme a "self-generating money machine." He seems to have colorful friends too; here is a story about Ben Dusing, a friend of Hild's from high school who is now a lawyer and "has built a reputation on winning acquittals for high-profile clients accused of white-collar crimes in federal courts in Cincinnati and Northern Kentucky." Now he's going to the big city to defend Hild: United States Attorney Geoffrey Berman's office is prosecuting the case in the Southern District of New York in the prestigious Manhattan courthouse. "It is the Yankee Stadium of financial fraud worldwide," Dusing said. … "I don't care what the facts are; it is David versus Goliath," Dusing said, adding, "There are advantages to being an outsider." The whole story has a pleasing sort of reverse-"My Cousin Vinny" vibe: Dusing is known for wearing pocket squares and fancy suits while testing the limits of judges' patience with long arguments and frequent questions about the properness of evidence, witnesses, jury instructions and prosecutors. But he is also known for delivering results. … "This little guy from Kentucky started this (company) and it had a lot of benefit to a lot of people," Dusing said. "A lot of people who would appropriately be described as the elite in this country benefited from the existence of Live Well Financial. And after they benefited and the dust clears, the little guy from Ft. Wright, Kentucky, is under indictment in the elite capital of the globe … for financial fraud." I suppose eventually he will say more about the alleged bond mismarking. Things happen Credit Suisse chairman has sought to extend tenure. Wells Fargo Was Promised Soft Handling by Trump Appointee, Democrats Say. HP Rejects Xerox's Hostile Takeover Offer, Calling Bid Too Low. "Homeowners are starting to lock in some of the lowest 30-year mortgage rates ever." Farmers Fight John Deere Over Who Gets to Fix an $800,000 Tractor. Star Engineer Who Crossed Google Is Ordered to Pay $179 Million to Company. "The arrival of ridehailing is associated with an increase of approximately 3% in the number of fatalities and fatal accidents, for both vehicle occupants and pedestrians." The Anxiety Algorithm. "People were stealing our Häagen-Dazs. It was a big problem." Forget Chess—the Real Challenge Is Teaching AI to Play D&D. If you'd like to get Money Stuff in handy email form, right in your inbox, please subscribe at this link. Or you can subscribe to Money Stuff and other great Bloomberg newsletters here. Thanks! |

Post a Comment