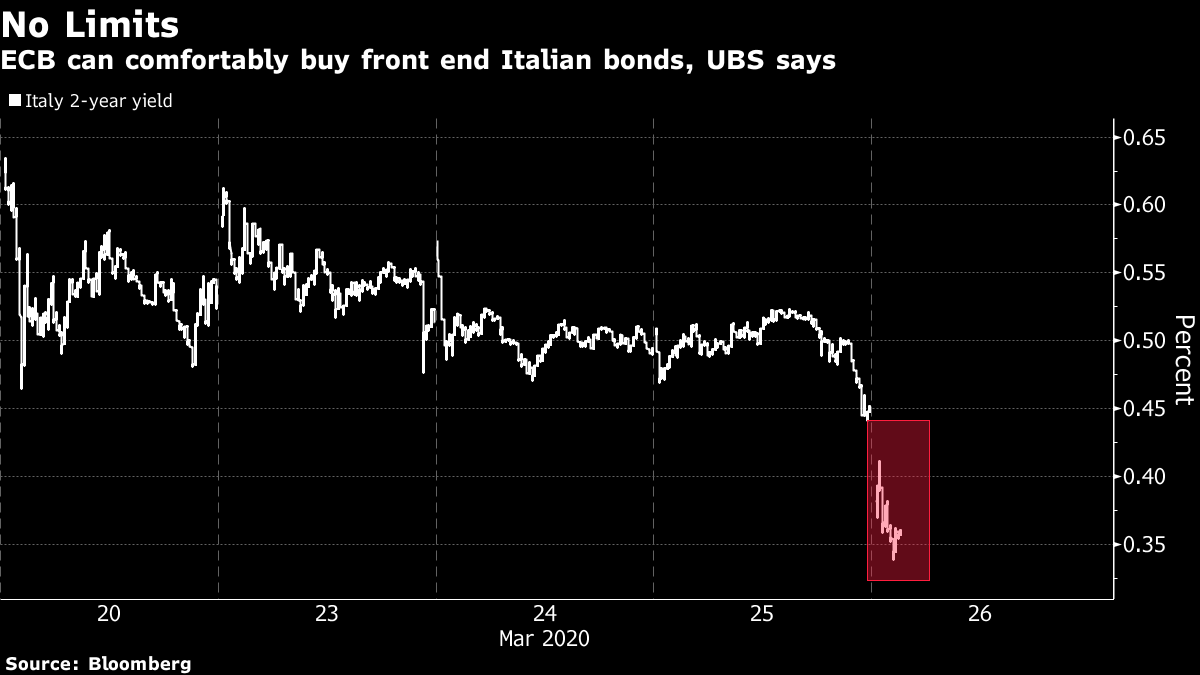

| All eyes on jobless claims, Senate passes $2 trillion virus plan, and WHO says countries are wasting time. Record number This week's initial jobless claims data at 8:30 a.m. Eastern Time is the most hotly anticipated in years as it will be the first hard data on the severity of the economic hit from the coronavirus-spurred shutdowns. The median estimate of economists is for 1.6 million with forecasts running as high as 4 million. White House chief economic adviser Larry Kudlow said the number would show a "very large increase." Canada saw jobless claims of nearly 1 million, representing nearly 5% of the total workforce. Bill passed The Senate passed the historic $2 trillion stimulus bill last night in a 96-0 vote following intense negotiations between Republicans and Democrats on the make-up of the package. The measures include loans to corporations, tax breaks and direct payments to companies and individuals. Democrats won a major concession in securing independent oversight of the $500 billion slated for distressed companies, but there are fears the move could slow the flow of cash. The House is scheduled to vote on the bill tomorrow, and President Donald Trump said he would sign it immediately. Virus warning There was an unusually blunt message from the World Health Organisation for governments, with the body saying political leaders should stop wasting time in the fight against the spread of the coronavirus. WHO Director-General Tedros Adhanom Ghebreyesus said the first window of opportunity to act has already been squandered. The death toll from the virus in the U.S. passed 1,000 as states continue to tighten movement restrictions, and Governors call for more funding to help fight the outbreak. Evidence of the global economic fallout piles up by the day, with Singapore estimating its economy shrunk the most in a decade. ECB goes all in The European Central Bank published the legal text of its 750 billion euro ($819 billion) Pandemic Emergency Purchase Program (PEPP) which revealed the bank will scrap the issuer limits on purchases of bonds, and widened the scope of buying to include instrument with as little as 70 days left to maturity. "The decision removes virtually all constraints on asset purchases," Frederik Ducrozet, global strategist at Bank Pictet & Cie. in Geneva, said. Euro-area sovereign bonds are rallying as markets digest the details of the move, with short-dated Italian debt dropping as much as 13 basis points and Greek bonds surging this morning. Speaking of central banks, the Bank of England announces its latest policy decision at 8:00 a.m. this morning. Markets drop Now that the stimulus bill has been passed, global equity investors seem to be turning back to worrying about the virus, with markets taking a turn lower today. Overnight, the MSCI Asia Pacific Index gained 0.1% with a mixed performance across the region. Japan's Topix index dropped 1.8% while India's Sensex Index jumped over 4%. In Europe, the Stoxx 600 Index was 1.5% lower at 5:55 a.m. with all but one industry group trading in the red. S&P 500 futures pointed to a drop at the open, the 10-year Treasury yield was at 0.811% and gold slipped. What we've been reading This is what's caught our eye over the last 24 hours. And finally, here's what Lorcan's interested in this morning Yesterday the European Central Bank published the details of its emergency asset-purchase program designed to ease the economic fallout from the virus shutdowns across the euro area. Looking at the details, it's hard to overstate how significant the measures introduced are -- forget about OMT, this package gives the ECB almost unlimited powers to buy whatever fixed income it wants, from whoever it wants. It is a clear sign of how serious policy makers are taking the threats from the virus that the ECB Governing Council was able to agree on such a package. (It's traditionally seen as the home of some of the most conservative monetary hawks on the planet, especially relative to the U.S.) But -- of course there's a but -- the response to the outbreak in the region should be much more reliant on fiscal than monetary measures. In an column in the Financial Times this morning, former ECB President Mario Draghi warned that "the cost of hesitation may be irreversible" as he called for a huge increase in borrowing to meet the needs of the economy. While national governments are introducing their own measures, the lack of a euro-wide package is starting to seem like a major oversight. Leaders of Spain, Italy, France, Portugal, Greece, Belgium, Luxembourg Slovenia and Ireland wrote a letter calling for the introduction of "coronabonds" ahead of today's top-level summit. While the list of countries calling for what would basically be euro bonds is long, it is missing the names of some key players, particularly Germany. This crisis is very different to the sovereign debt crisis, but the major step that could have been taken then, and should be taken now to solve a lot of the pain is the same: the issuance of joint liability debt. Unfortunately it seems likely that like last time, national concerns will trump a move to acting as "one Europe" rather than acting as a collection of nations using a common currency. I hope I am proven wrong, but the appetite for such a move, even under the current exceptional circumstances, seems low where it matters most. As long as focus remains on helping individual nations, and not the euro area as a whole, this moment too will pass without the introduction of common euro bonds.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment