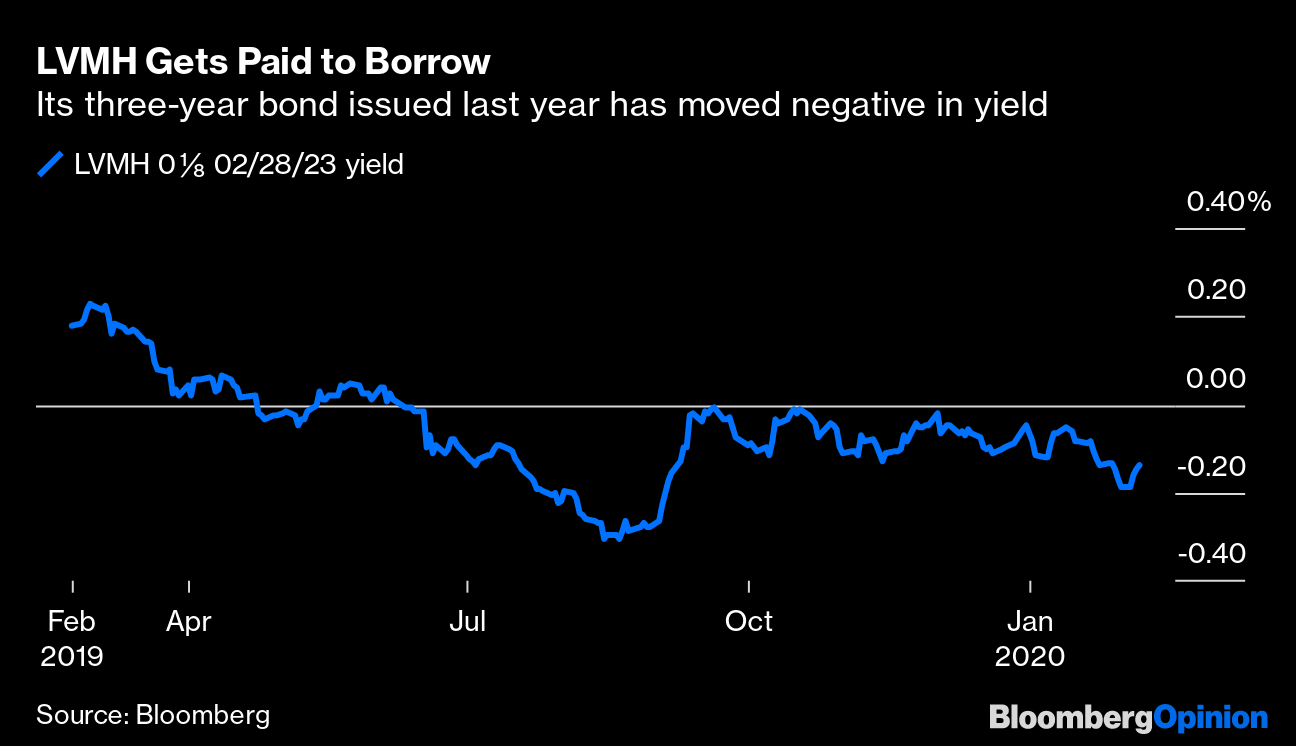

| This is Bloomberg Opinion Today, a data release of Bloomberg Opinion's opinions. Sign up here. Today's Agenda  The monthly jobs report. Photographer: Orlando/Hulton Archive/Getty Images The Jobs Report Is a Rorschach Test Monthly jobs reports are kind of like early Iowa caucus returns. Everybody watches them obsessively. They're unreliable. Some politicians use them to declare premature victory. Others claim they're rigged. (Hi, Herman Cain.) It could be a year before we know who won the latest Iowa caucus. It will definitely be a year before we know for sure how many jobs the U.S. economy created in January. There was a report today, sure, showing 225,000 jobs created. But that will be revised repeatedly, and next year the government will overhaul all of 2020's numbers. It took an axe to the 2019 data today, reporting the economy created 422,000 fewer jobs than we first thought, notes Justin Fox. Some of the biggest hits were in the fracking, retail and restaurant industries. Coal mining, which President Donald Trump has promised to make great again, lost jobs too, Justin notes, but the true insult was that the government cut it from some future data reports because it has withered to such a tiny nub. Trump will get credit for the overall health of the job market, which may be the strongest argument for his re-election. Democrats won't really help their case by poor-mouthing the economy if nobody believes them, writes Ramesh Ponnuru. Of course, because this is Trump we're talking about, he claims way more credit than he deserves. The economy's trends were in place before he got to the White House, and job growth was better in the last year of Barack Obama's presidency than in any year of Trump's. This will probably be the last jobs report for which reporters get an early peek, giving them time to write full stories and offer immediate analysis. From here on, the fastest robot to read the numbers will win the day, notes Brian Chappatta. The change may not be fair, but it also may not cause much market turmoil. It almost certainly won't keep us from obsessing over the numbers. Credit Suisse Drama Loses a Key Player The Credit Suisse reality show took a spectacular turn today, with the Swiss bank ousting CEO Tidjane Thiam. He had started the drama back in January 2019, fighting with his then-head of wealth management, Iqbal Khan, after Khan "insulted the state of the garden" at Thiam's house. Real House-Husbands of Swiss Banking stuff. The two kept feuding until Khan left for UBS, at which point Credit Suisse started spying on him to make sure he didn't poach bankers. Thiam was cleared in the ensuing scandal, but the bank claims the controversy hurt its reputation. But getting rid of Thiam barely begins to solve its problems, writes Elisa Martinuzzi. The new CEO faces operational problems and angry shareholders who wanted Thiam to stay. This firing is another example of a company placing "stakeholder" interests over shareholders, writes Matt Levine. In this case, the stakeholders were the Swiss establishment. Always Look on the Bright Side of the Coronavirus The economy edged closer to another Fed boost today; the central bank called the Wuhan coronavirus a new risk to global growth. And new risks often result magically in lower interest rates. The stock market, after days of aggressively not caring about the virus, cared today, supposedly. The epidemic is definitely bad for China's growth, with knock-on effects around the world. There are some upsides, if we may be so crass. For example, this was about the best possible time for this disruption to happen to Apple Inc., writes Tim Culpan. Its global supply chain is already pretty diversified from China. The virus also means Beijing has slowed a shadow-banking crackdown that was hurting the economy, writes Shuli Ren. This is a good chance to rethink the approach. But the negative effects are everywhere: Copper prices are down, writes Clara Ferreira Marques (though stimulus will goose them back up again). America's frackers are hurting from the impact on oil prices, notes Liam Denning (though they needed balance-sheet control anyway). And the luxury sector is discovering it's overexposed to China, writes Andrea Felsted. Hard Times for Unicorn Survivors The end of the Unicorn Era is forcing some hard choices. For one thing, unicorn herder Softbank Corp. must learn a way of life that doesn't involve showering startups with comical amounts of cash, notes Tim Culpan. Fortunately, Elliott Management has come along to give it some pointers. Meanwhile, mattress-maker and former unicorn Casper Sleep Inc. must cope with an IPO that didn't raise as much money as it had hoped. The failings of other unicorns didn't help Casper, but Joe Nocera notes the company is also weirdly burning through much more cash than its peers. Telltale Charts Once upon a time Saudi Arabia crushed the Soviet Union by flooding the market with oil, just when it needed higher prices to feed itself. The tables have turned on this rivalry, writes David Fickling — though now may not be the best time for Russia to get revenge.  Thanks to the ECB buying up corporate debt, LVMH is getting paid to borrow money to buy Tiffany & Co., writes Marcus Ashworth.  Further Reading Tonight's Democratic debate could be the biggest yet, but Pete Buttigieg's rivals may not gang up on him. — Jonathan Bernstein Value stocks have underperformed for a long time, but they might not be permanently broken. — John Authers Vladimir Putin laughed for years as Turkey annoyed the U.S. Now it's doing the same thing to Russia. — Bobby Ghosh Companies have good reason to crack down on food theft more than office-supply pilfering. — Sarah Green Carmichael ICYMI We're not ready for the next global virus outbreak. Masks won't save you from coronavirus, though there's a shortage anyway (h/t Mike Smedley). This is what it takes to be in the 1% around the world. Kickers Chernobyl fungus eats radiation. Something is happening to Norway. Scientists grow date-palm trees from 2,000-year-old seeds. Spice up your next party with the best board games of the ancient world. Note: Please send board games and complaints to Mark Gongloff at mgongloff1@bloomberg.net. Sign up here and follow us on Twitter and Facebook. |

Post a Comment