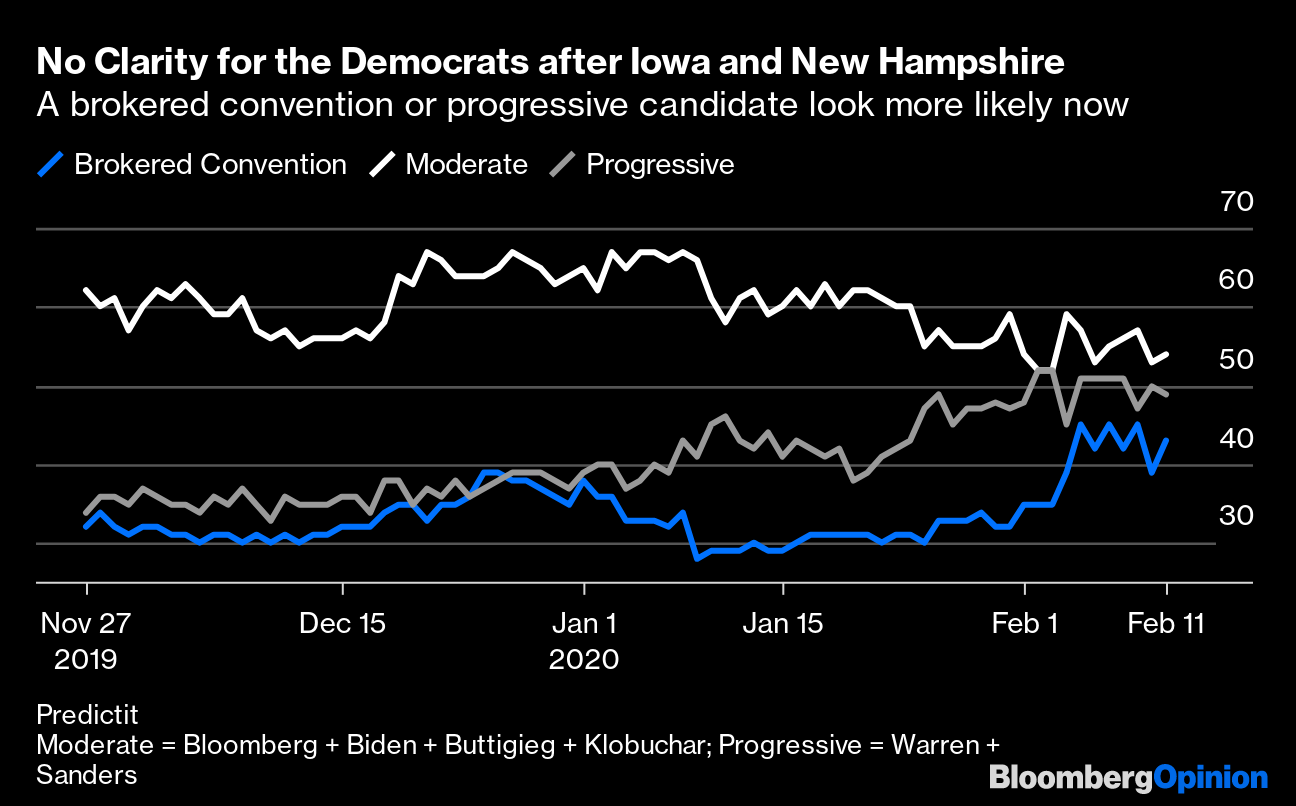

Greeks Bearing Gifts Does politics matter, or doesn't it? Some remarkable moves are afoot, the world over, and they aren't getting the market response that might be expected. Italy The Italian bond market made a new landmark Wednesday. The spread of Italian BTP yields over equivalent Germand bund yields is now back down where it was in the spring of 2018, before the left wing-populist Five Star movement and the right-populist League announced that they had agreed on a coalition. That government briefly threatened a confrontation with the European Union over the Italian budget, causing country risk to soar. Now, Italy's economy looks very weak; it has a new coalition with the League now out of power though still influential. But as far as the market is concerned, the worst of the political risk is over:  Greece Greek bonds set an even more historic landmark. It was Greece that triggered the eurozone's sovereign debt crisis after its election in 2009, when newly elected Prime Minister George Papandreou announced that he had discovered the deficit was higher than previously disclosed, and in breach of the eurozone's official rules. For years afterwards, the spread of Greek over German bond yields dominated thoughts and discussions of politicians and investors throughout the eurozone. On Wednesday that spread at last returned to its level when Papandreou was elected in October 2009. As far as the market is concerned then, judging by the metric that for a long time was treated as the definitive one for the eurozone's chance of survival, the crisis is finally, definitively over:  How did it get there? A decade ago, I and many other commentators assumed that the eurozone could only right the ship with massive institutional reform. New institutions would need to ensure that the eurozone had one fiscal policy, as well as one monetary policy. And the eurozone's stricken banking system would need to be shaken up and reformed. Instead, politicians opted to muddle through, and just about got away with it. In Greece, political instability has been extreme. The premiership, which passed from Kostas Karamanlis to Papandreou in 2009, has moved through Lucas Papademos, Panagiotis Pikrammenos, Antonis Samaras, Alexis Tsipras and now Kyriakos Mitsotakis. On the other side of the Greek-German spread, all of them had to deal with the same German chancellor, Angela Merkel. But despite suffering a full-blown economic depression, root-and-branch structural reform is still absent in Greece. Like the eurozone, it is still muddling through. The new prime minister represents New Democracy, the party that bequeathed the mess to Papandreou in the first place. And the same elites remain in place. Three of Greece's prime ministers from 2009 onward are the sons of previous prime ministers, including the current incumbent. There is little or no reason to see why the crisis that was unleashed in 2009 could not be repeated. Nothing has been done to reform the system. But the market is comfortable that the risk is over. Europe None of this much helped the eurozone. The euro is no longer believed to be under existential threat, and the periphery no longer trades at an extreme spread over the center, but the euro nevertheless weakened Wednesday to a 32-month low against the dollar. The problem now has moved from periphery to center. German and French politics both see embattled governments dealing with populist insurgencies, against a background of serious weakness in their industrial sector. Politicians may have muddled through the crisis, losing the U.K. along the way. The existence of the euro itself may no longer be in question, but confidence in the eurozone, its economy and its political institutions remains very low:  U.S. Yet another record close for the S&P 500 on Wednesday suggested that markets saw nothing to worry about in the recent events in Iowa and New Hampshire as the Democrats attempt to settle on a competitor for President Donald Trump. The human drama is compelling — the apparent free-fall of the campaigns of former Vice President Joe Biden and Massachusetts senator Elizabeth Warren is a sight to behold. Three months ago, I reported that the word "Warren" was everywhere. Now, Bernie Sanders is planning a revolution, and nobody seems to care. Prediction markets are imperfect but crystallize conventional wisdom as well as anything. This chart summarizes where Predictit sees the race; it is roughly a 50-50 shot whether a progressive (now almost certainly Sanders) or a moderate (who could be almost anyone, including Michael Bloomberg, the founder and majority owner of Bloomberg News's parent company) gets the nod. There is a very significant chance that we have a brokered convention for the first time since 1952. And indeed it is already hard to see how anyone other than Sanders can wrap up a majority of the delegates before the convention, such is the confusion on the moderate side of the party. It is an awful mess.  A few months ago, markets were terrified by the prospect of President Warren. Now they are calm. Why? The rationalization goes as follows: Sanders is unelectable, and so if he is nominated, then the market-friendly Donald Trump should win; any of the moderates would do relatively little damage to the markets (and Bloomberg might even do them some good); and the confusion of a contested convention would merely served to improve still further the chances of a Trump re-election. Each chain in this logic makes sense, but it still smacks of dangerous complacency. Unelectable candidates do get elected (see 2016). The Predictit market puts a Republican victory at only a 56% probability, which represents a sharp improvement over the last two months, but is still nothing like a shoo-in. If a new Trump scandal erupts when Sanders is his only possible replacement, or if there is a contested election result, that would not be great for an already blatantly overvalued stock market. Greek and Italian politicians have muddled through for now; it would still be wise to take out some insurance against the risk that American politicians cannot manage the same trick. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment