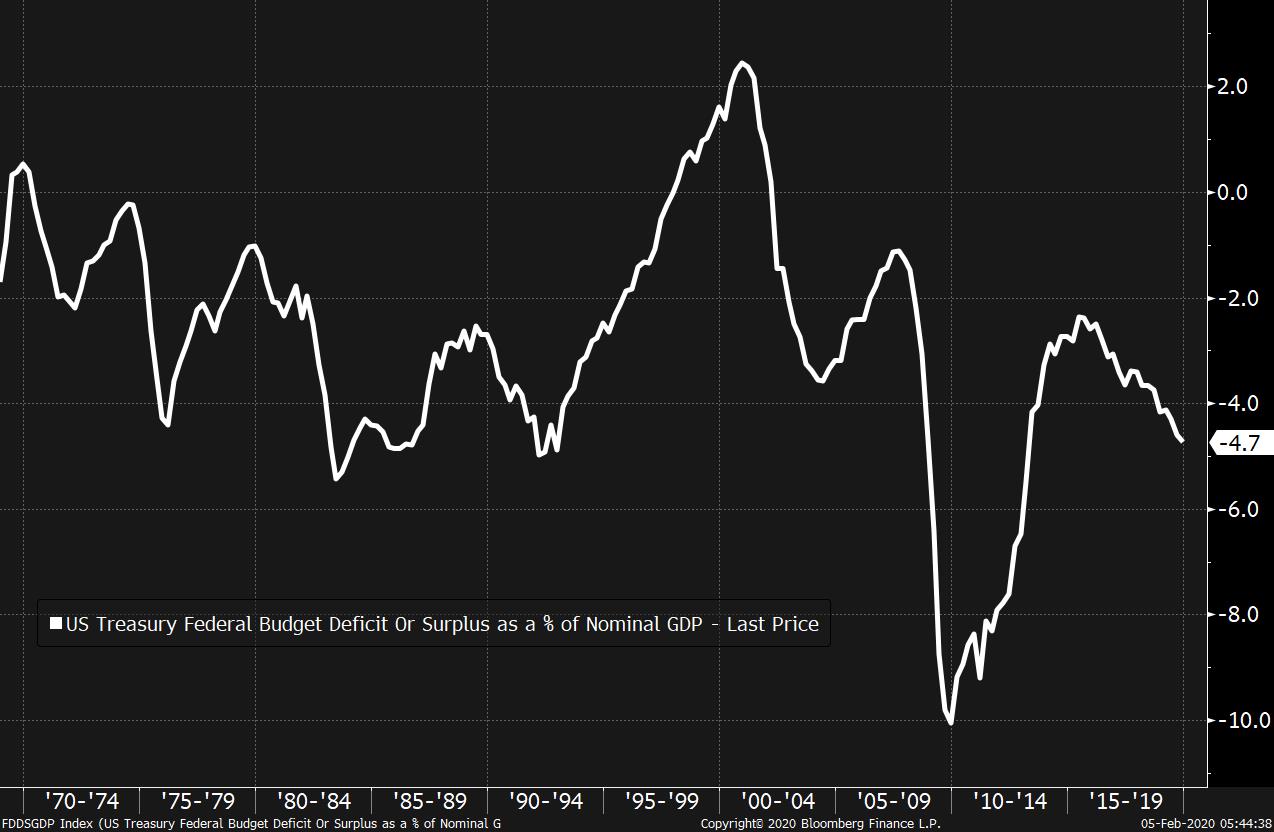

Virus fallout continues, partisan divide overshadows Trump address, and OPEC+ talks continue. Almost 25,000The number of confirmed cases and fatalities from the coronavirus outbreak continues to rise, with governments announcing further measures to combat the spread. Hong Kong's leader said the city will quarantine people arriving from mainland China, saying that "the next 14 days are critical." Experts in the U.S. now see little hope the advance can be largely contained within China, and advise that governments should plan for the worst. The economic damage is mounting, with hundreds of global supply chains cut due to the extended holiday in China. Trump stumpPresident Donald Trump's annual State of the Union speech made no mention of the impeachment saga which is expected to wrap up with his acquittal in the Senate today. He spent much of the address describing economic gains in the U.S. under his leadership ahead of his re-election campaign. The animosity between Republicans and Democrats was on full display, with Trump refusing to shake House Speaker Nancy Pelosi's hand before the speech, while she ripped up a copy of the text of the address when he finished speaking. Regardless of the partisan spectacle, it has already been a good week for the president, with news of his highest approval rating since taking office, according to a Gallup survey. Still talkingOfficials from OPEC and its allies gathered for a second day of talks in Vienna for further technical discussions about whether to increase production cuts to counter falling global crude demand due to the virus. Estimates on the long-term impact on demand remain highly uncertain, and Russian resistance to further reductions means that a meaningful agreement may be difficult to reach. In the market this morning, a barrel of West Texas Intermediate for March delivery was trading at $50.72 by 5:45 a.m. Eastern Time. Markets riseGlobal equities remain focused on events in China, with reports of advances in producing a vaccine boosting sentiment. Overnight the MSCI Asia Pacific Index climbed 0.7% while Japan's Topix index closed 1% higher. In Europe the Stoxx 600 Index had gained 1.1% by 5:45 a.m., with the regional gauge helped by stronger than expected final PMI readings for January. S&P 500 futures pointed to another strong start to trading, the 10-year Treasury yield was at 1.637% and gold was lower. Coming up…The excitement about Friday's payrolls number gets going at 8:15 a.m. when ADP publishes its employment change number. The U.S. trade balance for December is at 8:30 a.m. Final January services and composite PMI from Markit is at 9:45 a.m., with ISM non-manufacturing at 10:00 a.m. Brazil's central bank may cut rates at today's meeting. General Motors Co., Qualcomm Inc. and Peloton Interactive Inc. are among the companies reporting earnings. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Joe's interested in this morningOn Monday, I wrote about how seemingly everyone these days says we need a "handoff" from monetary to fiscal policy. With central bank rates at extremely low levels, and widespread frustration at the pace of the post-crisis recovery, it's a commonly held view that next time we have a downturn, government spending needs to play a central role in stabilizing the economy. But in a new piece for Project Syndicate, the economist Kenneth Rogoff says this is all a fantasy. Basically -- and it's hard to argue with this point -- there's a lot of naivety in this discussion about the politics of government spending. In some dream world perhaps politicians look at what the economy needs, and do what's best in a timely manner. In the real world, however, politicians have motivations like re-election and making their opponents look bad. And that makes a timely spending boost an unrealistic and unreliable tool. So Rogoff's prescription is to just forget about fiscal policy altogether, and instead focus on new tools that central banks can use, like negative rates. Whether you agree with Rogoff or not here, his piece gets at an important aspect of the whole debate, which is that the argument you have to have precedes economics. The question is, do you accept the constraints of the existing system and say "well, politics will make fiscal stimulus unreliable, so let's just stick with our reliance on central banks." Or, do you say "more active fiscal policy is better, so let's find a way change the political constraints." You could argue that this tension explains the rise of MMT, which is really a fusion of an economic framework with political activism. While the MMT economists write books and papers making the case for more aggressive use of public money, non-economists are spreading messages and memes in order to affect the political change that might allow theory to be put into practice.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment