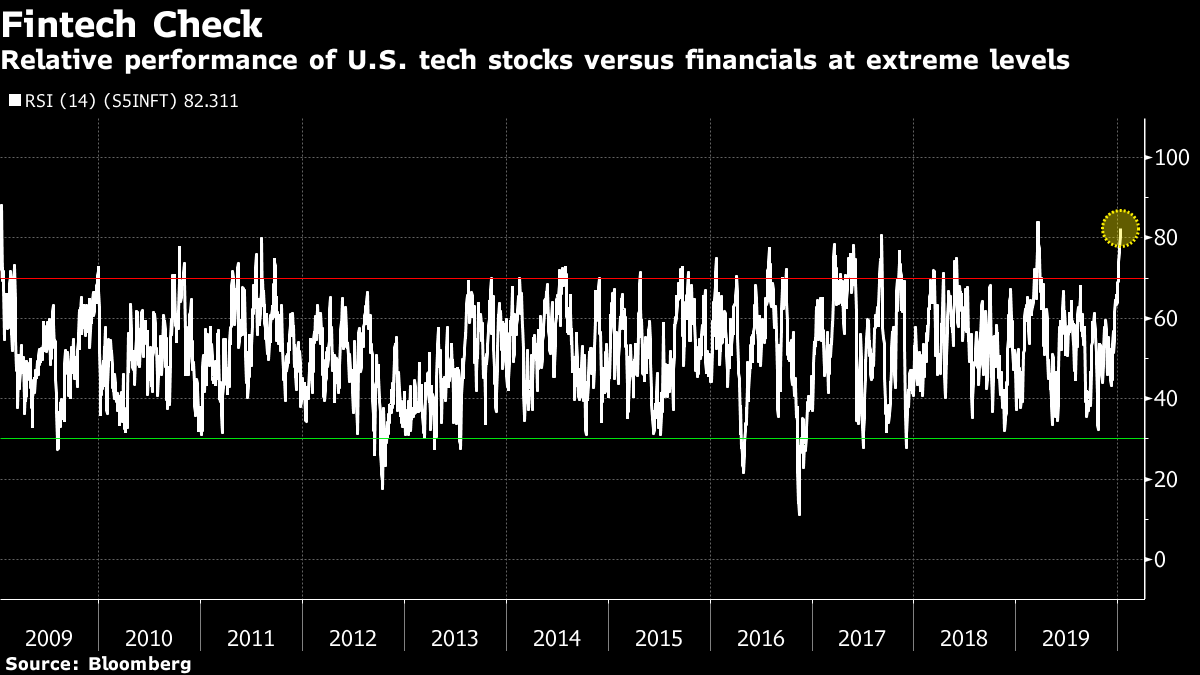

| Welcome to your morning markets update, delivered every weekday before the European open. Good morning. The U.S. dropped its label of China as a currency manipulator, the pound steadied after slumping on Monday and big U.S. banks start reporting earnings. Here's what's moving markets. Label Dropped The Trump administration lifted its designation of China as a currency manipulator in an important change to the U.S. stance that should give investors further confidence in relations between Washington and Beijing. "China has made enforceable commitments to refrain from competitive devaluation, while promoting transparency and accountability," Treasury Secretary Steven Mnuchin said in a statement, ahead of the scheduled signing of the phase one trade deal on Wednesday. Pound Steadies The pound steadied against the dollar overnight, after sliding Monday following Bank of England policymaker Gertjan Vlieghe's comments on the potential for more stimulus, in addition to gross domestic product numbers that showed the economy contracted in November. Money markets priced in a 50% chance of a rate cut this month, up from 25% on Friday, based on the remarks, with gilt yields sliding. But here's why the central bank might be setting itself up for a policy mistake if it does cut too soon. Stocks Trim Gains Asian stocks trimmed earlier gains as data showed Chinese trade with the U.S. dropped almost 11% in 2019, crimped by the trade war. Equities had risen earlier on the change in the U.S. stance on China, while technology shares sent the S&P 500 and Nasdaq Composite benchmarks to record highs in New York. While European stocks mainly slipped on Monday, there's a potentially bullish indicator coming from fixed income as German bond yields creep back toward positive territory, in a possible sign that investors are more buoyant about the state of the region's economy. Big Banks Earnings reports start flowing today from big U.S. banks, with Citigroup Inc. and JPMorgan Chase & Co. due out. Analysts expect the sector to see a combined profit drop of $10 billion this year, as global interest rates remain low and geopolitical tensions high. That said, quarterly trading revenue could be a bright spot amid a weak comparative given the market turmoil that took a toll on the industry at the back end of 2018, if you can remember that far back. European peers don't start reporting until the end of the month. Coming Up… In European earnings, we'll get numbers from FTSE 100 home-builder Taylor Wimpey Plc and Swiss chocolatier Lindt & Spruengli AG, among others, while better-than-expected results from German chipmaker Dialog Semiconductor Plc could boost tech today. Elsewhere, it's worth noting that the European Union's new trade chief will be in Washington for talks for the next three days, with both sides having recently revived old disputes and triggered new ones as a result of fundamental disagreements over trade policy. What We've Been Reading This is what's caught our eye over the past 24 hours. And finally, here's what Cormac Mullen is interested in this morning Another day, another fresh record for U.S. stocks Monday, with once again technology stocks leading the charge. While the S&P 500 is up a short 2% so far this year, the NYSE FANG+ Index of tech behemoths has risen closer to 9%. This kind of a surge hasn't always been a positive for future returns. In fact tech's dominance over other sectors has reached such extreme levels that it could presage equity weakness, at least in the short term. For example, the 14-day relative strength index -- a gauge of price momentum -- of the tech sector versus its financial counterpart has risen above 80 for the first time since March. Previous climbs above 80 have led to a median decline in the S&P 500 Index of 2.5% over the following two months, according to Sundial Capital Research's Troy Bombardia. Sentiment is bullish and optimism over this week's signing of the U.S.-China trade deal seems to be the catalyst. However given the stellar gains in 2019 and already strong start to 2020, investors would be wise to remember the old market adage that sometimes it's better to travel than to arrive.  Cormac Mullen is a Cross-Asset reporter and editor for Bloomberg News in Tokyo. CORRECTION: Monday's newsletter incorrectly referred to Iran as an "Arab nation." We apologize for the error. Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. Before it's here, it's on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can't find anywhere else. Learn more. |

Post a Comment