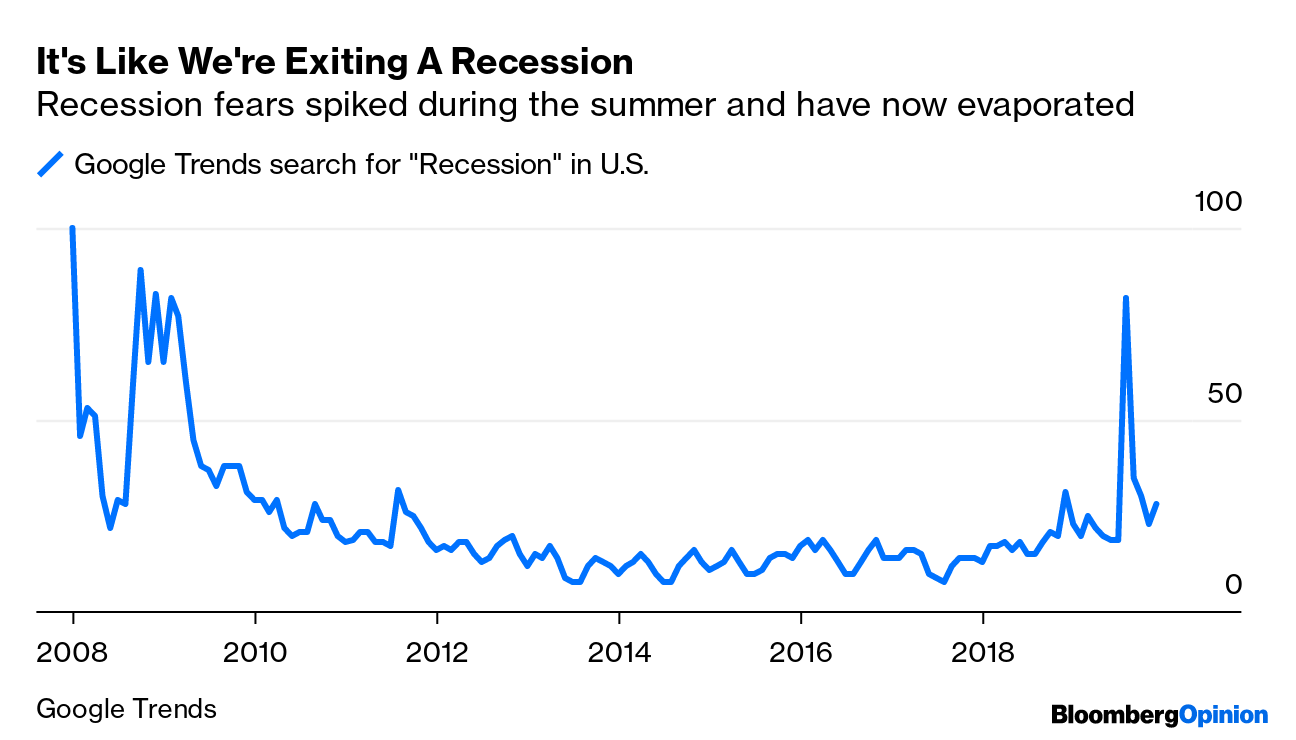

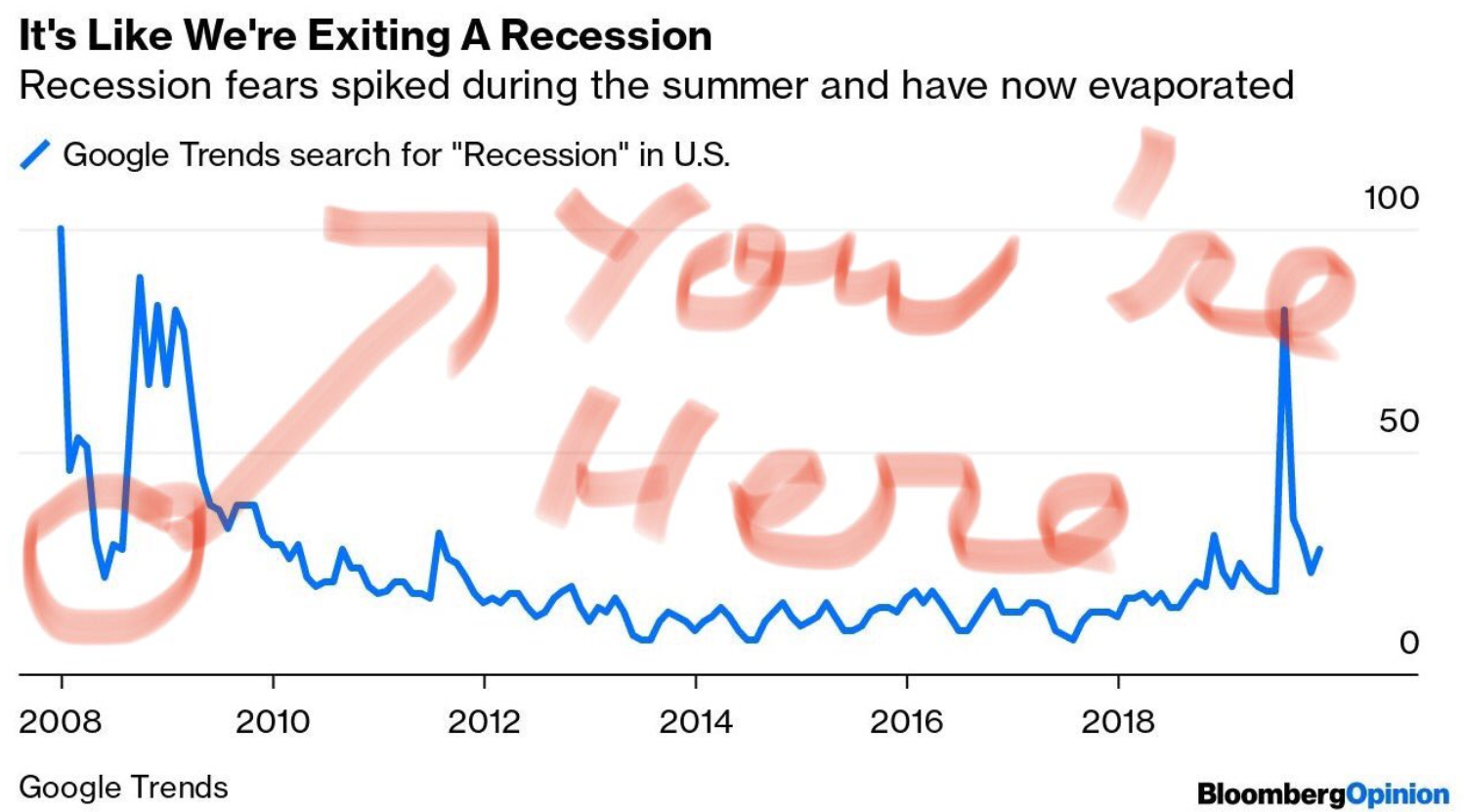

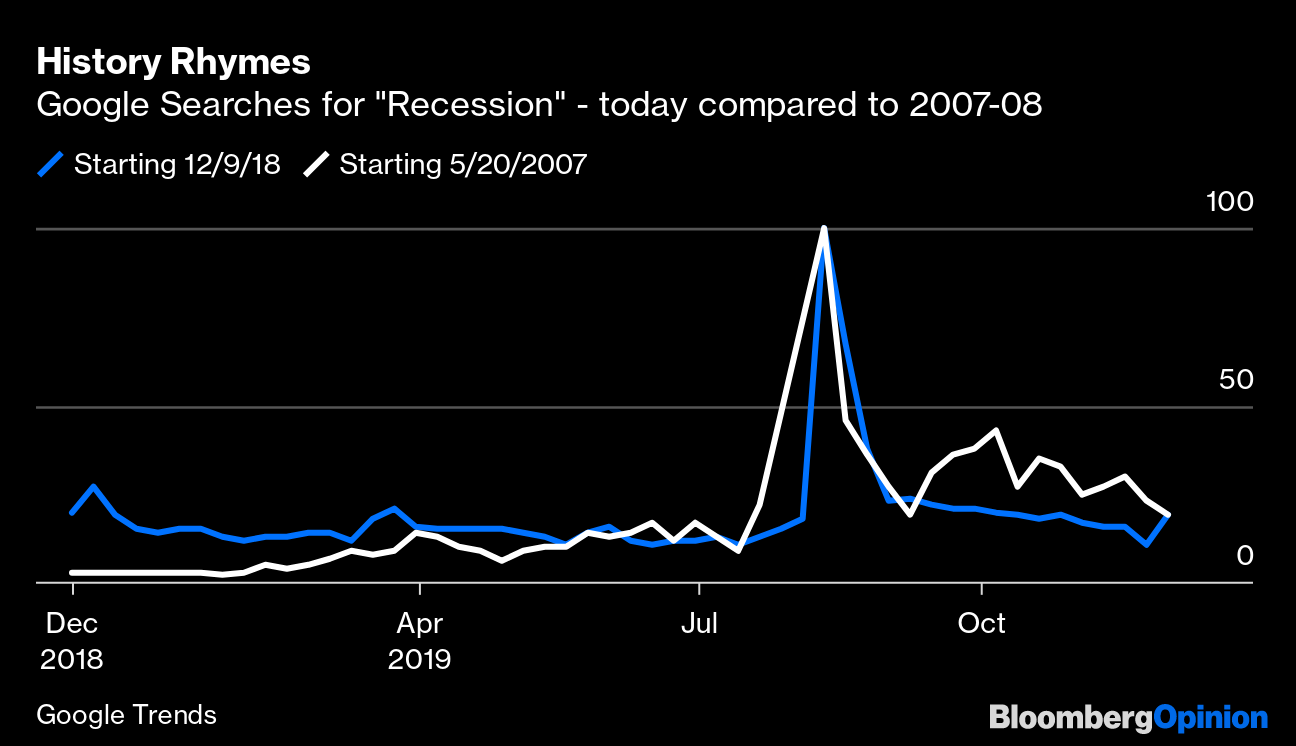

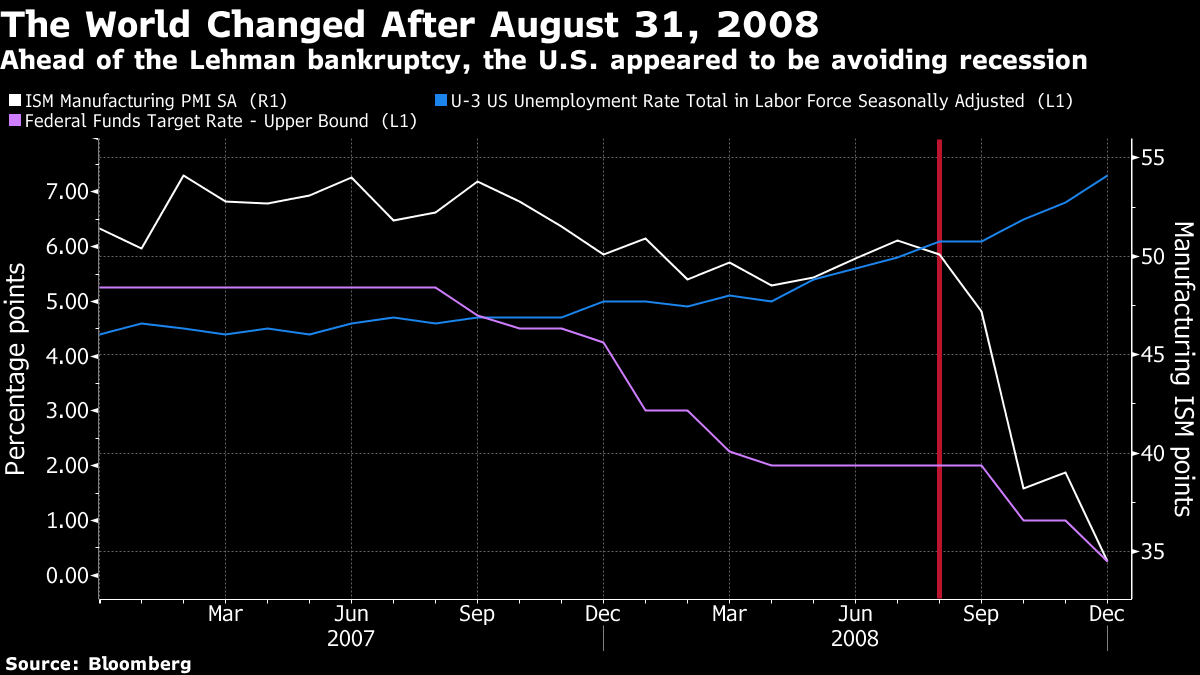

| There is nothing like animal spirits to drive markets. Keynes diagnosed them long ago, and they have a huge impact on trading. Thus, the brief but severe recession fear of midsummer has allowed last week's much more positive data on U.S. employment to feel more like an exit from a recession that has happened, rather than a reduction in perceived risk of one. This is a Google Trends chart on searches for the word "recession" that I published in a column over the weekend. It shows that fears suddenly spiked in midsummer to their highest level since the last actual recession:  The point I was trying to make was that the positioning that investors took on during the summer, as new tariff announcements hit Twitter, the yield curve inverted, and financial markets braced for an instant recession, created the conditions for an excessive bounce. Such powerful relief can translate into much more stronger animal spirits than if fears had persisted at the same contained level. The market might be setting itself up to step on a rake. But there is more to it than that. This morning, I received the following carefully annotated version of my chart via Twitter:  If we look carefully we can see that the last time pessimism reached such a crescendo and then collapsed, in early 2008, it was followed by the worst recession that most of us can remember. Looking further, the following chart shows how Google searches for recession have moved over the past year, compared to the 12 months starting on May 20, 2007. (Yes, I chose the date to align the two peaks, but the pattern is remarkably similar):  In May 2008, after the fire sale of Bear Stearns and with the market for structured credit melting down, people had calmed down as much about the risk of a recession as they have in the months since the summer sell-off. In both cases, online searchers' interest in recessions has dropped by 80%. With the benefit of hindsight, it might seem that people were mad back in 2008. The warning signs were obvious. But if we look at the data, it wasn't quite so mad as it first appeared. The main data on employment and manufacturing surveys wobbled, but stayed the right side of recession. In the first week of September 2008, only a week before the crisis would come to a head, it looked as though the economy was muddling through, with the help of some aggressive easing by the Federal Reserve:  Meanwhile, optimism that recession could be averted had an extraordinary effect on financial markets. The following is possibly my favorite chart to illustrate the global insanity of 2008. It shows the relative performance of Brent crude futures versus the KBW index of big U.S. banks. Versions of this trade were popular with hedge funds at the time. The idea was to go long oil, or anything else that took advantage of booming commodity prices, while selling short U.S. banks. Investors correctly foresaw that horrors would befall the U.S. banking sector — but they incorrectly assumed that commodity markets, and ultimately the global economy, would be immune. The belief that the U.S. banking system could collapse in a world separate from the rest of the global economy persisted until Bastille Day, July 14:  Amazingly, by the end of the year shares in U.S. banks had held their value better than oil had done. There are more similarities between 2008 and today. In both cases, a rupture in the financial world led to fears for the real economy. In 2008, the market spasm was driven by Jerome Kerviel, the rogue trader at Societe Generale SA. The jitters eased once it became clear why there had been sudden and aggressive selling in Europe. This time around, the yield curve inversion, following the stock sell-off at the end of last year, prompted the fear. Since then, the data have improved (although manufacturing looks weaker than it did on the eve of the Lehman Brothers collapse), and the yield curve has un-inverted (which it always does before a recession), while concerns over the trade war have abated (for no obvious reason). From the U.K., the risk of a chaotic "no-deal" exit has receded almost completely — at least until the end of next year. And of course the Fed has cut rates twice more since August. To be clear, there is nothing in the global economy that should cause us as much concern as the parlous state of the U.S. and European banking sectors in 2008. But the surge in recession fear, and the eager rush to bottle that uneasiness, is very similar, and suggests the kind of febrile sentiment that might give us something like the market break that saw oil prices crash in summer 2008. Another critical point is that recession sentiment is a lagging indicator. Goldman Sachs Group Inc. noted the spike in Google searches back in August, in a note that was much circulated. Peter Atwater of Financial Insyghts responded with this LinkedIn post including the prescient words: My point is that what many investors think are leading indicators of market behavior are, in fact, lagging. When recession is on the tip of everyone's tongue, it is not time to sell stocks, but to buy stocks. He certainly got that right. When narratives are blisteringly hot, they are probably contrarian indicators. The S&P 500 is up 6% from when he made that post, and more than 10% from the height of the "recession" searches earlier in August. He added: if history rhymes, what we saw last week [the second week of August] looks a lot like the early January 2008 market lows where recessionary fears (as expressed by Google Searches) were the manifestation of falling bond yields and stock prices. People were worried about a recession, not because they felt it directly, but because the financial markets were saying they should be worried about. There was behavioral capitulation at the extreme in sentiment. That now seems a great explanation of what happened in August. It doesn't necessarily mean that we are about to stage a repeat of the second half of 2008. But, there are plenty of banana-skins ahead. Market pricing currently assumes a Conservative majority in the U.K. election (which is likely but far from assured), and a resolution to the trade dispute by the tariff deadline of Dec. 15 (which is possible but seems unlikely). If stocks were priced on the assumption that the banking sector could be ignored in 2008, they now assume that we need not worry about any of the political turmoil around the world. And what we plainly should take from 2008 is that extreme whipsawing of sentiment can set us up beautifully for financial accidents. Let's be careful out there. It's Hard Out There for a Fund Manager; But Great for Monopolies Just what is the most depressing chart out there for an active equity fund manager? Last week I offered this candidate, from Andrew Lapthorne, quant strategist at Societe Generale. It showed that the great majority of stocks globally have failed to beat the S&P 500 over the last two years. I followed it with a candidate from Hendrik Bessembinder of Arizona State University. Over the long term, he shows, most stocks fail even to beat cash.

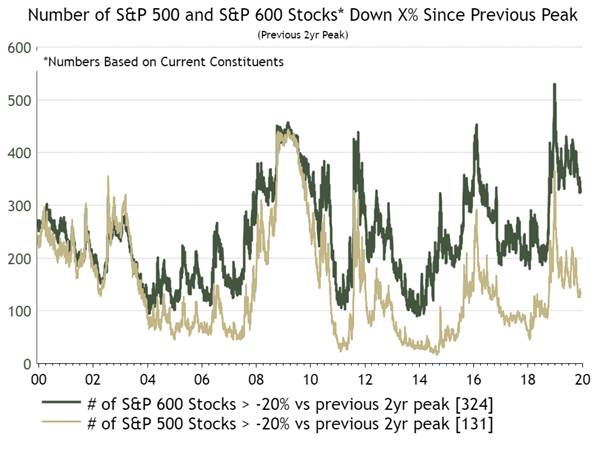

Now more charts pile up to demonstrate how difficult it is to spot a winner, and how easy it is to miss out on a great boom. This from Ian Harnett of Absolute Strategy Research Ltd. shows that more than half of the stocks in the small-cap S&P 600 remain more than 20% below their peak for the last two years. More than 100 companies in the large-cap S&P 500 are also effectively mired in a bear market:

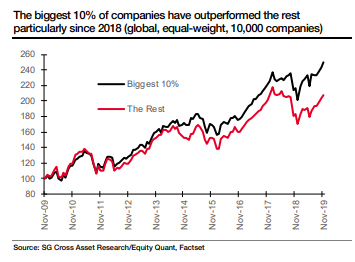

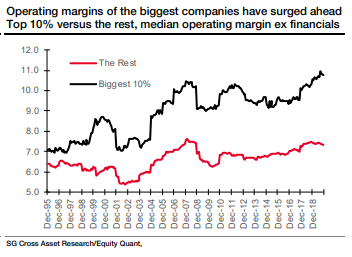

For smaller companies, the pain seems particularly intense. As he shows, their actual (trailing) earnings per share is tanking after the sugar high produced by tax reform last year, while expectations for future sales and earnings have stalled:  That is because the biggest companies are getting things their own way for a change. The "mega-caps" of the Russell Top 50 badly lagged small-caps during the first decade of this century. They are now on their most extended run of outperformance since the bursting of the dot-com bubble in 2000:  Meanwhile, Lapthorne has returned to the fray, and shows that the performance of the biggest 10% of global companies, from a huge sample, has recently gone into overdrive. This is a new and striking phenomenon:  And that in turn rests on the remarkable trend for the biggest companies to be far more profitable than everyone else. The extent of this phenomenon, shown in another Lapthorne chart, is extraordinary:  A quarter of a century ago, the biggest 10% of companies had only a slightly better margin than everyone else. Now, it is more than double. What can explain this? One obvious explanation is: lack of antitrust enforcement. Back in 1995, we might hypothesize, companies weren't allowed to merge with each other to foreclose competition. Now, they can get away with it. That leaves active managers with little choice but to pile into the biggest companies that everyone already knows about. And that in turn forces them to mimic the big index-trackers ever closer, making it ever harder to justify their existence. Lack of government regulation of monopolies has turned formerly great stock pickers into closet indexers. Book Club The problems for active equity managers are, in the scheme of things, one of the less important ramifications of the growth of monopolies. There are many more. And that brings me to the Bloomberg book club. We will be discussing The Myth of Capitalism: Monopolies and the Death of Competition with authors Jonathan Tepper and Denise Hearn in a live chat on the terminal on Wednesday, starting at 11 a.m. New York time. Tepper and Hearn will join from Bloomberg bureaus in London and Seattle respectively. My Bloomberg Opinion colleague Tara Lachapelle will also participate. Please send any comments or questions about the book, or generally on the subject of competition policy and its role in the current discontent with capitalism, to: authersnotes@bloomberg.net. And join us at TLIV on Wednesday morning. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment