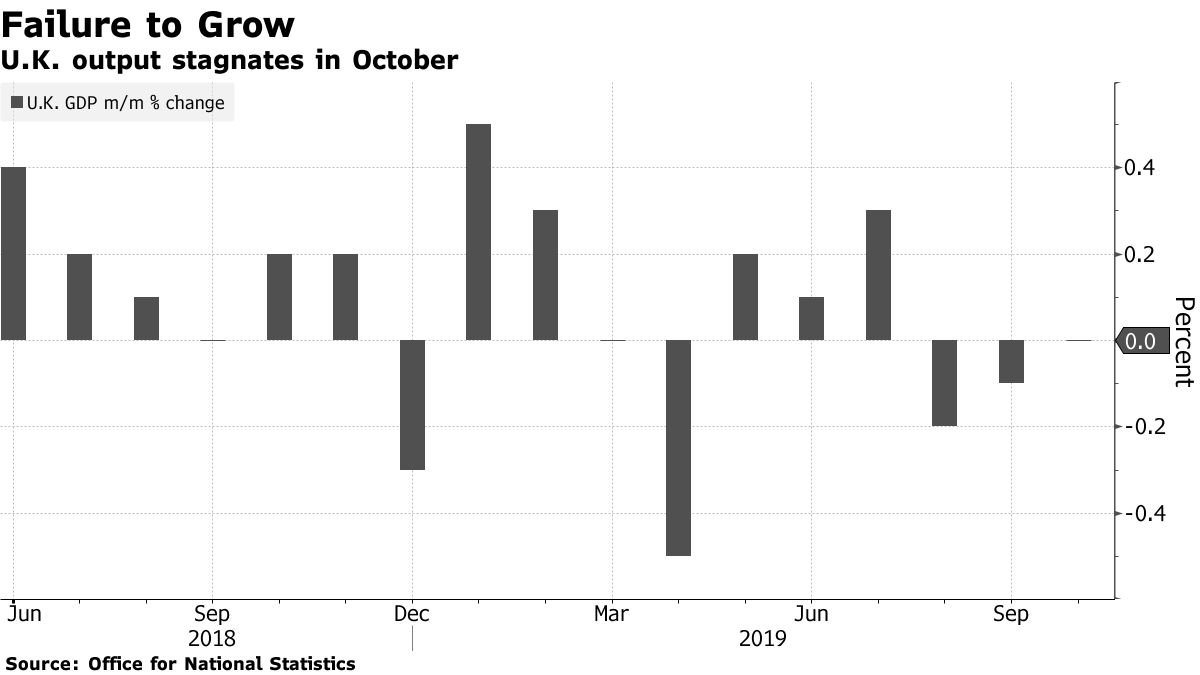

House set to unveil articles of impeachment, Deutsche Bank says it won't need more capital, and repo worries continue. House rules The leaders of the House committees running the inquiry into President Donald Trump will announce two articles of impeachment at a news conference scheduled for 9:00 a.m. Eastern Time. One centers on the abuse of power and the other lays out charges relating to the obstruction of Congress, according to people familiar with proceedings. Trump is all but certain to be acquitted by the Senate, where Republicans hold a majority. Separately, the Justice Department's inspector general found the Federal Bureau of Investigation acted properly when it began a broad investigation into candidate Trump in the run-up to the 2016 election. We're fineDeutsche Bank AG is holding its first investor day in four years today as Chief Executive Officer Christian Sewing tries to convince the market his strategy for the lender is on track. He said the bank would be able to execute one of the largest restructurings in its history without having to tap investors for more funds. Deutsche Bank shares slipped in German trading. Elsewhere, Morgan Stanley has been fined 20 million euros ($22.1 million) by French regulators who accuse the firm of rigging the country's bond markets. ZeroThe U.K. failed to produce any growth in the third quarter, leaving the country on course for an expansion of little more than 1% this year as Brexit uncertainty continues to take its toll. The feeble result is unlikely to change the momentum behind Prime Minister Boris Johnson's campaign to gain an overall majority in Parliament in Thursday's election. For markets, it seems that even a Johnson victory would not be enough to lend a further boost to the pound. Markets lower Equity investors are becoming more cautious as the deadline to the next round of China tariffs runs down. Overnight the MSCI Asia Pacific Index slipped 0.2% while Japan's Topix index closed 0.1% lower. In Europe, the Stoxx 600 Index had dropped 0.8% by 5:45 a.m. in a broad-based reversal. S&P 500 futures pointed to some selling at the open, the 10-year Treasury yield was at 1.816% and gold was higher. Repo reduction Yesterday's New York Fed liquidity operations did little to quell the outstanding worries about the health of the U.S. repo market, with all three auctions oversubscribed. The next crunch point is Monday Dec. 16 when the Treasury distributes new U.S. debt to investors, also the day after new tariffs on China may be implemented. One of the big problems in the market at the moment is the continued falling cash levels at banks, making a liquidity crunch more likely around year-end. Zoltan Pozsar, a Credit Suisse Group AG analyst, warned that this could lead to a spike in Treasury yields. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Joe's interested in this morningThe U.K. economy is growing at its slowest pace since 2012. With uncertainty and disruptions caused by Brexit likely to persist (regardless of what happens in this week's general election), this looks like a country that needs fiscal stimulus. And it will probably get it in some form or another after the vote. On this note, yesterday, Tracy Alloway and I talked to Lord Robert Skidelsky, the famous Keynes biographer, and author of a new book titled Money and Government: The Past and Future of Economics. The interview won't be out for a few weeks (so subscribe to Odd Lots here) but he made a comment about fiscal stimulus in the U.K. and elsewhere that was particularly timely so I'll mention it here now. Ultimately, while he believes that there is a need for fiscal authorities to play a greater role in boosting the economy, these type of election-season promises are counter-productive. All you're doing when you make the issue of spending an election gambit is moving from the animal spirits of the economy to the animal spirits of the political system, neither of which gets you to a state of economic stability. What's needed is not "stimulus" per se, but a permanent role for public money: Robust fiscal stabilizers that don't depend on who's in power and persistent public investment in areas like infrastructure and R&D. That permanent, credible role, he argues, is what's needed... not just having the government fill up a money hole every time there's a slump and politicians need to get re-elected.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. Before it's here, it's on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can't find anywhere else. Learn more. |

Post a Comment