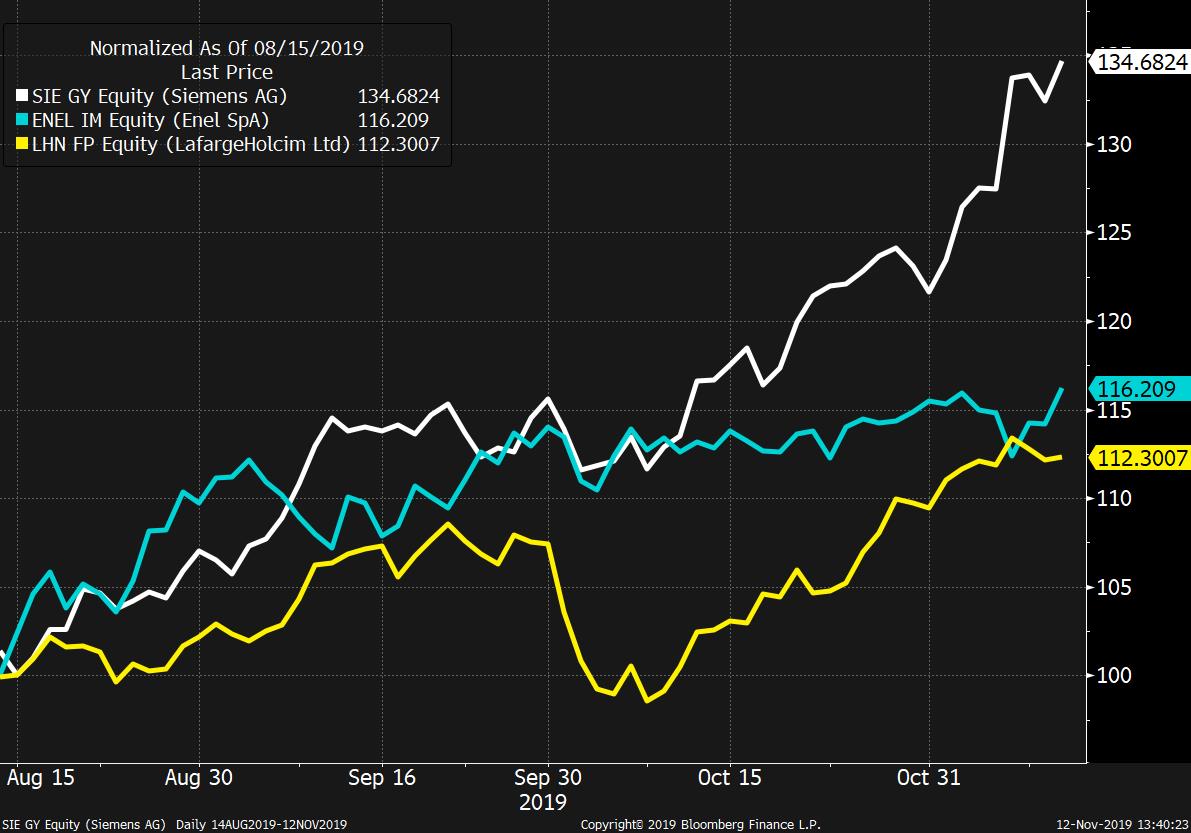

| Wall Street awaits Powell testimony, public impeachment inquiry hearings begin, and another warning on oil demand. Powell's turn In his speech to the Economic Club of New York yesterday President Donald Trump renewed his assault on the Federal Reserve saying the bank was hurting the U.S. by not cutting rates into negative territory. Fed Chairman Jerome Powell will get a chance to give his views in Washington when he appears before Congress's Joint Economic Committee at 11:00 a.m. Eastern Time. While analysts expect him to maintain the cautiously optimistic approach outlined after the October policy meeting, investors now see increasing chances that rates may remain unchanged throughout 2020. Impeachment inquiry If Powell is going to capture Wall Street's interest today, another event on Capitol Hill is likely to command the wider public's attention: Hearings to determine whether President Trump abused his office and should be impeached at 10:00 a.m. Top U.S. envoy to Ukraine William Taylor and Deputy Assistant Secretary of State George Kent are due to testify in a session that also holds risks for Democratic presidential contenders as Republicans seek ammunition to attack former Vice President Joe Biden. And six senators in the running for the nomination may be forced off the campaign trail at a crucial moment as they would be jurors in a trial. Oil plateau Saudi Aramco's prospectus last weekend re-ignited the discussion over peak global demand for crude, with the company citing a forecast that sees a top within the next 20 years. The International Energy Agency painted an even grimmer picture in its latest long-term World Energy Outlook, saying it now sees demand for oil hitting a plateau in about a decade. The forecast suggests current growth levels will continue for the next five years, then start to slow significantly as the use of oil-based passenger cars drops. Investors more concerned about short-term demand effects are pushing the price of a barrel of crude lower this morning as doubts over trade cloud the outlook. Markets slip The lack of an announcement on trade progress in President Trump's speech yesterday continues to weigh on markets. Overnight the MSCI Asia Pacific Index dropped 0.8%, with Hong Kong's Hang Seng closing 1.8% lower as protests continued to grip the city. In Europe, the Stoxx 600 Index was 0.6% lower at 5:40 a.m. with automakers among the worst performers following no word on the delay of threatened U.S. tariffs on the region's car industry. S&P 500 futures pointed to a drop at the open, the 10-year Treasury yield was at 1.876% and gold was recovering some ground. Coming up... U.S. inflation data for October is expected to show no change from the previous month, with the headline number staying at 1.7% and core at 2.4% when it is published at 8:30 a.m. The monthly budget statement will be released at 2:00 p.m. In keeping with the strong political theme in today's news, Trump will welcome Turkish president Recep Tayyip Erdogan to the White House, the first meeting between the leaders since the beginning of Turkey's military offensive in northern Syria. As well as Powell, we will also hear from Minneapolis Fed President Neel Kashkari and Philadelphia Fed President Patrick Harker later. Earnings are from Canada Goose Holdings Inc. and Cisco Systems Inc. What we've been reading This is what's caught our eye over the last 24 hours. And finally, here's what Joe's interested in this morning The other day I made a joke on Twitter about how exciting American companies are (Beyond Meat! Square! Amazon!) and how relatively boring European companies are (Siemens, DaneGlass, NordSteel). Ok, DaneGlass and NordSteel don't actually exist, but nobody would blink because so many companies seem to be some former state-run industrial giant, or quasi utility, whose stock hasn't gone anywhere in a long time. But then I looked at the chart of Siemens, and two things stood out to me. One is that over the long term, especially when you include dividends, it's been a fantastic performer. And second is that in the last several weeks, the stock's been on an absolute tear. It's up 33% since the middle of August. Then I started looking around and noticed there were a bunch of pretty charts in Europe. Check out, for example, LafargeHolcim, the big French building materials company, which rose about 14% from its low last month. Or the Italian energy and gas company ENEL, which has been like a straight line up year. This is the season of rotation, of course. The big theme in the U.S. has been the shift from growth stocks to value stocks. While they might not grab the headlines the same way, those boring old European companies that don't get many pageviews are suddenly right in the sweet spot of what investors want, as profit-less growth is out, and cyclical recovery is back in style. And the lesson to me, regarding my tweet is, never joke! Or at least fact-check all jokes before sending them.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. Before it's here, it's on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can't find anywhere else. Learn more. |

Post a Comment