Welcome to the Weekly Fix, the newsletter wondering if Brian Moynihan will end the market's obsession with trading banks off the 10-year yield. –Luke Kawa, Cross-Asset Reporter

Down the Middle

Market participants were seemingly betrayed on July 31, when Federal Reserve Chairman Jerome Powell suggested that the central bank's first interest-rate reduction in nearly a decade was part of a "mid-cycle adjustment" rather than a full-blown easing cycle. Fast forward a couple months, and the price action is increasingly a story of traders coming around full-circle to the Fed's view – and implicitly acknowledging that a shallower-than-previously-anticipated easing cycle is a positive development.

January 2020 and 2022 federal funds futures imply just 30 basis points of easing over this period – less than half of what was priced in six weeks ago, or what was foreseen before the Fed's first cut:

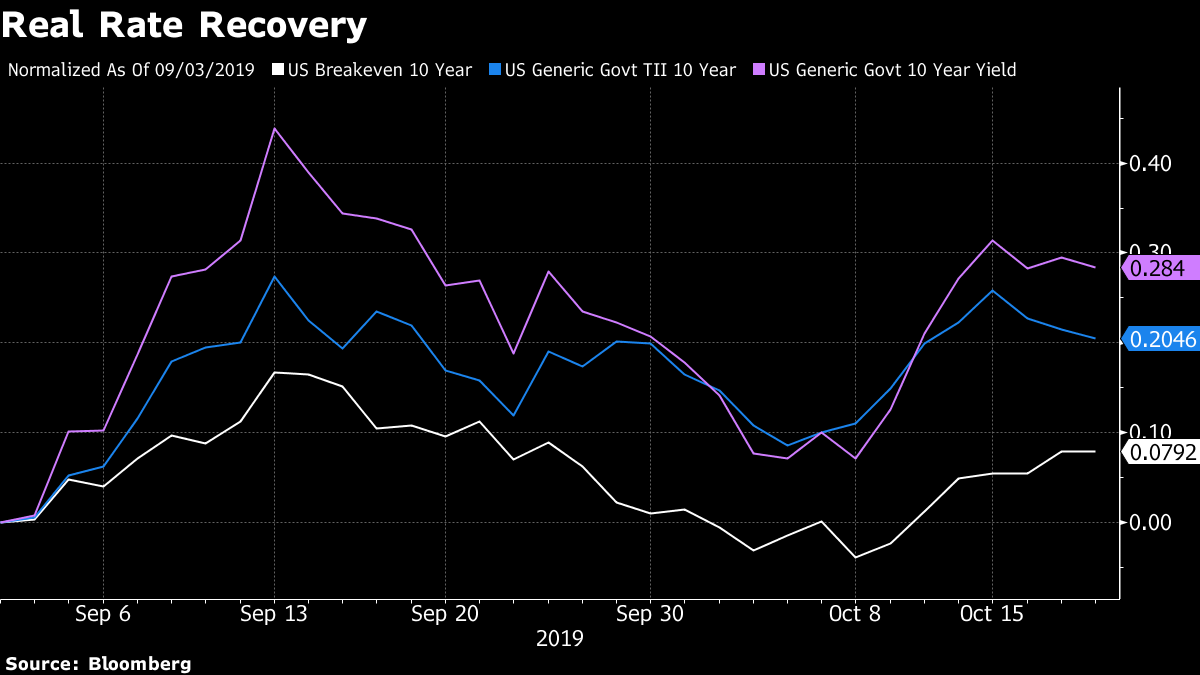

Investors are signaling belief that less monetary accommodation will be required, rather than necessarily anticipating full-bore reflation. Consider the decomposition of the 10-year Treasury yield's move off of its 2019 lows: most of the gain is in real rates, with breakevens posting a much smaller advance.

Similarly, while the cost of options that protect against inflation averaging sub-2% over the next five years has retreated meaningfully, inflation caps that protect against the opposite dynamic remain very depressed and near cycle lows:

The lack of reactivity to episodes of underwhelming U.S. data this week (Treasuries have preferred to take their cues from the twists and turns in the relatively constructive Brexit talks) suggests that the risks have become a little more balanced in the bond market's eyes.

To this end, three-month, two-year swaptions are starting to settle down relative to their 10-year counterparts. That is, the range of opinions as to the timing and depth of the Fed's easing cycle have recently been compressing more meaningfully than the outlook for longer-term rates (with the caveat that swaptions are elevated for both tenors relative to their five-year history, especially at the front-end).

After four instances of (at last) 25 basis-point-swings in the 10-year yield over the past two months, perhaps a semblance of stability might be creeping back into the Treasury market.

Record Money in the Banks

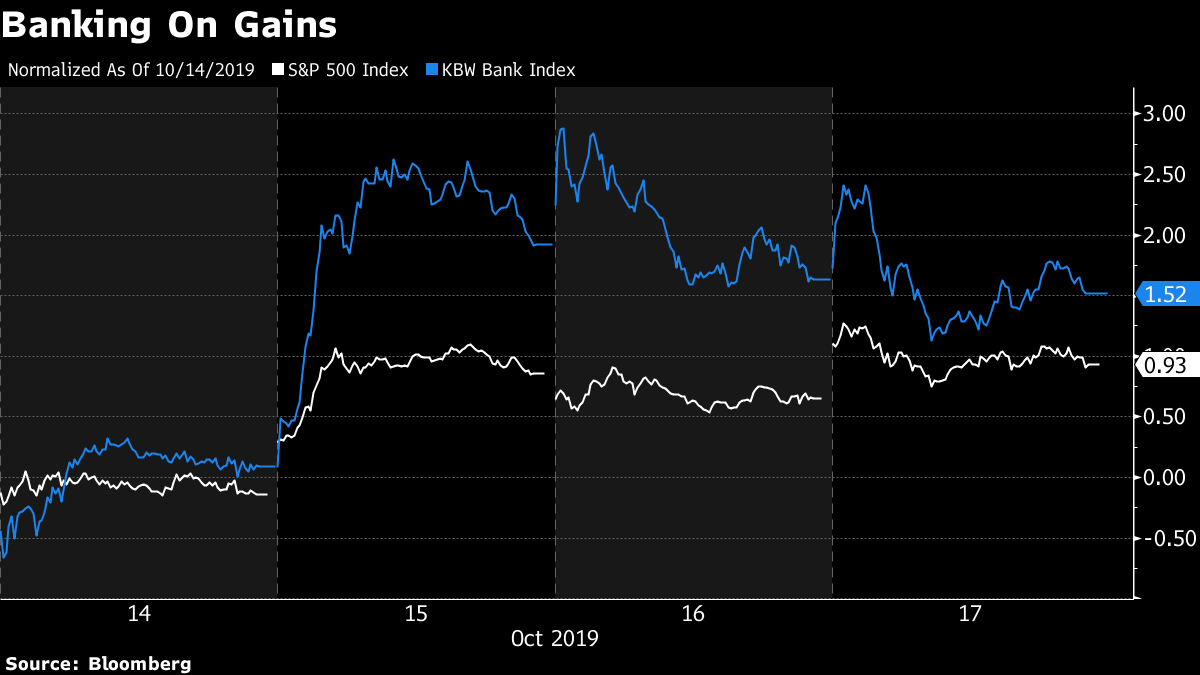

Ten-year U.S. yields ended September little more than a third of a percentage point from all-time lows. And yet, America's big banks are on track for a record year of profits after the latest quarterly reporting period.

Better-than-expected results and a modest uptick in yields have provided the fuel for U.S. bank outperformance so far this week.

To be clear, the interest-rate environment was referred to as a headwind throughout quarterly conference calls. While it's not ideal, it's certainly not crippling. Here's what else executives said about the yield backdrop:

JPMorgan Chase & Co. Chief Financial Officer Jennifer Piepszak:

The expectation is for investment banking fees "to be down both sequentially and year-on-year, driven by strong performances in the third quarter and prior year, however, the pipeline remains healthy as strategic dialogue with clients is constructive, equity markets remain receptive to new issuance and the lower rate environment has made debt issuance more attractive."

Citigroup Inc. CFO Mark Mason:

"As we saw the rate environment increasing a year or so ago, we didn't see the benefits of that."

"Similarly, as we see rate cuts play out, we're not going to see that play through either."

Wells Fargo & Co. CFO John Shrewsberry:

"Deposit cost will be cheaper in the fourth quarter."

That said, "if rates continue to move down on the asset side it still works against us, even if deposit costs aren't rising."

Summing up, there is some upside in other parts of the business associated with lower interest rates, the sensitivity for some institutions might not be that immense in either direction and the real trouble so far might have been the lack of downward adjustments in funding costs.

And here's Bank of America Corp. Chief Executive Officer Brian Moynihan, after numerous questions about his institution's sensitivity to lower interest rates, with the cherry on top:

"There has been more rate cuts and we're still holding the same guidance of $12 billion-and-change."

"We're managing the heck to try to avoid some of these impacts."

"There's just a lot of moving parts that frankly we've managed better than we thought we could."

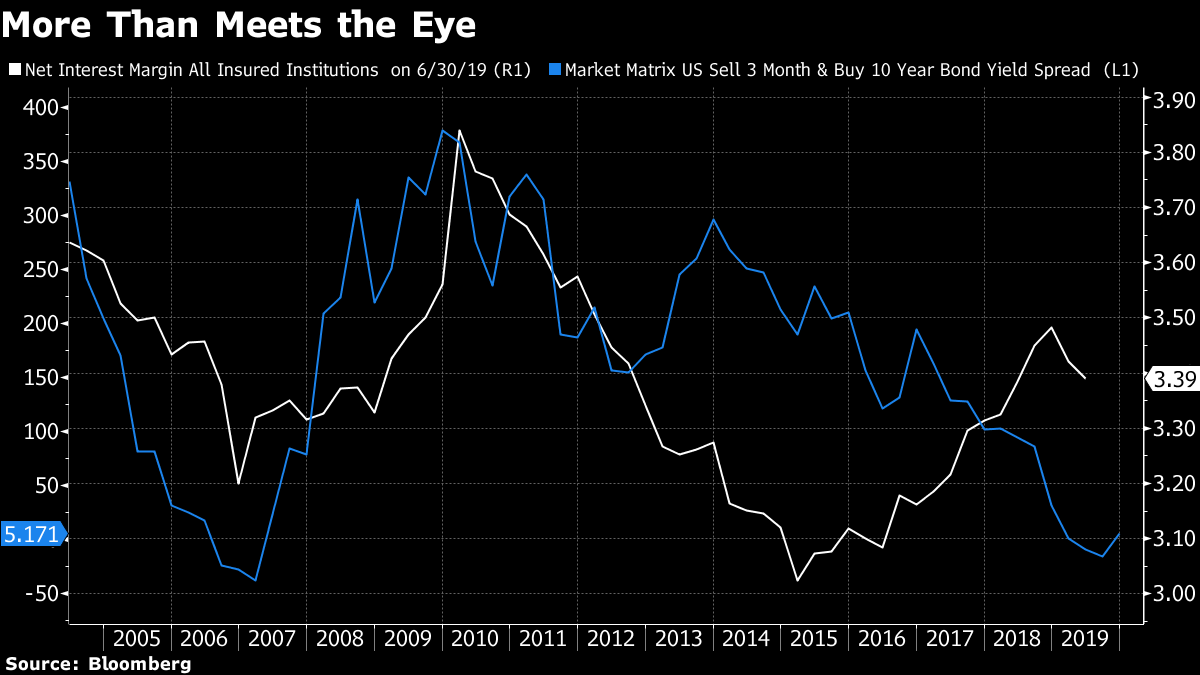

The level of rates and rate differentials are not the end-all, be-all for banks' profits. And seeing as banks elected to maintain guidance pertaining to net interest income despite a more than 30 basis point drop in the 10-year yield in the third quarter, the proof seems to be in the pudding. Financial institutions engage in maturity and risk transformation, so mapping out margins isn't as simple as tracking the Treasury curve and level of rates. In addition, non-interest income is "A Thing."

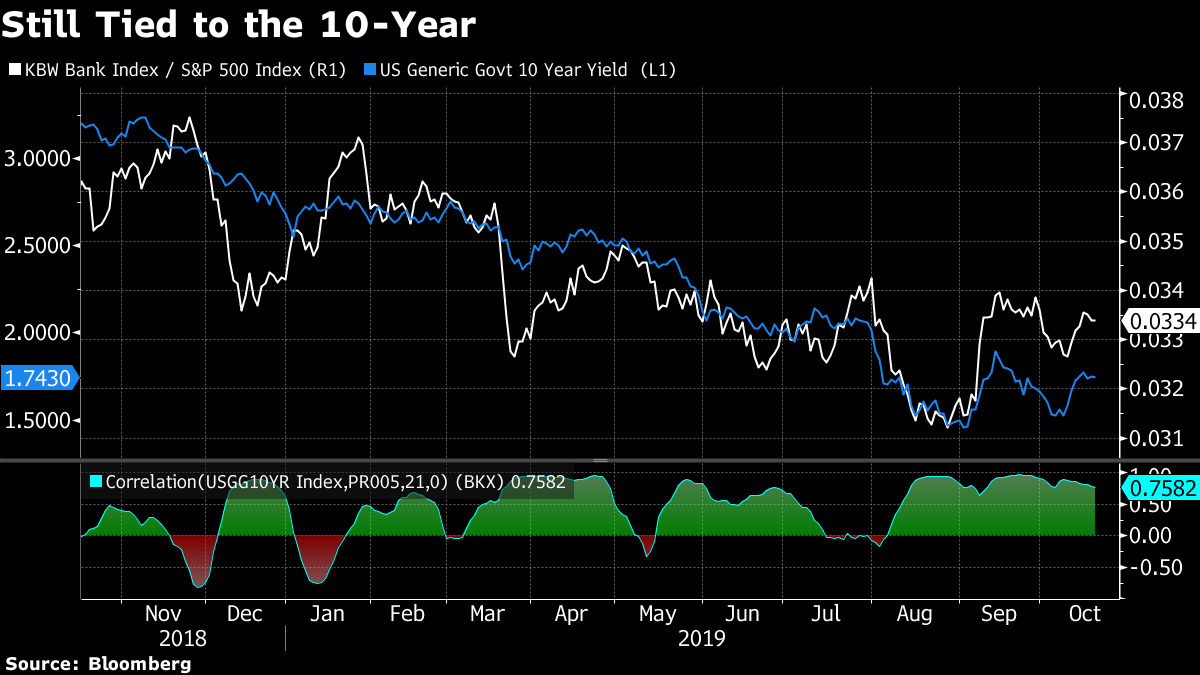

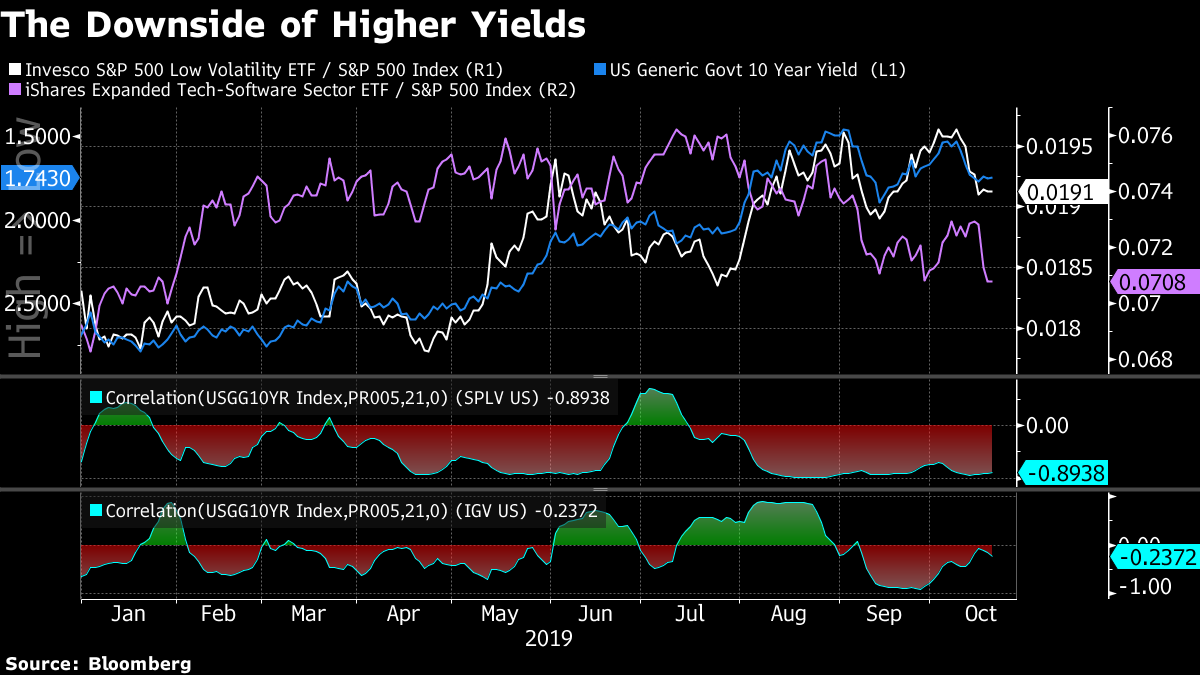

Alas, it's tough to convince the market of that: the relative performance of bank stocks has been very much tied to the level and direction of the 10-year Treasury yield.

Post a Comment