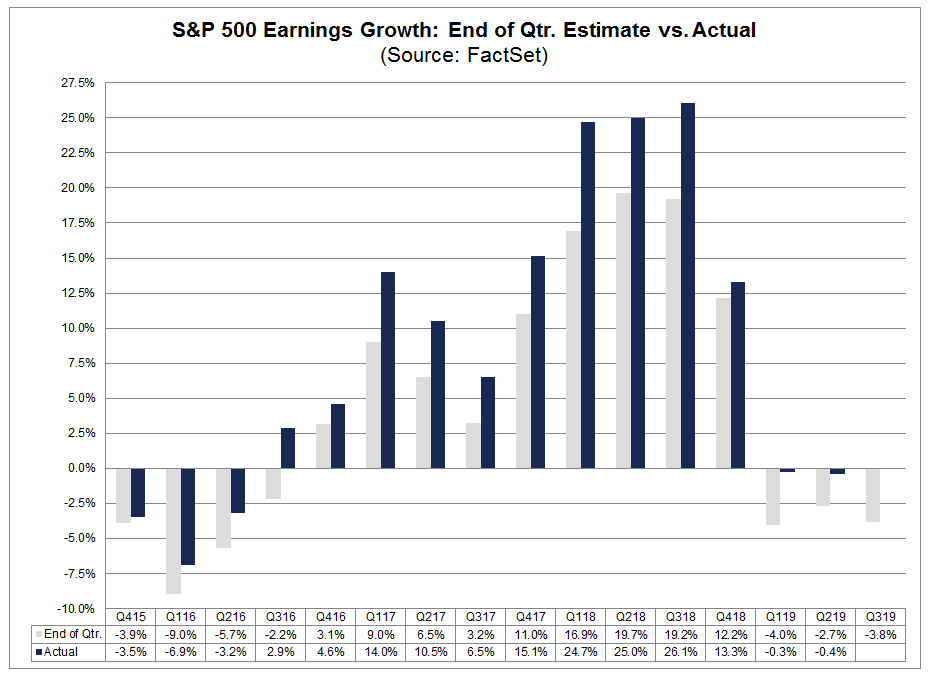

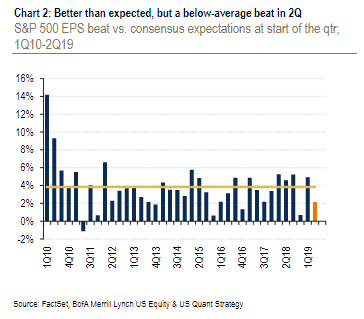

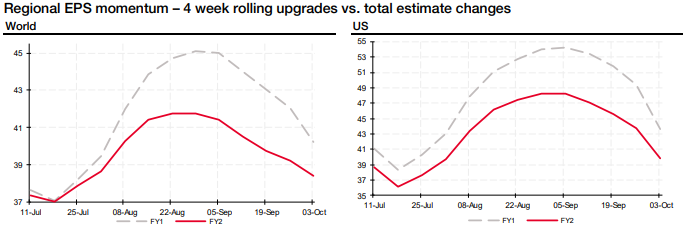

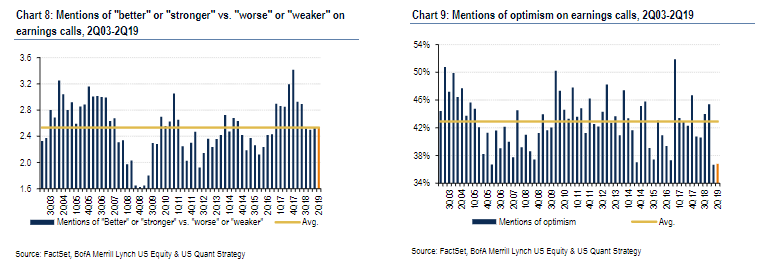

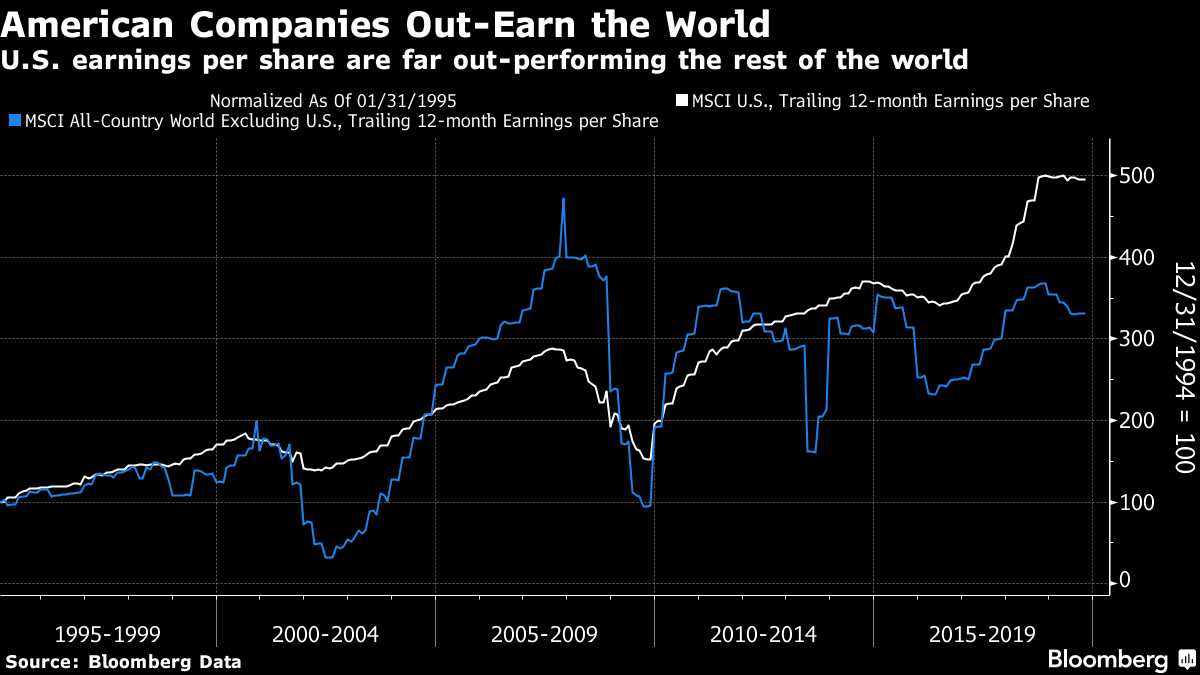

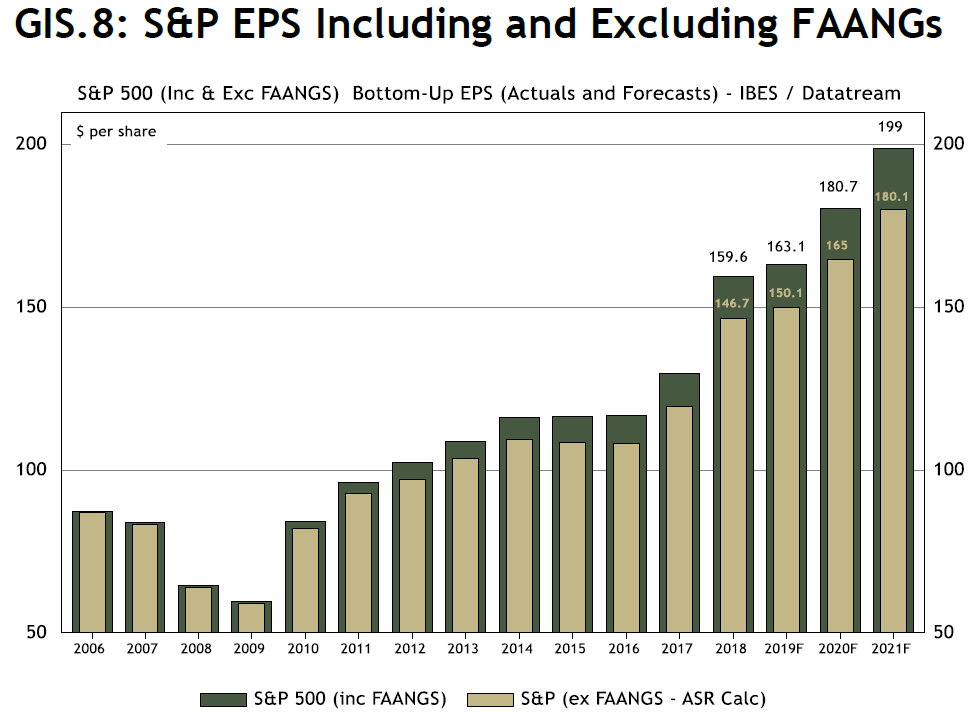

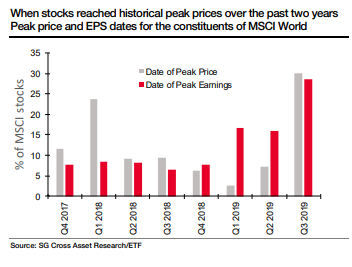

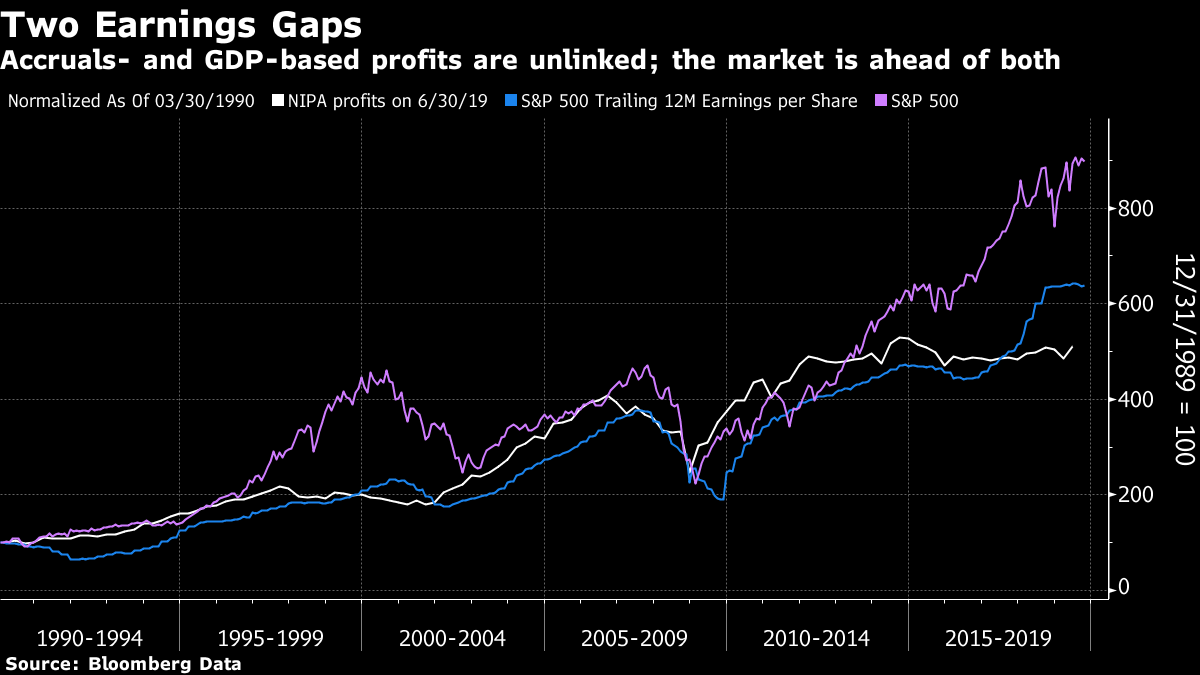

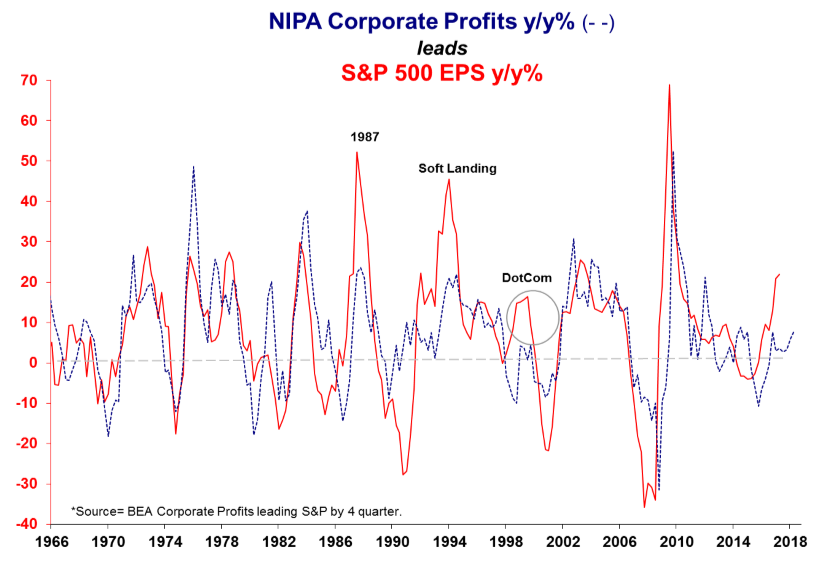

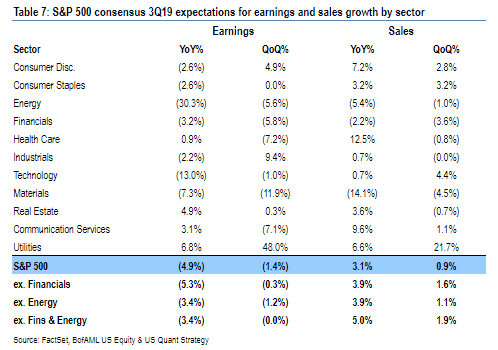

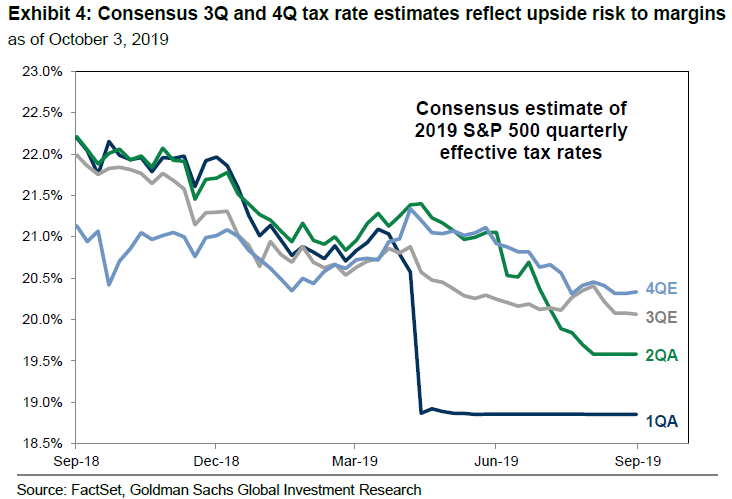

Earnings Divide The third-quarter reporting season is about to break out, and Wall Street brokers have made sure their clients are braced for an outright decline in earnings per share compared to a year ago. If that happens, this would be the third quarter in a row – although things were very close in both the first two quarters of this year. These are expectations as recorded by FactSet:  What should we expect? First, companies' investor relations departments are good at their job, so you can be sure that the final outcome will beat expectations. After all, companies that deliver a positive earnings "surprise" after manipulating forecasts lower see their share prices rise on the day. Savita Subramanian at Bank of America Merrill Lynch shows that in the aggregate, negative surprises just don't happen:  However, some negativity about earnings is meaningful. As Andrew Lapthorne of Societe Generale SA records, downgrades by companies have accounted for a larger share of corporate announcements as the reporting season approaches. Weak earnings "momentum" is visible both in the U.S. and elsewhere:  Meanwhile, when we last heard from executives on earnings calls for the second quarter, their tone was noticeably negative – at a point when it's not necessarily in their interests to talk down expectations. This is Subramanian of BAML's running total of mentions of "optimism" by executives in calls:  But rather than playing games with earnings forecasts, investors should focus on whether U.S. profits can possibly make sense. The earnings per share that American companies report are diverging ever further from what should be sensible comparisons. This chart shows how the MSCI U.S. index's EPS moved over the last quarter-century, compared to EPS for its index of the rest of the world:  The rest of the world is more volatile, thanks to greater dependence on variable commodities markets. But the current divergence, with the U.S. in the lead, is quite remarkable. And Absolute Strategy Research of London shows that the phenomenon of the "FAANG" dominant internet stocks only partially explains the divergence – even excluding them, U.S. earnings are expected to post strong gains this year and in 2020 and 2021:  For the developed world as a whole, earnings at some 70% of companies are lower now than two years ago, and roughly as many remain below their peak share price for the last two years, as this chart from SocGen's Lapthorne shows:  There are even more profound earnings gaps. The numbers on corporate profits in the National Income and Profit Accounts, or NIPA, have stagnated throughout the post-crisis decade. These are compiled by the Bureau of Economic Analysis as part of its calculations of gross domestic product. By contrast, the S&P 500's profits under accruals accounting have moved ahead, while share prices have risen far faster than either:  There are reasons why earnings calculated under the two methods will diverge from time to time, but this is extreme. If anything, NIPA tends to be a leading indicator. This chart, from Stephanie Pomboy of MacroMavens LLC in New York, shows annual changes for the two series, with NIPA 12 months ahead. The last time the two series diverged so widely was during the dotcom bubble.:  The disparity is largely due to financial engineering. Taxes, interest, and a declining share count all help to reduce reported earnings per share without affecting the NIPA series. Beyond the financial engineering, there's little evidence from the NIPA data that corporate America is as strong as it appears. Then there's the issue of margins. Over history, margins have a strong tendency to revert to the mean – a trend mainly driven by the economic cycle, and by the relative bargaining strength of managements and the workforce. Margins have been high for a while. Subramanian of BAML points out that this is one of those rare quarters where sales are expected to perform better than earnings. In other words, margins are expected to tighten – which should be no surprise given the strong labor market.  There are caveats to the gloom. A few companies, led by recently scandal-stricken aerospace group Boeing Co., have pre-announced poor results that weigh down the S&P 500 as a whole, while the heavily cyclical semiconductor sector is expected to sustain a lot of pain. The median S&P 500 company is projected to raise EPS by 3%, according to David Kostin of Goldman Sachs Group Inc. Tax might easily surprise on the upside. Kostin points out that companies reported far lower effective tax rates in the first two quarters than investors had expected. Despite that, they are braced for a higher effective tax rate in the third quarter – opening the chance for companies to surprise positively once again.  The gloom that precedes it does set up this earnings season to provide excuses to buy, as many brokers love to point out. But the difficulties remain. High multiples in the U.S. presuppose optimism that earnings will grow in the future. And yet there is ample reason to doubt whether the gains made so far are sustainable, or even real. So in the final analysis, investors prepared to buy at those multiples must heed the warning of Morrissey, and Kirsty McColl: You just haven't earned it yet, baby. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment