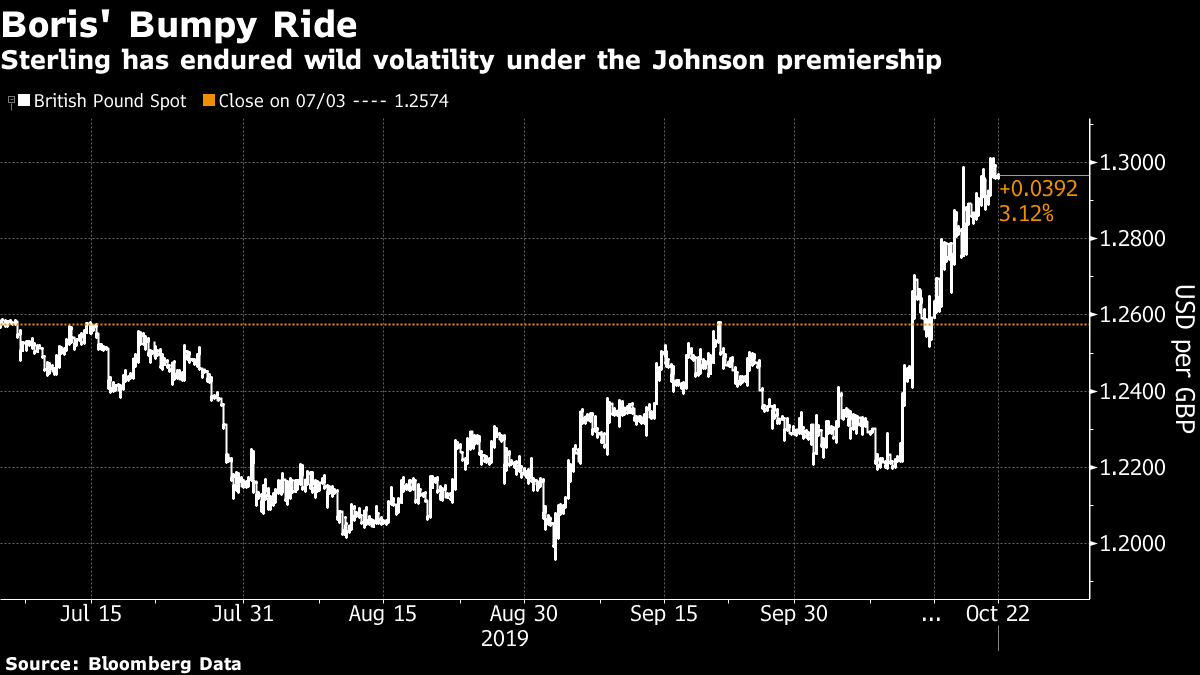

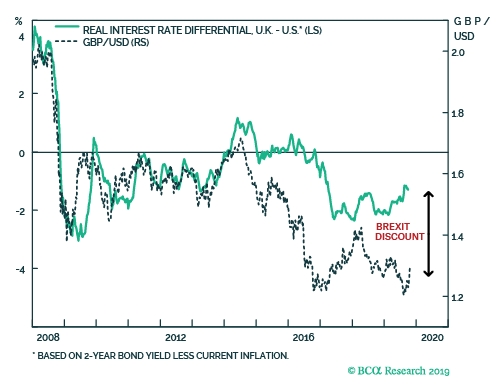

Brexit from Boris to Bercow Yet more political excitement over Brexit, and yet more strength for the pound. While in the City of Westminster the prime minister was discovering that he had been supplanted as the nation's most powerful man by John Bercow, the speaker of the House of Commons, traders in the City of London a mile to the east saw no reason to sell sterling. The currency even breached $1.30 for the first time in Boris Johnson's wild ride as prime minister:  On this occasion, it looks like the markets have it right. The U.K. is in unprecedented constitutional territory, and a general election is likely within months. That could conceivably see figures from the ideological left or the avowedly nationalistic right in power, and offers plentiful opportunities for unstable coalitions that would leave up in the air many vital decisions for the nation's future. Despite all this, it makes sense for sterling to strengthen. First, remember that the pound starts extremely cheap, due to the horrors that the U.K. has chosen to inflict on itself over the last few years. Fair value in the foreign exchange market is a slippery concept, but one of the main yardsticks used by traders involves rate differentials. If one country offers much higher rates than another, it will tend to attract money and so its currency will tend to strengthen. The following chart from BCA Research Inc. shows the spread in real rates between the U.S. and the U.K., which the pound-dollar exchange rate has tracked closely. They began to come detached in 2014, as investors positioned for higher rates ahead in the U.S. — and then the June 2016 referendum scrambled the signal completely:  There is a plainly a "Brexit discount" of some size. That has moved for about a year now in response to one single, binary risk: Will the U.K. drop out of the EU without a deal, or not? If the U.K. leaves via a deal under the process established by the EU, it enters into a transition period, and nothing changes immediately. Without a deal, the changes are immediate, and could easily lead to serious problems, such as traffic pile-ups at English Channel ports. With "no deal," the U.K. starts trading with its closest neighbors on the basic tariff terms laid out by the World Trade Organization, and these become the baseline for subsequent negotiations that could take years. With a deal, tariffs stay unchanged pending negotiations over the future trading relationship. I labor this point because the one constant from the events of the last two months has been to reduce the risk of "no deal." The September parliamentary move to force the prime minister to request an extension of EU membership if he could not agree a deal by Oct. 31 was meant to reduce the risk of no deal. So was the Saturday decision to defer a vote on Johnson's accord until all the legislation to enable it had been passed. Monday's developments, with Johnson blocked from putting his deal to another vote, continue the pattern. There's a real risk that the Oct. 31 deadline will be missed, and Johnson has staked much political capital on this. But for anyone trading foreign exchange, it need not matter much. The EU would almost certainly allow an extension if parliament was in the middle of confirming a deal. If the moment of a negotiated exit is postponed by a few days, the economic effect would be nil. So while the alternatives for the state of British politics and the country's future relationship with the EU continue to proliferate, the overriding point for sterling is that the chance of a no-deal exit continues to dwindle. It might yet happen, but the odds look slimmer than at any point in months. The discount for this risk has been almost eliminated. It's now worth looking at what might stop the pound from closing the "Brexit discount." George Saravelos, global head of FX strategy at Deutsche Bank AG, suggests that sterling could make it to $1.35, but this would depend on two factors: - How long will the transition period be? At present it's due to elapse at the end of 2020, which could be prohibitively short to negotiate a new free-trade agreement. An extension to the end of 2022 would be popular with the market, according to Saravelos; and

- What type of relationship with the EU would a new government be looking for after the general election?

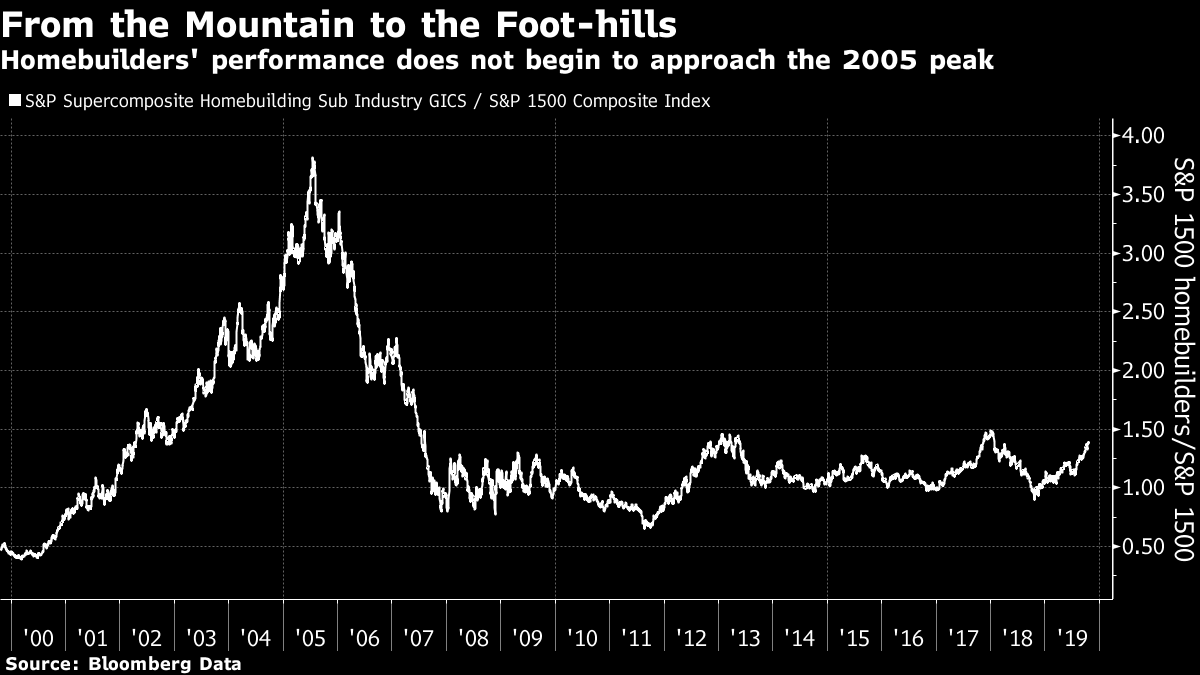

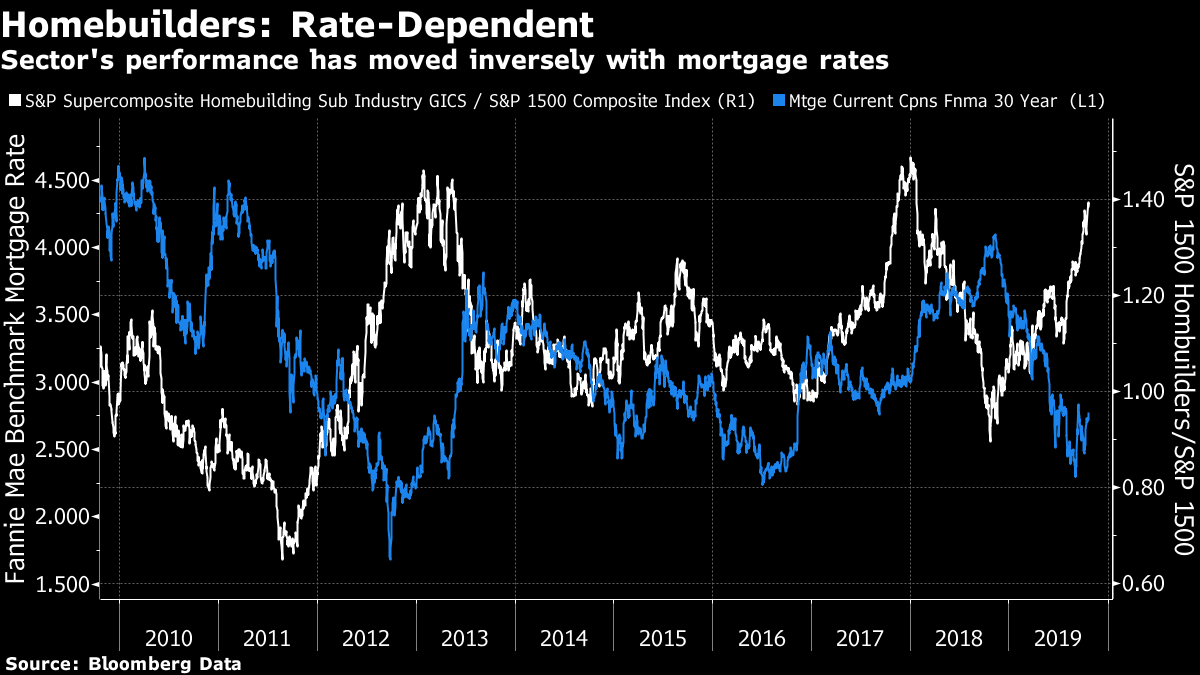

Neither question will be answered quickly, and the range of answers to the second is bafflingly complex. In the long term, sterling looks cheap enough on the fundamentals that it should be a "buy" — provided buyers can wait out what could be an even more dramatic medium term. Sterling's gains should remain intact. But there may be many more months of fractious political debate before it can appreciate further. An American's Home…. U.S. homebuilder stocks hit their highest level since 2006 on Monday. As they close in on the all-time high set at the top of the housing bubble, it probably gives us all some unpleasant memories. But we shouldn't be too concerned. First of all, if we look at homebuilder stocks in comparison to the market as a whole, they are still merely undulating. This is nothing like the mad peak they hit in 2005.  Further, this ride has been driven by low interest rates, rather than high house prices. Mortgage refinancing is running at more than double its volume for the same period last year, so this makes sense. For the post-crisis decade, homebuilder share prices and mortgage rates have had an inverse relationship:  There are many reasons for anxiety about the future of the world economy. The U.S. housing market isn't one of them. Its continued health should buoy the American consumer. If western consumers have taken over from Chinese industrialists as the world's premier drivers of growth, this is good news. Investment Culture: It's a White Man Thing "Culture" can be an irritatingly imprecise and squishy term, but that's not to say it doesn't matter. If the culture around you leads you in a particular direction, that is the way you will probably go. There are also more precise ways of looking at the phenomenon of groupthink, which has been picked apart by behavioral economists. Put together a homogeneous group of people, and they will all think the same way, questionable judgments will go unchallenged, and mistakes will be made. Academics have run experiments showing that investment decisions are better if groups are more diverse, either by ethnicity or gender, while the few hedge funds that include women tend to do better for it. This comes to mind following weekend reading of two excellent pieces that diagnosed problems with the culture at well-known investment groups. An article by my old friends at the Financial Times looked at the horror story that wasthe attempt by Neil Woodford, the U.K.'s most famous fund manager, to break away from Invesco Perpetual and set up his own firm. The other is by my Bloomberg colleagueSabrina Willmer on the culture of Fisher Investments. Its head, Ken Fisher, is in hot water for some sexist comments in a speech earlier this month, and investors are pulling their money. Both are great reads — and not just for those who work in fund management. They are different cases. Woodford has crashed irreparably, while Fisher is going through a public relations bad patch. But one common element is toxic white masculinity. Woodford might have averted disaster, and Fisher might have avoided difficulties, with a more heterogeneous culture. And that lesson is universal. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment