Helicopters, Two Sheds and a Shot of Adrenaline What started a month ago with the helicopters from "Apocalypse Now" ended on Thursday with the Arthur "Two Sheds" Jackson sketch from Monty Python. In between, we managed to have a long chat about The Case for the People's Quantitative Easing by Frances Coppola, a succinct and polemical defense of what is best-known as "helicopter money" — dropping cash from the sky, or more prosaically getting central banks to print money and by some mechanism send it directly to the people. For those of you who were unable to follow our 90-minute live chat about the book on the Bloomberg terminal, in which Coppola talked to me and Bloomberg Opinion's Clive Crook, the full transcript is on the web here. It was a fascinating discussion that I thoroughly recommend reading in full. If you would prefer a briefer version, what follows, continuing the cinematic analogy, is a "Director's Cut." The single greatest insight, in my opinion, is that the problems with printing money have little to do with economics, and everything to do with politics and institutions. Used sparingly, there's surprisingly little economic reason why the government shouldn't conjure money out of thin air from time to time. The problem is working out how to give anyone the power to do this without setting a precedent that will lead people to demand more money from nothing, and politicians to keep bringing out the helicopters every time they have a new project. That's where "Two Sheds" comes in. In the sketch, the interviewee is a composer who is proud of his new symphony but every question is about his strange nickname. Similarly, almost all the questions that Coppola faced boiled down to concerns about political institutions. The first critical point in her response was that People's QE should never be viewed as a vehicle for combating inequality. It shouldn't therefore be confused with the "universal basic income" idea that U.S. presidential candidate Andrew Yang is floating with some success on the campaign trail. Coppola also batted down suggestions that money should be aimed specifically at the elderly or at families with children, on the basis that they are likely to spend it. Her objection is that any such targeting would create the impression of an entitlement, and make it far harder to stop. It would also risk politicization, and by being more narrowly focused it would have less chance of performing its critical task of raising aggregate demand. All questions of distribution should be left to fiscal policy. So, central banks dropping money are not in some Robin Hood-like exercise in robbing from the rich and giving to the poor (even if QE so far has had the opposite effect). Rather, the best cinematic analogy involves what John Travolta did to Uma Thurman in a famous scene from "Pulp Fiction." It should be regarded as a shot of adrenaline to be administered only when the patient is comatose or near death. Or, in Coppola's words, "one-off responses to negative economic shocks which cause a large fall in aggregate demand." It is only for use when the risk is deflation. How do we make sure it stays that way? First, Coppola suggests that fiscal and monetary authorities need to coordinate more closely. This is ever a vexed issue. Second, central banks make the decisions and must remain independent, with the backing of responsible politicians. Legitimate, effective and respected governments turn out to be a necessary condition for helicopter drops to be workable. This suggests, I fear, the greatest problem with this concept: With levels of public trust in democratic institutions alarmingly low across the western world, it becomes much more dangerous to permit the possibility of helicopter money, because it's harder to resist the pressures toward ever more drops. Why exactly do we need to resort to helicopter money? I don't think we spent enough time on this, but Coppola's main point, with which I cautiously agree, is that other alternatives have been exhausted. Negative interest rates are beginning to warp incentives in dangerous ways. Take rates much further into negative territory and the entire security of the banking system comes into question. And as for the subject that I thought might dominate, there were surprisingly few questions attacking the admissibility of the entire concept, or warning of Zimbabwe or Weimar Republic-style hyperinflations (which Coppola argued, I think correctly, were due to seriously weak political institutions). It does make sense for central banks to retain helicopter money as an option; but only if they save it for true emergencies. As she put it: "It doesn't make a great deal of sense to deny them use of a money-creating tool, when creating money is their job." All further feedback continues to be welcome. Please send to the book club's email address: authersnotes@bloomberg.net. And Now, on to Antitrust With helicopter money done, we will now move on to antitrust enforcement, or rather the lack of it. The contention of Jonathan Tepper in The Myth of Capitalism is that a failure to maintain competition policy has allowed industries to become too concentrated and uncompetitive, and with that has come the curdling of the benefits of capitalism. It's a very well written polemic. For a first taste, try reading the op ed he wrote forBloomberg Opinion last year, or listen to the podcast he recorded with Arthur Levitt. There will be far more on this subject over the coming month; please get reading.

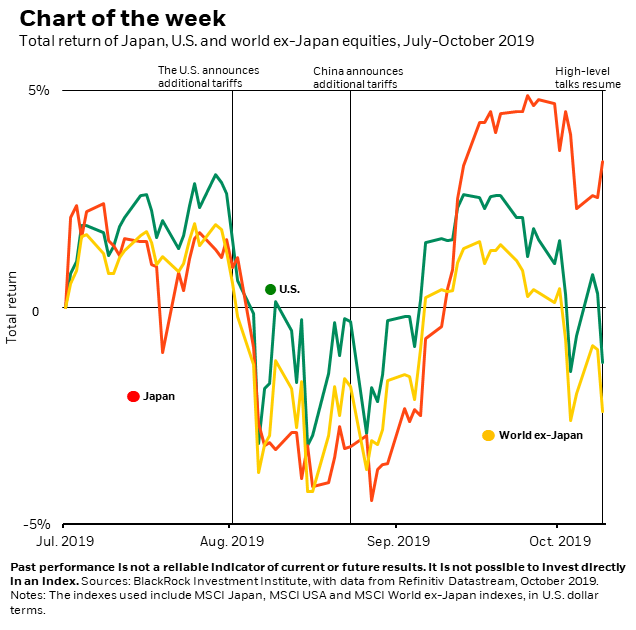

And Back to Japan Following yesterday's piece on the bullish case for Japan (if executives can ever be persuaded to disgorge their cash), I saw this interesting chart from BlackRock Inc. This amplifies the potential bullish case for Japanese equities, which is that they are a cheap and leveraged way to buy exposure to China. The problem is that you have to bet on both a positive resolution to the U.S.-Chinese trade talks, and a change in behavior by corporate Japan. But the possibilities are plain.  Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment