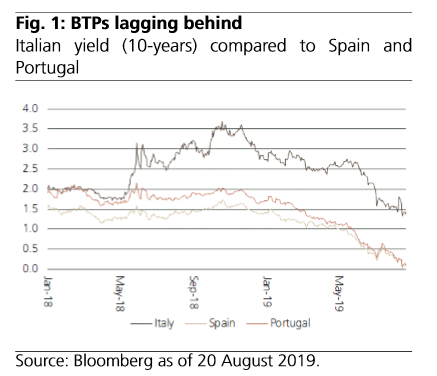

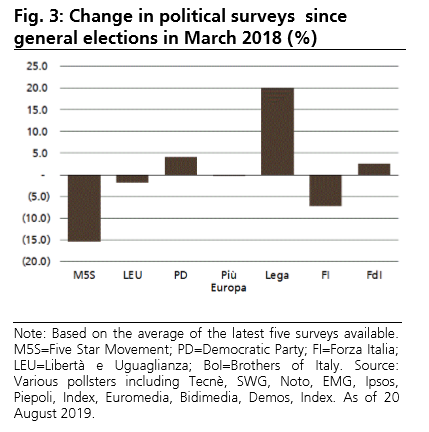

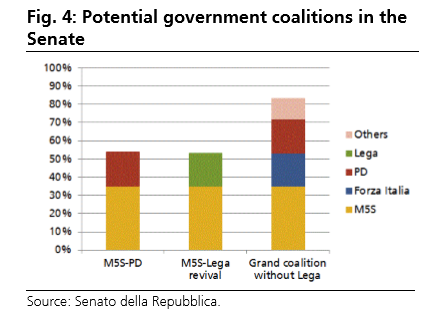

The Italian Job Geopolitical developments continue to churn global markets, but one shocking development is having remarkably little impact: Italy's political crisis is passing almost unremarked. It is easy to say that governments in Italy practically fall at the rate of one a year, which isn't wide of the mark. But it misses the point that the current coalition was a very new development, and that the future is now clouded with radical uncertainty. It is standard to take the yield spread of Italian bonds (BTPs) over German bunds as an indicator of perceived political risk. The wider the spread, the higher the political risk of Italy. The formation of the coalition between the left-populist Five Star Movement and the right-populist Leauge was greeted with horror last summer. The decision by the League this month to end the coalition, and the resignation of the prime minister Tuesday, barely show up on the chart:  Another way of assessing this is to compare BTP yields with equivalent bonds from the Iberian peninsula. While both Spain and Portugal appeared to be in much deeper crisis than Italy, yields on Italian bonds surged higher with the formation of the coalition; now, they are moving in alignment with their Spanish and Portuguese counterparts. The yield gap hasn't closed, but it hasn't widened either:  This is hard to explain. The current Machiavellian maneuvers are deeply distasteful, as Ferdinando Giugliano explains in this column, but they are driven by the hugely successful rise in the power and popularity of the League. The League's agenda can be called many things, and market-unfriendly is certainly one of them. Since the coalition was formed, Matteo Salvini, the League's leader, has done a great job of building power at the expense of his coalition partner, and of others in the Italian political orbit. Whatever else he may be, this chart, produced by UBS, makes clear that he is a very skillful politician:  With the prime minister Giuseppe Conte (who belonged to neither Five Star nor the League) announcing his resignation, the likelihood is that the president will call an election, in which the League would almost certainly, on current trends, emerge as the biggest party. It is just conceivable that they could win an outright majority. If they weren't in government as the leading party, any alternative ruling coalition would be fatally weakened as sniping from Salvini in opposition would doom their prospects. So hope of avoiding a very messy situation rests on putting together a new coalition without them. This didn't happen last year after the election, and most of the versions given here by UBS look implausible:  (The PD is a center-left group and Forza Italia was the populist political vehicle set up a quarter of a century ago by former president Silvio Berlusconi).

In 2017, the prospect of Marine Le Pen, a very similar politician to Salvini, gaining the French presidency was enough to frighten markets to the core. Salvini's chances of taking power now look much higher than Le Pen's did then. The only alternative appears to be a dreadful mess. Markets may be overreacting to other political events around the globe, but they are underreacting to this one. From Frankfurt With Love Which way will bonds turn next? The latest drop in yields shows that the global situation remains febrile, but I think it is fair to say that much of it turns on the U.S. relationship with Germany (to a greater extent even than China). The following chart shows the spread of U.S. 10-year inflation expectations, derived from the bond market, over the same number for Germany:  The sudden tightening of this spread in the last few weeks is extraordinary and more or less impossible to explain in terms of economic data. No obvious new reasons to expect a sharp fall in future inflation in the U.S. have emerged recently (and the latest round of tariff threats gives a reason to expect inflation to rise). And there is no obvious reason to expect German inflation expectations to rise. The best explanation is that this is driven more by a switch between the markets in search of yield.

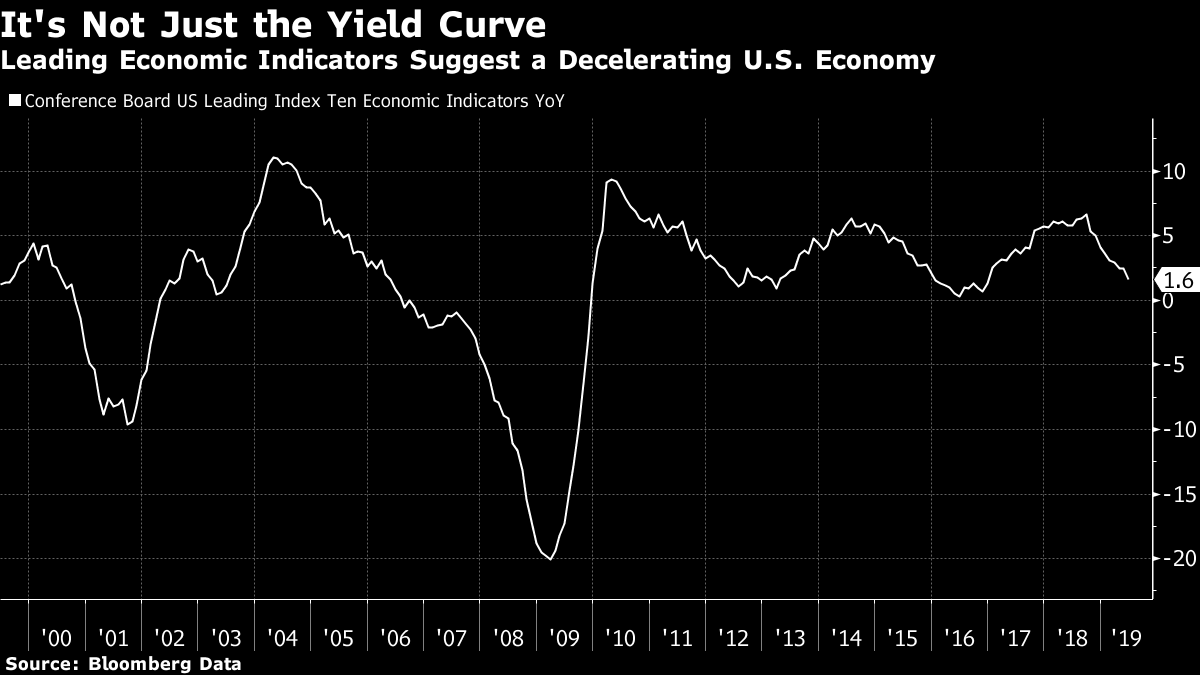

If that can be taken as a reason to disbelieve that the inverted yield curve and its prediction of a recession (and note that the 3-month Treasury yield remains above the 10-year Treasury yield, so inversion remains in place), there are unfortunately other reasons for concern. The yield curve over history has been the best recession indicator we have, but other indicators are also suggesting economic weakening, if not an outright recession. This is the latest readout from the Conference Board's 10 leading economic indicators, and it shows a sharp deceleration in growth over the last few months. This indicator has twice been slightly weaker in the post-crisis decade without an ensuing recession, but the hard economic data are plainly giving reason for some concern:  There is a similar picture from the now widely followed "Nowcast" produced by the Federal Reserve Bank of Atlanta and intended to map the growth of the economy in real time. That growth, according to the Atlanta Fed's model, is now just over 2%. We aren't in recession yet, but neither are we enjoying the kind of levels of economic growth that allow for any complacency:  There is continued political invective against anyone who criticizes the economy. Words on this subject should always be chosen with care, and it would certainly be alarmist to say that a recession is unavoidable. It is also fair to say that the alarming yield-curve indicator does seem to owe something to very strange global market conditions. But in the final analysis, if you are confident either that a recession is imminent or that it isn't, you are probably over-confident. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment