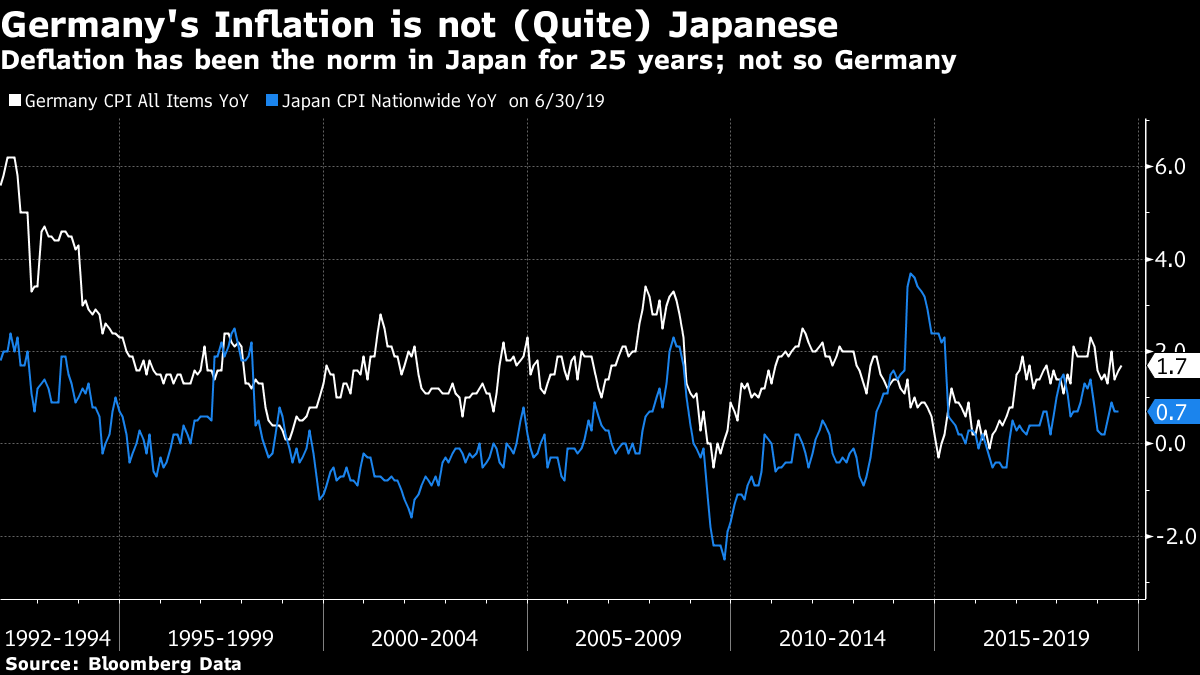

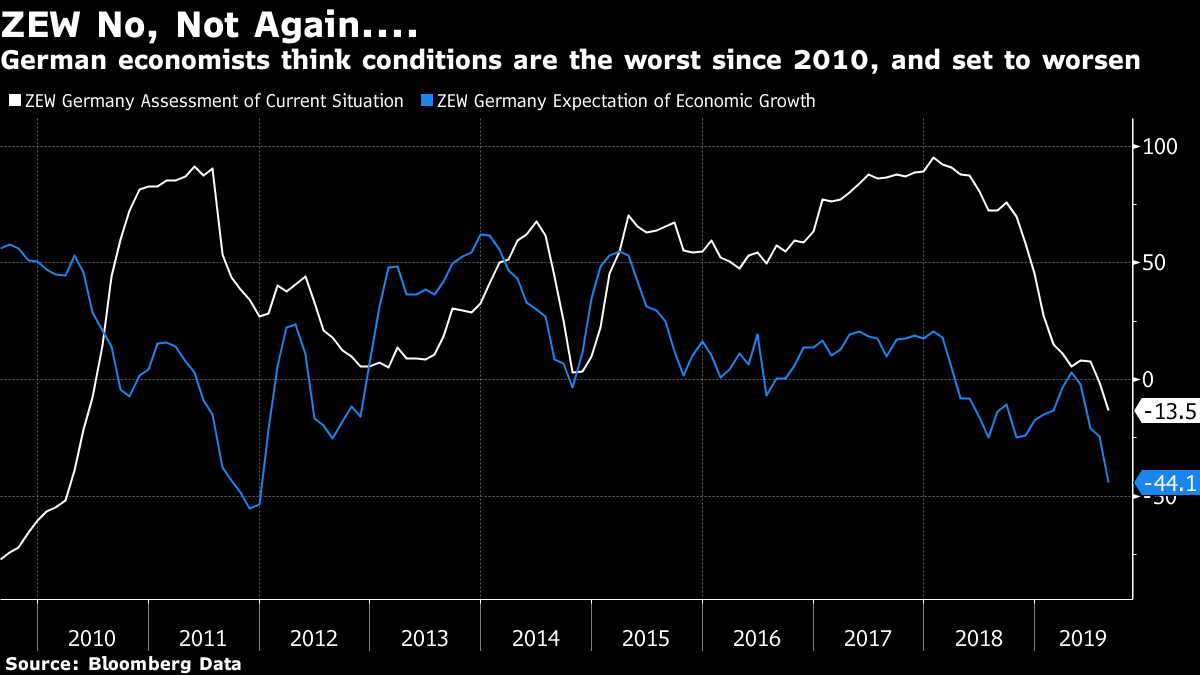

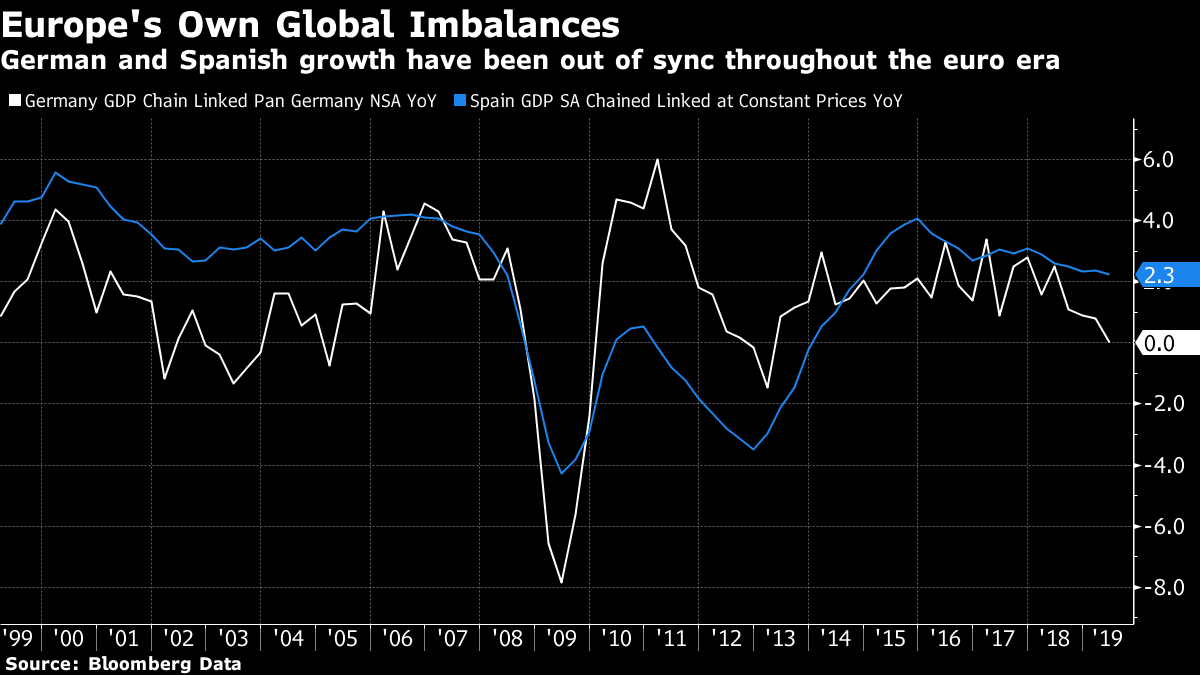

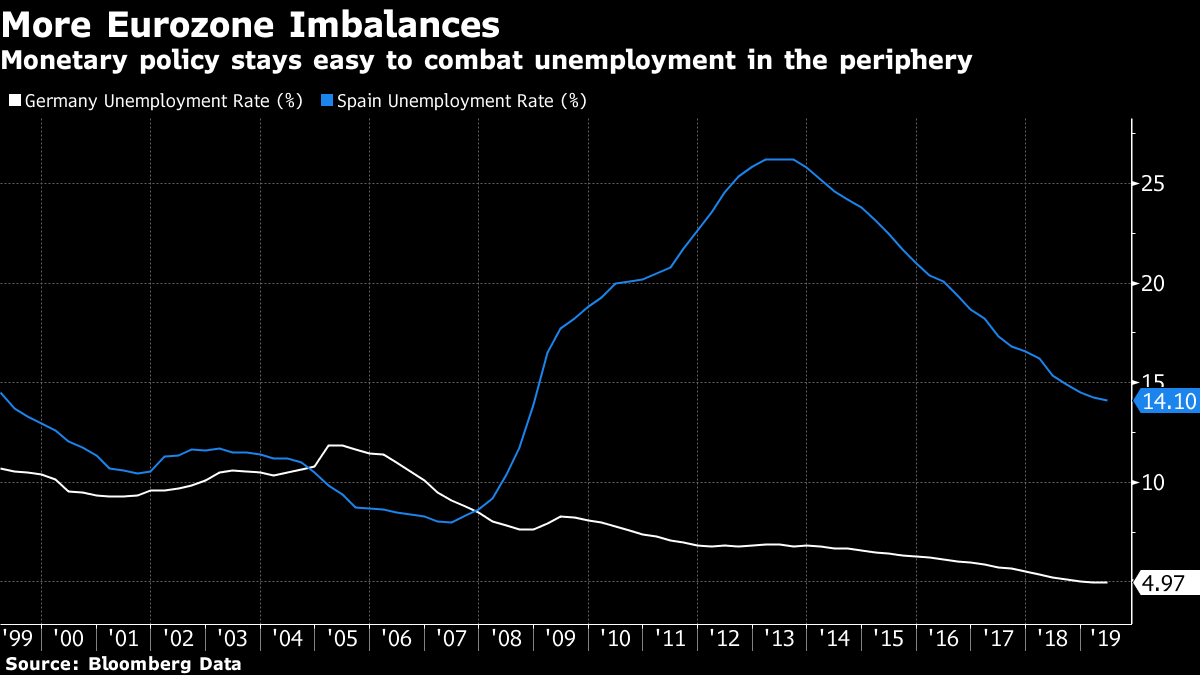

Deutschland, Deutschland, unter alles. Germany has a dreadful case of the Vapors. For those who were not brought up in the 1980s Britain, what I mean is that, to quote the immortal words of the great one-hit wonders The Vapors, Germany is turning Japanese. Its problem is now so extreme that before long Japan might have to start worrying about turning German. Japan has been in the grips of dreadful deflationary slump that started to set in once its great equity and property bubble burst at the beginning of the 1990s. This has pulled yields on Japanese government bonds – JGBs - ever lower, and no amount of attempts by successive governments and successive governors of the Bank of Japan have been able to snap the country out of this downward spiral in yields. Indeed, it was the BOJ that gave the world the concept of quantitative easing , or QE, buy purchasing bonds in a bid to push down yields even further and flood the financial system with cash in an effort to jolt the economy. Germany has been in danger of Japanification for a while, but until recently an escape seemed likely. Market volatility was historically low in 2017, and the talk was of a "synchronized global recovery" as German data proved to be startling strong. Disappointment set in during 2018, however, and the savage move in the bond market the last few months has pushed yields on German bunds not only significantly below JGBs for the first time, but significantly lower than JGB yields have ever been:  Germany's pain has been central to bond market convulsions around the world. Very disappointing data on German economic growth has acted as the most direct catalyst for the buying of long-dated U.S. Treasuries that briefly caused an inversion of the U.S. yield curve, with the 10-year yields falling below two-year yields for the first time in 12 years. While the inversion lasted only a matter of minutes, the spread between the 3-month bill rates and 10-year yields continues to be inverted, as it has been for several weeks. And virtually unnoticed amid the excitement, the 3-month/10-year curve in Germany also inverted:  An inverted yield curve has over time been a good indicator of an oncoming recession. But it is worth looking at what exactly is ailing Germany and whether it really is similar to Japan. Both are large exporting nations that enjoyed quasi-miraculous growth after the second world war, and now have challenging demographics with an aging population. But while outright deflation (an actual sustained drop in consumer prices over time) has become a fact of life in Japan, German inflation has remained above zero with only a very brief exceptions. When last seen, German consumer price inflation was 1.7%, within striking distance of the European Cenral Bank's 2% target:  So the market sees Japanification coming, but Japanification is not yet an established fact in Germany. For a sign of how bad sentiment has become in Germany, take a look at the widely followed ZEW survey of economists and analysts. The latest reading, which came out as last week's bond market turmoil was getting started. showed sentiment toward Germany's current economy is worse than at any time since the tail end of the Great Recession. The period since then has included the euro zone's sovereign debt crisis, two economic downturns and the shock provided by the U.K.'s Brexit referendum. Meanwhile, expectations for the future are dropping sharply, and are the lowest since the worst of the sovereign debt crisis in 2011:  Germany's travails have impact far beyond the country itself given that it is part of the euro zone, and its economy is out of sync with those of countries on the euro zone's periphery. Before the global financial crisis, Spain was growing healthily and might have benefited from higher interest rates; Germany was growing more weakly. As one monetary policy had to fit all, Spain benefited from low rates aimed at Germany, and enjoyed an epic construction boom that would inflict a severe and enduring recession once the bubble burst:  Even more dramatically, this is what has happened to Spanish and German unemployment rates since the adoption of the euro in 1999. Setting one monetary policy that will work for both these very different economies is impossible:  A further problem for Germany, which can become a vicious circle, is its banking system. Europe's banks were far more bloated and over-leveraged than their U.S. counterparts when the crisis hit. This has left them with a legacy of de-leveraging that has hurt their ability to lend. Banks remains far more central to financing businesses and people in Europe than they are in the U.S., so this matters greatly. Europe's banks remain troubled, with the agonies of Deutsche Bank probably the most serious symptom. Weak banks imply a weak economy. That means investors will have less trust in the strength of banks' balance sheets, so they will bid down the share price to trade at a lower multiple to the official book value of assets. That makes it harder for banks to raise equity financing. And as weak banks also diminish confidence in an economy, this causes the yield curve to flatten, and a flatter or inverted yield curve makes it harder for banks to generate profits. And so this year has seen a simultaneous flattening of the yield curve and decline in the book valuations of banks. The net effect is to make it harder for Europe or Germany to escape Japanification:  In one crucial respect, the American response to the Global Financial Crisis worked better than that of Europe. U.S. banks could be re-capitalized, and to the surprise of many that actually happened. In Europe, re-capitalization was harder, and the sovereign debt crisis brought on by the imbalances in the euro zone made it even harder. As a result, the European banking system has Japanified since the crisis while the U.S. banking system has not. It is hard to see how Europe's economy can stage a strong recovery without a revival in confidence in the banks.  Europe's big banks are proving to be more central to the world economy than many had grasped. There is a growing recognition that they contributed greatly to the Great Financial Crisis. For example, Unfinished Business by International Monetary Fund official Tamim Bayoumi argued in 2017 that the whole crisis should be known as the "North Atlantic Financial Crisis," with European banks' willingness to finance excesses in the property markets of the U.S. and many regions of Europe an essential element in the disaster that developed. The creeping realization of both the importance and the weakness of the European banking system – which begins to look very much like Japan's banking system – is reflected in the relative valuation of European and U.S. banks. Immediately after the crisis, European banks commanded a slight premium, in terms of price-to-book multiples. That has steadily turned into a crushing discount. The gap has narrowed slightly in the last year, despite the market excitement, but still has far to go:  Europe's Japanification affects everyone. The level of bond yields, rather than the curve, matters most. Bunds now yield far less than Treasuries, creating an incentive to move money out of Europe's largest economy and across the Atlantic to the U.S. There is a long way to go before bunds and Treasuries return to anything like their typical historical alignment:  So Germany's low yields put upward pressure on the dollar, reducing American competitiveness along the way, while adding to downward pressure on bond yields. The crisis of confidence in the Europe's economic powerhouse gave birth to last week's crisis of confidence as seen in the U.S. bond market's inverted yield curve. What can be done to reverse this? The pressure on the ECB to resort to yet more bond purchases is evident. That might at least spark faster inflation but it would also push down on European yields while adding to the upward pressure on the dollar. That leaves fiscal policy. Germany has persistent budget and trade surpluses, and inflation is little concern at present. If ever there were a time to resort to fiscal stimulus, this is it. More German spending might ease the difficulties of keeping the countries of the euro zone together. And the market is making it easy for Germany to do. Lower bond yields effectively encourage governments to spend by making it cheaper to borrow, and greater issuance of debt increases supply that will tend to pressure yields higher. So the market is almost directly pushing Germany to an outcome that many in the rest of the world would welcome. The problem is that Germany is maddeningly averse to fiscal stimulus, as Bloomberg News noted this week. Rules have been written into law to limit discretion to expand fiscal policy, other than when a downturn is already under way. German officials are now talking about new fiscal policy in the event of a recession. But that begs the questions of whether this would be anything more than the extra spending in welfare payments that governments naturally take on during a recession, and whether the spending could come before any recession, which is when it would be most helpful. The country is also caught in a web of what George Soros would call reflexivity, or the tendency of moves in markets to affect reality and to become self-fulfilling prophecies. When sentiment is this weak, negative yields, flat yield curves and distrusted banks combine to make it almost impossible for the economy to turn around. The negative sentiment that leads to these market phenomena may well be overblown and overdone, but for the time being it is turning Germany Japanese. And that, in turn, becomes an issue for the rest of the world. Fear itself. Reflexivity is in the air, although it generally goes under the one-word label "fear." My Bloomberg Opinion colleague Mohamed El-Erian commented last week that "we may end up in a situation where people read these alarmist headlines, they get concerned, they stop spending." Bank of America Corp. CEO Bryan Moynihan told Bloomberg News Friday that: "We have nothing to fear about a recession right now except for the fear of recession." And President Donald Trump tweeted that "The Fake News Media is doing everything they can to crash the economy because they think that will be bad for me and my re-election." There is an element of truth here. Negativity in the news that people read (including the tweets they read), can affect their behavior, which in turn affects the economy. Banishing fear is a first step to recovery, as famously enunciated by Franklin D. Roosevelt in his inaugural address: So, first of all, let me assert my firm belief that the only thing we have to fear is fear itself—nameless, unreasoning, unjustified terror which paralyzes needed efforts to convert retreat into advance. FDR saw fear as his enemy. By contrast, the current occupant of the White House made an inaugural address remembered for stoking alarm by inveighing against "American carnage." And Trump has made clear that he sees fear as a vital tool and weapon for the powerful. In an interview with the journalist Bob Woodward during the campaign in 2016, he commented: Real power is through respect. Real power is – I don't even want to use the word – fear. That then became the title for Woodward's book on the early days of the Trump presidency:  Frightening people and keeping them off-balance by staying unpredictable is indeed a great strategy for retaining power. As the Trump presidency continues, we can see that strategy playing out. He deliberately tries to frighten people. Headlines accurately reflecting his views will justifiably be alarming, and possibly even "alarmist." But that reveals the problem with exercising power through fear. Fear has its own effects on the confidence of businesses and consumers, and on markets that can set the rules of the game in a way which the president cannot counteract. When looking at the U.S. economy specifically, it is hard to see that it is moving in quite the negative direction that markets, the news media, or surveys of consumers and businesses suggest. Each of these groups tends to magnify the message of the others. So to this extent, there is justice in complaining that negative reporting on the economy and the markets is damaging the economy. But there is a circularity here. An accurate report on a sentiment survey or on the market will be very negative at present. People need to be informed accurately, but on seeing such reports they are likely to become even more negative and thereby require another round of negative headlines. What was the trigger that started this round of negativity? The formal media (now charmingly known as the "mainstream media" or even the "fake news media") has little choice but to respond to presidential broadsides on Twitter, or to report factually on moves in markets and what they imply. Social media enhances groupthink, which can be led by opinion leaders, such as the president of the U.S. But the current round of market turmoil can be dated very easily to the presidential tweet imposing a new round on tariffs on China that appeared on Aug. 1. That tweet was presumably meant to frighten China. It also frightened markets, and started a cycle of negative reflexivity. Those who can inspire fear are usually very powerful. But frightening the markets is dangerous. This month has shown the limit of the strategy of ruling through fear. Does the president have another strategy to replace it? My apologies if this question seems alarmist, but it needs to be answered.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment