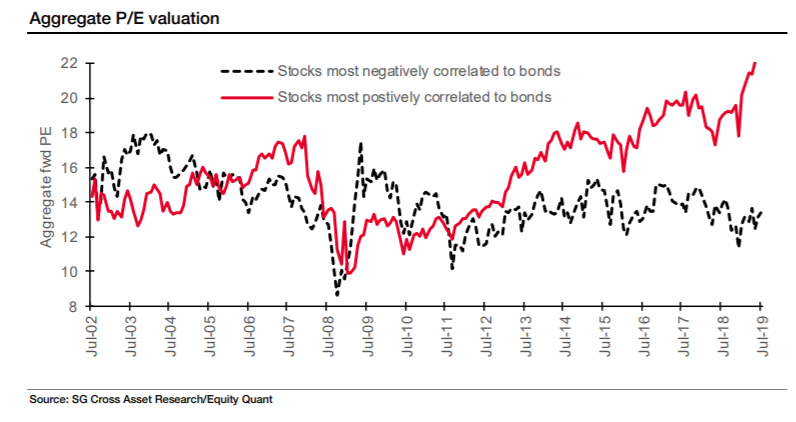

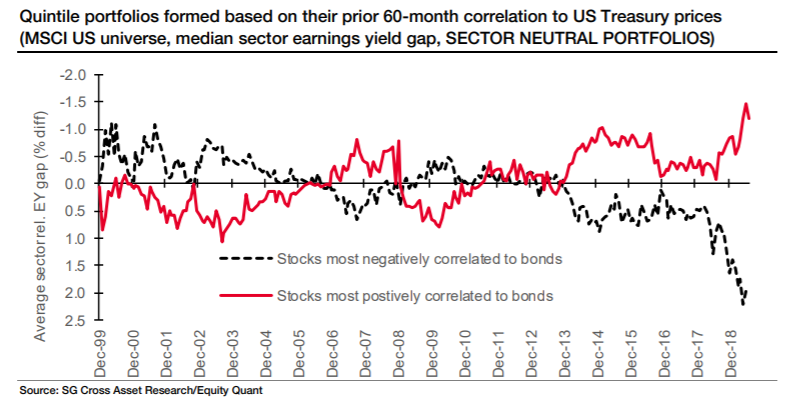

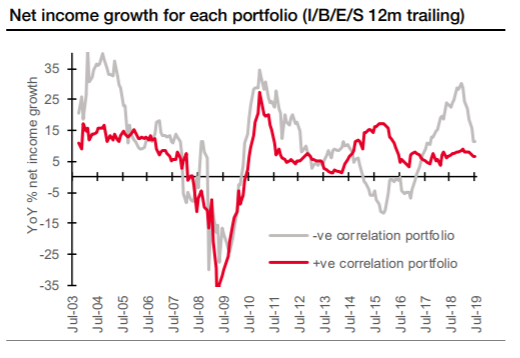

After the curve has gone. Chaotic conditions continue in the bond market, and yields keep falling. The yield curve, defined as the difference between two- and 10-year Treasury note rates, is no longer inverted, but that doesn't seem to matter at present. The surge of investors into bonds is a fact of life for now, and it's roiling virtually all other markets. What to do about it? A day after the "Great Inversion," there's no shortage of advice from the professional investment community. First, it's best not to treat the inversion as a timing indicator marking the start of an immediate move out of bonds. Recessions and equity bear markets tend to start several months after the yield curve first inverts. If you have a horizon of five or more years, however, it becomes more useful. To quote Pictet Asset Management chief strategist Luca Paolini: The yield curve is a great tool for strategic (1-5 years), but not tactical allocation (3-6 months). In the past, the S&P index has rallied on average about 30% from inversion date to market peak, as UBS has pointed out. This is because equity markets typically experience a "last hurrah" before the start of a recession. Capital Economics global economist Simon MacAdam made the same point: At their best, yield curves are blind in one eye — they can often see economic trouble ahead but struggle to gauge how far away it is. Rather than the inversion itself, the sharp steepening of a yield curve following an inversion has proved to give a better sense that a recession is just around the corner. Sensible admonitions against using the inverted yield curve as a trigger for a big move out of stocks make a lot of sense — providing they don't somehow slide into a belief that it's a good idea to plan to keep holding a large load of stocks. What about investing within the stock market? The problem here is that investors have long been aware that the bond market is behaving very unusually, and that has brought many of them galloping into "bond proxies" — relatively boring companies that pay a high and and consistent yield. These became especially appealing when bond yields are low, for obvious reasons. Real estate and utilities, which both enjoy relatively protected streams of income, have tended to do well when bonds are doing well. So, in general, do "quality" stocks, which have particularly sound balance sheets. The complicating factor is that so many investors know this and many safe, high-quality bond proxies are now in fact dangerous, low-quality stocks that are nothing at all like bonds. That was the message I took from a new research paper from Andrew Lapthorne, who heads quantitative equity strategy for Societe Generale. He divided stocks into quintiles according to how correlated their prices were with bond prices. Bond proxies will tend to be most strongly correlated. Over history, the most and least bond-like quintiles tended to have quite similar valuations. But now, after years of central bank quantitative easing and the hunt for yield, bond proxies are far more expensive:  There's more. This is largely a sectoral effect, which explains why real estate investment trusts have largely avoided trouble amid the turbulence. But when Lapthorne produced sector-neutral quintiles (so that the least bond-like real estate company would appear in the lowest quintile and the most bond-like biotech group would appear in the highest quintile, and so on), he discovered that the more bond-like companies were outstripping their industry rivals to a quite absurd — his word is "bonkers" — extent:  So bonds are expensive, but so are bond substitutes. If there is any money to be made within the stock market, it's probably in finding the anti-bond stocks that have sold off too much. Meanwhile, the bond substitutes look as though they would be vulnerable to a reversal or sell-off in the bond market. And that's a problem, because Lapthorne also found that the bond substitutes tend not to be very safe, at least as we normally understand them to be. A fifth only went public within the last 10 years, so there is no history to gauge how they perform in a recession. Looking at profit growth for the companies that did have a long enough history revealed that the bond substitutes had indeed managed to keep increasing their earnings throughout the post-crisis period, which is impressive. But they had suffered declines during the recession, showing that they were not recession-proof. Though bond-like, they are not bonds.  So when piling into bond substitutes, exercise caution. They are no longer as safe as they appear. Beyond looking for bond correlations, the sectors that have performed best in the 12 months following past yield curve inversions are energy (an interesting contrarian bet at present given the troubles of the oil market) and technology, according to more number-crunching by the quantitative strategists at Bank of America Merrill Lynch. (In this case, it behooves investors to know that the tech sector has changed much over time.) The worst underperformers tend to be consumer discretionary stocks. An inversion heralds the onset of a recession, and investors spend the next 12 months reacting to the worsening prospects for companies most exposed to consumers. Beyond adopting extreme caution, then, there's not a lot that investors can do to profit from the current extremes in the bond market. Stay vigilant. A contrarian winner. If there was any good news Thursday, it came from Walmart Inc. The world's biggest bricks-and-mortar retailer announced surprisingly strong earnings and was awarded with a big pop in its share price. It came as a welcome change after some very poor data from large department-store chains. There is a sense, however, that this is actually bad news. Since its period of secular growth ended about 20 years ago, Walmart has become the perfect contrarian indicator for the rest of the U.S. stock market. When times are good, it does relatively badly. When they are bad, it does relatively well. It was the only stock of any size to be higher on the day the market bottomed in March 2009 than it had been at the top in October 2007. Indeed, over the last 20 years, we can see that Walmart tends to start outperforming the market as a whole just as the market begins to decline:  There's intuition to back this up. At the economic level, Walmart's business model of convenient and cheap shopping grows all the more competitive when times are tough. Shoppers may return to them and give them more business. And at the market level, if investors begin to find a huge and efficient retailer to be an exciting investment, that's a sign of dwindling animal spirits when applied to the rest of the market. So good news for Walmart may not be the best of news for the rest of us.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment