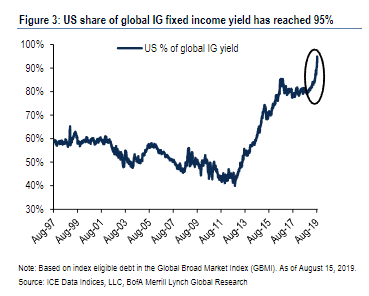

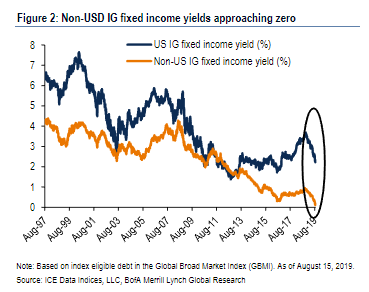

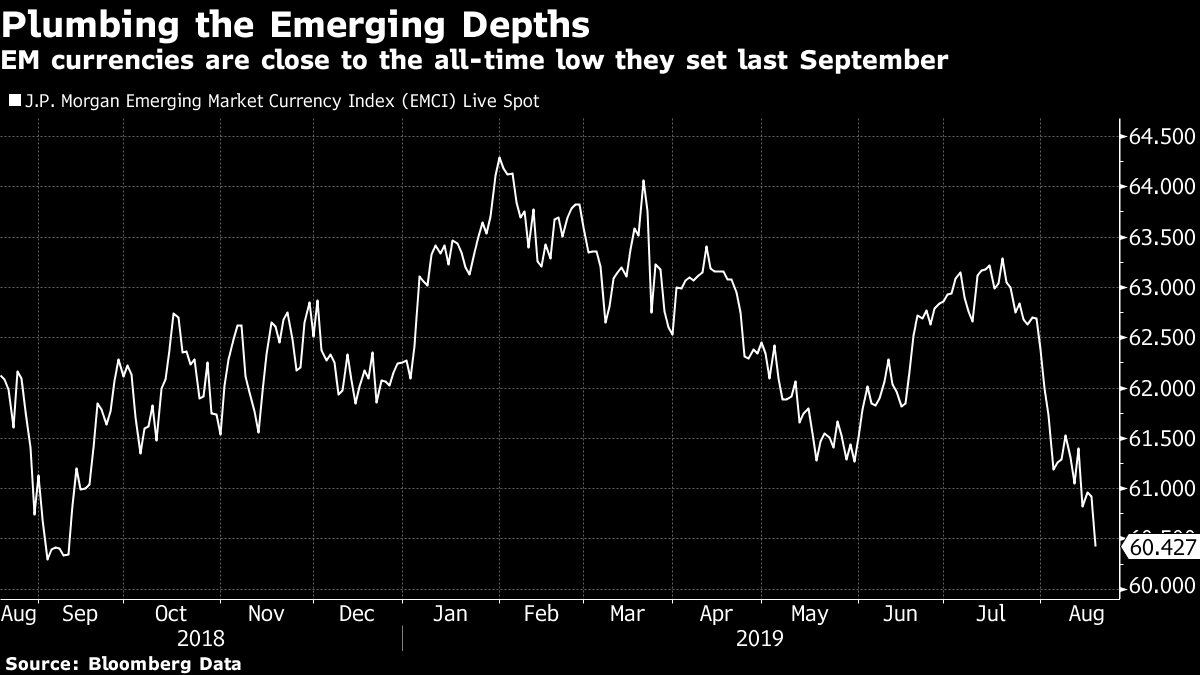

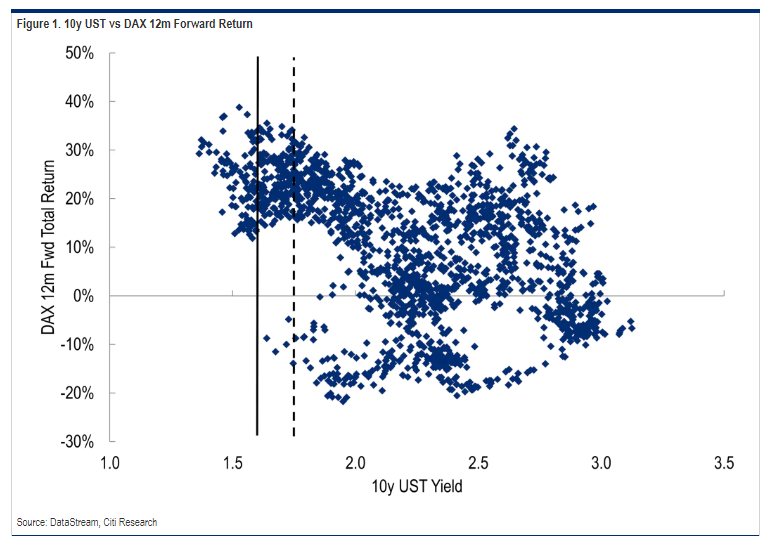

Are we there yet? The latest developments, for those who are getting behind or may have been on vacation, are that both Germany and the U.S. are talking about issuing more debt in the face of historically low yields. In response, stock prices rose and bond prices fell on Monday. That suggests a more delicately poised market situation than many might assume. This is how stocks have performed compared to long term U.S. Treasury bonds (represented by the most popular exchange traded funds) since the day before Lehman Brothers' bankruptcy transformed the global financial system:  Stocks remain very weak relative to bonds, holding at levels from which they have at previous points in the post-crisis equity bull market enjoyed a strong recovery. If they don't snap back quickly, then it might start to look like the beginning of a major secular move, with stocks falling. Repeating this exercise for gold, widely regarded as a haven and a hedge against potential government profligacy, such as issuing excessive debt or printing money via quantitative easing, we see a similar picture:  Viewed in terms of gold, stocks did not hit bottom until the U.S. debt ceiling crisis of 2011. Once it became clear that low yields were not sparking faster inflation and that the U.S. was not going to default, stocks enjoyed a great rally. But but at present they are no higher on this measure than they were in 2015. There has been no net growth on this score since the eve of the Chinese devaluation four years ago. As with the bonds chart, stocks appear to be poised for a turning point. But if they are not, then we could be at a tipping point, such as in 2011, when we see a big secular move out of stocks as investors accept that the bond market has been right in its concerns about the economy. There is good intuition for either outcome. Low yields are encouraging more debt issuance , which should drive up yields – all else being equal. And the bond market is picking up on unmistakably poor global economic growth, which will in time drag down share prices – all else being equal. What will determine which way we go? In the short term, I suspect the dollar could be the balancing mechanism. As this extraordinary chart from the credit strategists at Bank of America Merrill Lynch show, some 95% of all investment-grade corporate debt in the world that has a positive yield is in the U.S. Thus, the pressure on European fixed income managers trying to generate a return or guarantee that they can match liabilities will be to buy U.S. bonds – which will put upwards pressure on the dollar:  To put that another way, the average investment-grade corporate bond outside the U.S. now carries a negative yield. That makes the sanctuary of the U.S., where yields of more than 2% are still the norm, look much more appealing:  The dollar, which strengthened on Monday as U.S. stocks enjoyed a good day, will be where the stresses meet, I suspect. This is JPMorgan's index of emerging market currencies, which hit a low last September amid bad news from Argentina and Turkey, and speculation that the Federal Reserve was locked into a long-term rate-hiking cycle:  Even the drastic reversal the Fed has not been enough to stop emerging currencies from plumbing the depths once again. Emerging economies are not as exposed to the dollar as they used to be, because many have made steps to increase the amount of borrowing they do in local currency, but a further run on emerging currencies will still increase the risk of an emerging-market crises. With uncertainty over trade having been amped up to such a high level, this is the last thing anyone needs. Meanwhile, the Trump administration wants a weaker dollar to aid U.S. competitiveness. Despite the Fed's volte-face, that is not what it is getting. It is possible to overstate this, but the dollar is nearing a possible breakthrough to levels that make it less competitive than anytime in the past 15 years. This is Citigroup's real effective exchange rate (taking into account different rates of inflation) for the dollar against a broad range of currencies over 30 years. On this measure of competitiveness, which is as good as any, the dollar is now at levels that were unremarkable in the 1990s, but render U.S. exporters less competitive than they have been for most of the time for more than a decade:  The options ahead of us look binary. Jonathan Stubbs, Citigroup's veteran European equity strategist, synthesized it simply enough. Either you should buy stocks because the market will force the authorities into equity-friendly stimulus or it's different this time. And the impact is global. As he shows here, the subsequent one-year return for the German DAX index whenever Treasury yields get this low tends to be very strong:  But it may not be quite as binary as this. A splurge of debt issuance and government stimulus might yet set off a chain of selling in the bond market. As bonds are unprecedentedly expensive and satisfy all the normal conditions for an investment bubble, the fall-out could be severe. Less than a year ago, equity investors were alarmed by rising bond yields, not falling yields. Another way to look at it comes from Peter Atwater of Financial Insyghts. He points out that the plethora of headlines about recession risks, the desperate attempts by Trump and his advisers to shoot the messengers by blaming markets, journalists and Democrats for talking down the economy, and even cartoons in the New Yorker all suggest that a peak in sentiment is at hand. I will quote him at length because he captures the binary fork in the road ahead of us very well: Taken all together, the set up for a major "risk-on" rally looks really good here. Everyone – investors, policymakers and the media – believes that a major global recession is coming and is acting like it. Heck, even the Wall Street Journal editoral page is peeved with the White House!

Could bad go to worse? Absolutely! In fact, folks like Robert Shiller would argue that all the talk of a recession will inevitably cause the recession to occur, whether we want it to or not. While that may be the case, I don't think the markets will agree with that until substantial pain is inflicted first on those who bought bonds and sold stocks this August. Some kind of sentiment reversal is due. Should that now play out, new all-time nominal highs in the major U.S. indices would not be at all surprising. One place to watch for a potential bullish sentiment catalyst is the White House. With the 2020 Presidential Election looming large and the President's polling figures languishing, it would not be at all surprising to see some kind of major stimulus package attempted (likely accompanied by a dialing back in anti-China/tariff rhetoric.) Again, policymakers follow mood – especially in an election year. Finally, should we see a renewed sell-off in stocks, it would suggest that rather than hitting a turning point here, we have hit an important tipping point with the equity market playing catch up to the bond market in a hurry. I don't see that as a likely scenario, but it could happen. For all the recessionary rhetoric, the major U.S. indices still haven't budged from their all-time highs. I agree, but I do think it's important to add that the bond market, to a much greater extent than the stock market, looks over-extended. A reversal for bonds would not be great for stocks. If it turned into a rout, things could get very messy indeed, even with central banks and governments stepping up to the plate as the markets wish. Shareholder values. In what could be a great moment in the history of corporate governance, the U.S. Business Roundtable has come out in favor of stakeholder value, rather than shareholder value. This sounds like esoterica, but it has profound implications for the way companies behave and how they set their goals. Its precise significance, however, is easy to mistake. "Shareholder value" is the notion that it is the job of a company's managers and directors to maximize value for their shareholders, who own the company. Other stakeholders, such as employees, customers and affected members of the community, are less important. In recent decades, many boards have worked on the assumption that it is their legal duty as fiduciaries to do this, and there are some legal rulings to support this, although the legal precedents are complex and murky. As a moral notion, the idea springs from Milton Friedman, who can be seen arguing with a student at Cornell University in a video here. He was a remarkably persuasive man. However, you can see from the video that he is not quite saying what many now think he is saying. His point is that companies should not concern themselves with giving to charity. Rather, they should make as much money for their shareholders as they can, and then those shareholders, who own the company, can decide whether to make charitable gifts. This is an argument often used against ESG, or "socially responsible," investing: why not just maximize your return on your investment and then be generous to charities, rather than attempt to pick out good moral companies? Oliver Hart, a more recent Nobel laureate, makes this point in this video. Friedman is not necessarily arguing that we should be OK with companies making and selling AK-47s; he is merely saying that that moral question lies with shareholders. But if the origins of the shareholder value notion have been misunderstood, they have certainly underpinned much of the philosophy toward corporate activism and governance in recent decades. Cost-cutting, spin-offs to maximize value and the involvement of private equity are all part of a panoply of measures to boost shareholder value but not, many critics allege, the overall value to the community or customers. The most famous critic of shareholder value as a philosophy was also based at Cornell - the law professor Lynn Stout. She made the point that the shareholder is often an amorphous concept, and that while companies can always write an obligation to maximize shareholder value into their statutes, in practice none of them do. She passed away from cancer last year, but this video lays out her philosophy beautifully. A debate between Friedman and Stout would have been something to behold. What is fascinating is that the Stout view of corporate governance is now totally in the ascendant. A group of 181 CEOs led by JPMorgan's Jamie Dimon have now put their names to a statement that: "While each of our individual companies serves its own corporate purpose, we share a fundamental commitment to all of our stakeholders. Americans deserve an economy that allows each person to succeed through hard work and creativity and to lead a life of meaning and dignity. - Delivering value to our customers. We will further the tradition of American companies leading the way in meeting or exceeding customer expectations.

- Investing in our employees. This starts with compensating them fairly and providing important benefits. It also includes supporting them through training and education that help develop new skills for a rapidly changing world. We foster diversity and inclusion, dignity and respect.

- Dealing fairly and ethically with our suppliers. We are dedicated to serving as good partners to the other companies, large and small, that help us to meet our missions.

- Supporting the communities in which we work. We respect the people in our communities and protect the environment by embracing sustainable practices across our businesses.

- Generating long-term value for shareholders, who provide the capital that allows companies to invest, grow and innovate. We are committed to transparency and effective engagement with shareholders.

Each of our stakeholders is essential. We commit to deliver value to all of them, for the future success of our companies, our communities and our country." This goes directly against the Business Roundtable's previous policy. And it makes sense. With inequality a deepening cause of social conflict, companies need to make clear that they at the very least take the interest of their workers and communities into account. And it is fascinating to see that some of the strongest defenders of companies against corporate activists are in agreement. Martin Lipton of Wachell Lipton Rosen & Katz, probably the most famous U.S. corporate governance lawyer and the inventor of the "poison pill" defense against takeover bids, issued a statement strongly endorsing the Roundtable's line. He denounced shareholder value as "mistaken policies promoted by economists and law professors who rely on financial statistics to justify the concept of shareholder primacy." He added: "From a legal standpoint, stakeholder corporate governance recognizes that the management and board of directors' primary fiduciary duty is to promote the long-term value of the corporation and is not primarily to the shareholders. To fulfill that duty, the board of directors uses its business judgment in deciding among the stakeholders — employees, customers, suppliers, the environment, communities and shareholders. If the directors are not conflicted and use due care in reconciling the competing interests of the stakeholders, they will have the protection of the business judgment rule and the courts will defer to their decisions without second-guessing them. As a long-time proponent of stakeholder corporate governance and a firm believer in capitalism and the market economy, I applaud the BRT's commitment to stakeholder corporate governance." Quite an edifice was built on shareholder value, but its demolition now appears complete. It is most important for all concerned to move ahead with building a better model for corporate governance that can inspire broader social trust. But it would also be good to look back and work out exactly how so many people convinced themselves that directors had a moral and legal obligation to look after shareholders only, and that this would be best for the economy. Friedman never argued for this, and companies were never under a legal obligation to behave this way. So why did they? |

Post a Comment