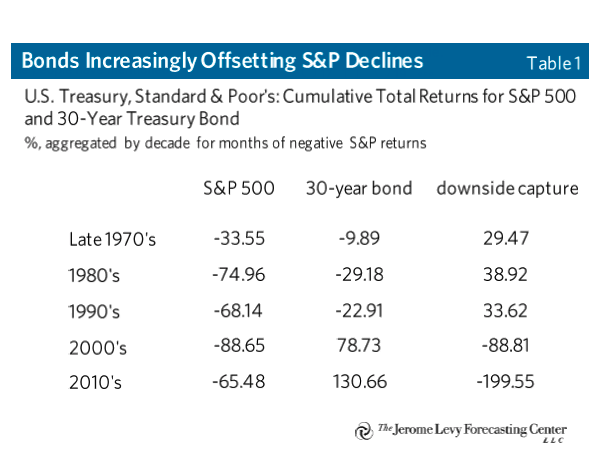

Fed in focus after choppy week, oil got caught up in some messy politics, and the economic data is actually pretty good. Fed watchAt the tail end of a wild week in markets, it's back to Fed watch. As debate rages over whether the fresh inversions of the yield curve signal recession, St. Louis Fed President James Bullard threw cold water on speculation the central bank would call an emergency gathering ahead of the Sept. 17-18 meeting. Chairman Jerome Powell may shed some light on how he sees things at Jackson Hole next week, potentially saying "I told you so" as solid data rolls in. Minutes of the July policy meeting Wednesday will also offer insight into last month's decision to cut rates for the first time since the crisis. Black and gold Oil is headed for its first weekly gain in three, but it certainly wasn't spared from the market's wild ride in recent days. The saga of an Iranian oil tanker caught in a spat between the U.S. and the U.K., trade war headlines, rising stockpiles and weakening global demand have all assailed the commodity. Meanwhile, Bloomberg data shows Russian oil companies raked in at least $905 million in additional revenues since November because U.S. sanctions on Iran and Venezuela have boosted demand for their particular brand of crude. And from black gold to gold gold: Investor angst is leading futures on the precious metal to a sixth weekly gain, their best streak in three years. And did you know the gold vault that floods when breached by bandits in Netflix's La Casa de Papel is a real thing? DataThis particular Friday feels – so far – like a typically August one. So let's try to get excited about data: University of Michigan consumer sentiment (due 10:00 a.m. Eastern Time) is expected to have fallen. Though as noted above, data Thursday showed strong retail sales in July, suggesting the consumer was holding up (at least before the latest escalation in the U.S.-China spat). Housing starts data (8:30 a.m.) are likely to show a slight rebound in July following a June decline. And oil-market watchers will get the latest Baker Hughes rig count (1:00 p.m.). MarketsOvernight, the MSCI Asia Pacific Index saw modest gains with Hong Kong's main index well ahead of its peers. Europe's Stoxx 600 Index rallied after two days of declines. S&P 500 futures jumped nearly 1% at 6:15 a.m. Eastern Time. The yield on 10-year Treasuries was 1.599%, and gold was lower. Also coming up…In a somewhat transparent effort to find a fifth thing, let's look at next week's events. Euro-zone final July inflation is due on Monday, Federal Reserve minutes are published Wednesday and central bankers gather in Jackson Hole Thursday. Data on mortgage applications and manufacturing are also on the schedule. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Luke's interested in this morningAs someone who talks to traders and strategists in the volatility space frequently, one thing I often ask is if the low level of U.S. Treasury yields helps them when pitching clients. That is, with rates so low, is it easier to talk up the prospective benefits of protection via direct exposure using puts on the S&P 500 versus the traditional embedded diversification provided by a 60/40 stocks/bonds portfolio and the presumption of a negative correlation between the two asset classes? Turns out, this premise might be completely off-base. Bonds have provided incredible protection this year. And Srinivas Thiruvadanthai, research director at the Jerome Levy Forecasting Center, wrote a tour de force report earlier this year that helps explain why. "One implication of the big balance sheet economy is that stock market declines have greater potential to trigger recessions and destabilizing debt dynamics," he writes. "Unsurprisingly, the downside capture ratio has been most negative in the 1920s, and 2010, both periods during which private sector balance sheets were large relative to incomes." His analysis shows that long bonds are increasingly offsetting damage done to the S&P 500. Let's do some back-of-the-envelope math to estimate how low yields would have to go for the 30-year Treasury to provide a sufficient offset to a material U.S. bear market. Lawrence Hamtil, financial advisor at Fortune Financial, makes the case that such a drawdown would be roughly 33%. Assuming downside capture from bonds in the same neighborhood of what's happened throughout this decade, that would put the benchmark 30-year yield in the ballpark of 50 basis points if such a risk-off episode were to play out over the next year.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. Before it's here, it's on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can't find anywhere else. Learn more. |

Post a Comment