Easy does it? If the Federal Reserve does not cut its target for the federal funds rate by at least 25 basis points at the end of this month, many in the market will feel entitled to sue the central bank for breach of contract. Wednesday's congressional testimony by Fed Chairman Jerome Powell and the publication of the minutes to the central bank's last monetary policy meeting were the last chance to walk back the widespread assumption that a July rate cut is a certainty. Powell made no attempt whatever to do so.

The market odds of a rate cut of some dimension are now 100%, and there is no precedent for the Fed bucking a market expectation that is this clear-cut this close to a policy meeting. We can assume that the Fed is in easing mode. In response, bond yields remain low and the benchmark S&P 500 Index of equities briefly topped 3,000 for the first time on Wednesday.

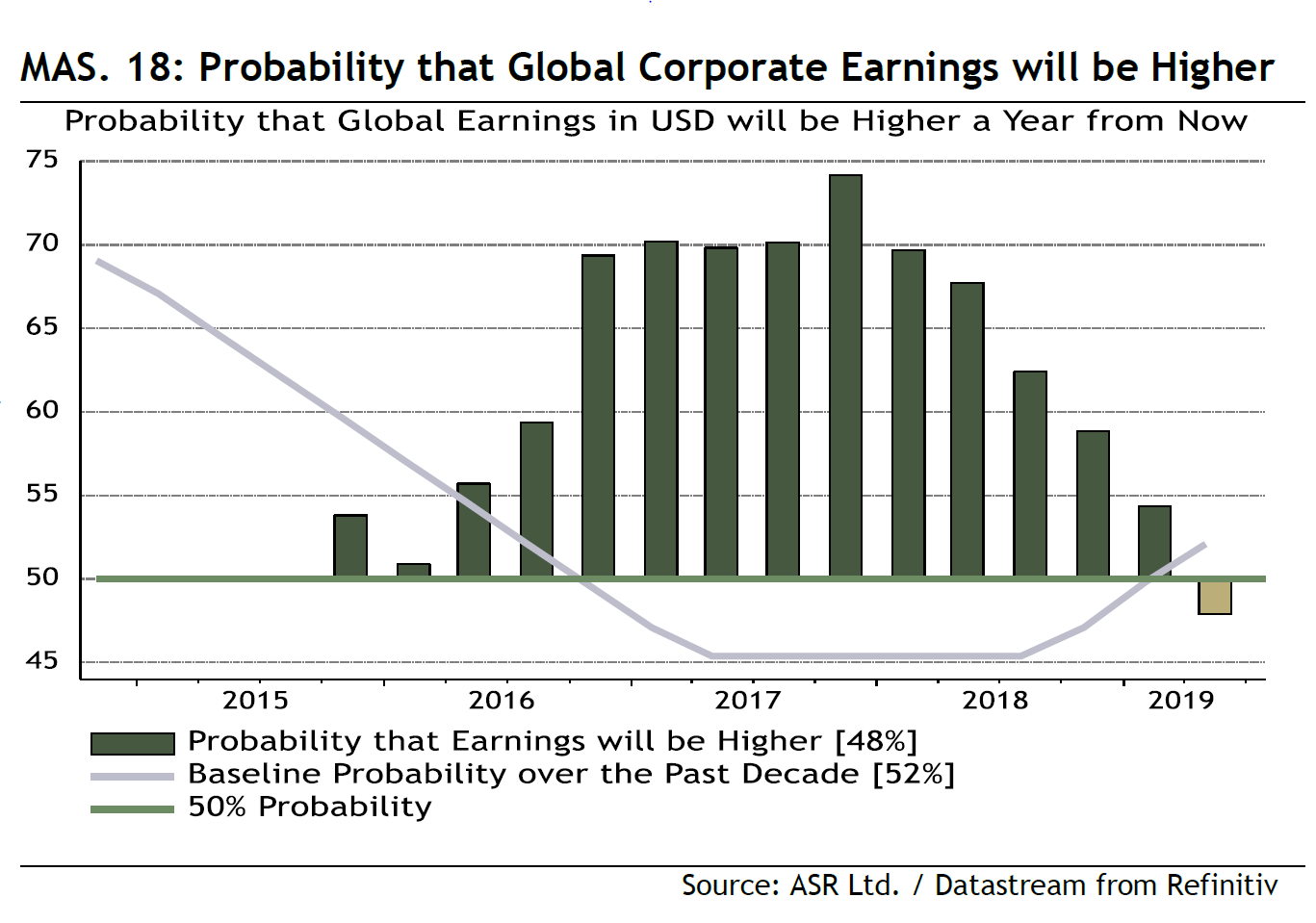

This is strange because investment managers have lapsed into a bearishness and pessimism that have not been seen since the financial crisis. That was the conclusion of the latest Bank of America Merrill Lynch monthly survey of fund managers, while Absolute Strategy Research's Multi-Asset Survey, which polls fund managers on their perceived probabilities of different outcomes, also suggests that investors are worried. Indeed, their predictions imply terrible problems for equities ahead. Only a minority believes that corporate earnings will rise over the next year, the most bearish outcome since the survey started:

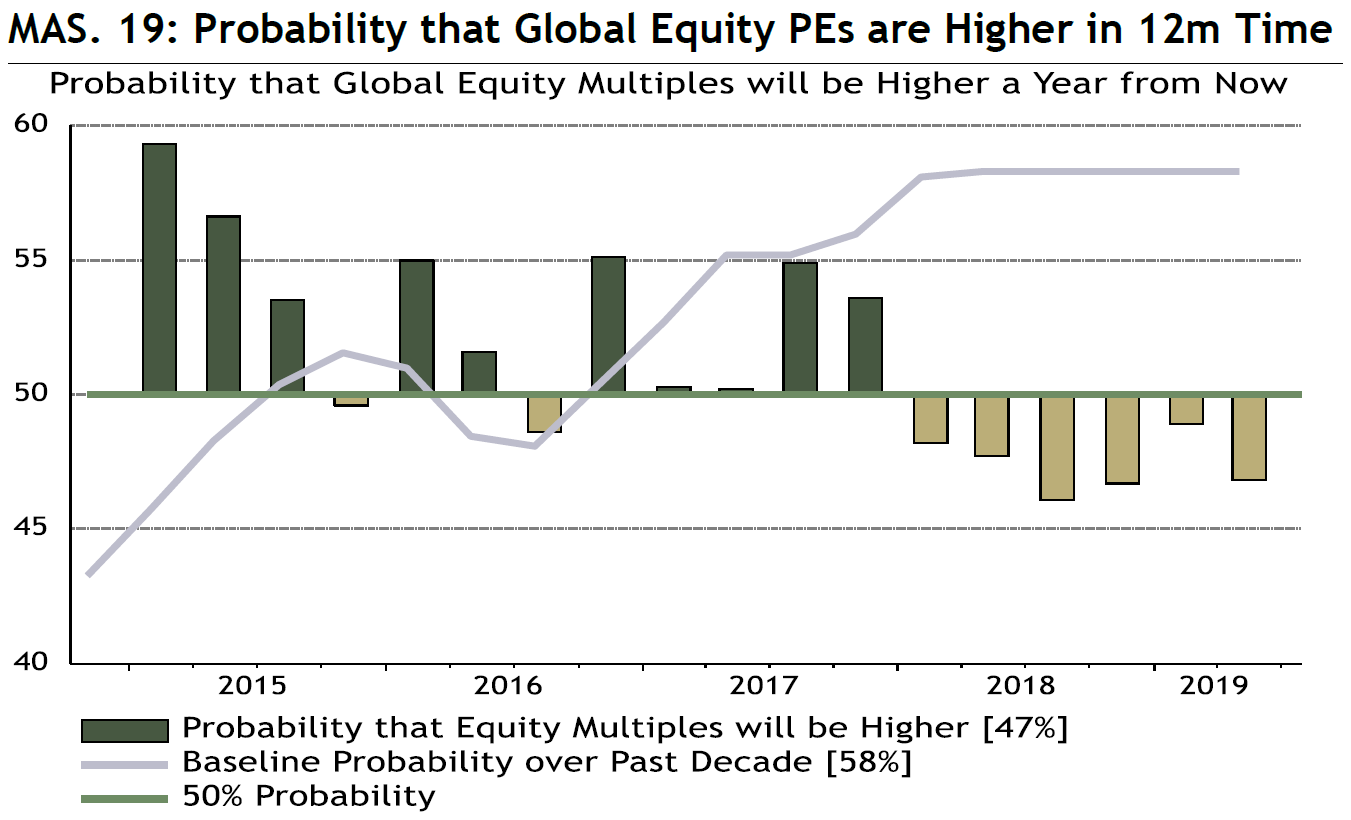

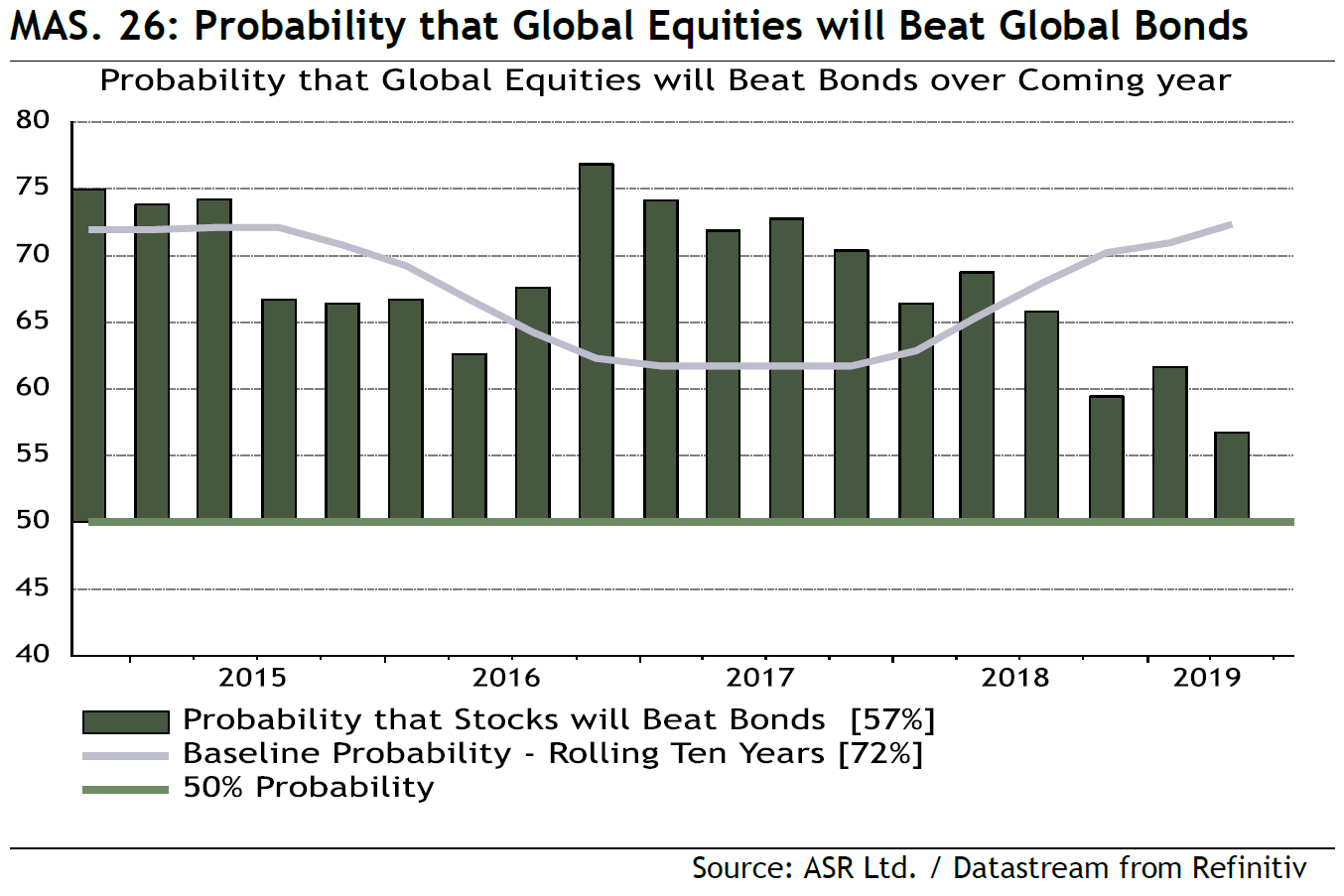

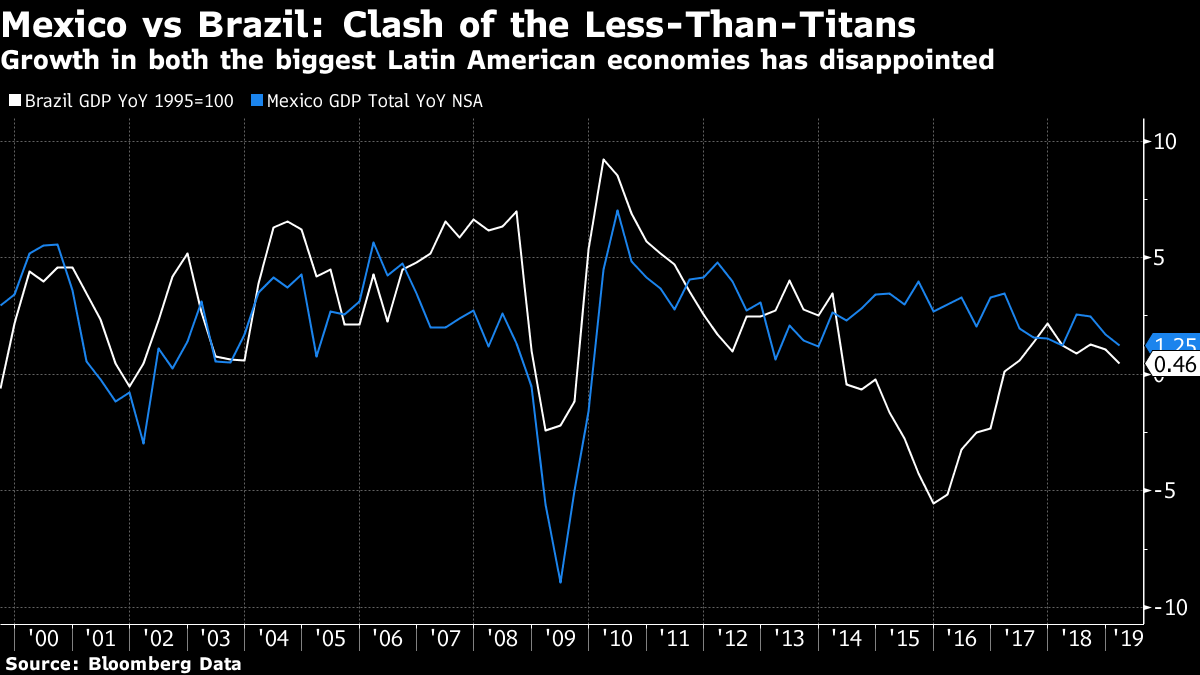

Meanwhile, a majority of institutions also believe that earnings multiples will be no higher in a year's time.  So, if we combine lower earnings with lower earnings multiples, it is only logical to expect lower share prices. Indeed, confidence that stocks will outperform bonds over the next year has dropped to its lowest in five years. But there is still a majority of investors who think bonds will somehow do even worse than equities:  The good news is that almost any good news would now constitute a positive surprise. Markets are primed for a triumph by optimists. The bad news is that if institutional investors are right, a few rate cuts from the Fed will not help much. Brazil 1 – Mexico 0 Before reading this section, Mexicans might like to watchthis video, which shows the final of 2012 Olympic men's soccer tournament, in which Mexico astonishingly beat a team from the world's greatest soccer nation Brazil. Even a young Neymar, who spearheaded the Brazilian attack, could not thwart a 2-1 Mexican victory. Now, on to the more relevant story for many readers, which is that Brazil is basking in adoration from international investors, while Mexico is totally out of favor. This is how Brazilian stocks have fared relative to Mexico over the last five years, as measured in dollar terms by MSCI:  Anyone who had put on a "long Brazil/short Mexico" trade in September would have made a 77% profit, even as world markets have been broadly flat. This is not, to be clear, because of any great gulf in economic performance. Growth for both of Latin America's two biggest economies is disappointing, just as it has been for a generation. At present, Mexico's growth is slightly less anemic, but neither country can tell an economic story to excite investors:  Rather, Brazil's dramatic outperformance is driven by politics, hope and fear. When its president Jair Bolsonaro, a right-wing populist, was elected last year, the greatest hope was that he could find a way to pass reform of Brazil's unsustainable national pension system. He had no clear plan to achieve this, but Congress appears now to be in the process of passing the reform. This is a critical breakthrough, as it should address the greatest issue facing Brazil: its escalating government debt as a share of GDP:  Combine the news on pension reform with the general global decline in bond yields, and the impact on government borrowing costs is already dramatic. Brazil's 10-year bond yields have dropped to their lowest in almost five years:  Faced with a horrifying problem like this, a breakthrough on pension reform is exactly what investors wanted. Meanwhile in Mexico, as I detailed on Tuesday, the resignation of Carlos Urzua as finance minister for the left-wing president Andres Manuel Lopez Obrador appears to fulfill the fears that the new administration will install cronies and push the country in an unsustainable direction. Mexican assets naturally fell under pressure once more. What should the future portend? There is a risk of overshooting in both countries. The prospects for pension reform in Brazil look very good, but it is not yet a done deal. Meanwhile, the Urzua resignation was damning for Mexico's government, but fences can still be rebuilt. But the greater issue lies with the U.S. and China. Mexico is more directly exposed to the U.S. than anyone else, while China has in recent years been a competitor that robbed the country of many manufacturing jobs. Brazil is not greatly exposed to the U.S., but its raw materials exports to China are central to its appeal for international investors. Hence, Mexico fared far worse during the 2008 U.S. recession, while Brazil slipped much more badly more recently as a China slowdown moved to head the list of global concerns. Mexico is one of the few countries that could conceivably benefit from a protracted trade war between the U.S. and China, which might see it regain jobs that had emigrated across the Pacific. A Chinese slowdown would be a disaster for Brazil. A peaceful resolution on trade, however, should be more obviously beneficial to Brazil than Mexico. At present, the choice between the two Latin American giants is driven by a choice between newly installed populist presidents, of left and right. But the next swing between the two will depend on the troubled relationship between the U.S. and China. Thank you for the continuing feedback on this month's book club choice, Red Flags by George Magnus. I now have a very provocative suggestion from David Kotok, the head of Cumberland Advisors. He zeroes in on the "trilemma" – the idea associated with the Nobel laureate economist Robert Mundell that a country cannot simultaneously have a fixed currency, a closed capital account and an independent monetary policy. It has to give up on at least one of these. As China does not want to cede control of its currency to the foreign-exchange market, or allow free capital flows, and certainly wants to maintain an independent monetary policy, that poses a big problem. Magnus calls this the "Renminbi Trap." We have already had the suggestion that the trap may not be as absolute as it appears – half-open capital flows and a half-floating currency might just allow China to maintain an independent monetary policy while keeping enough control over the towering heights of its economy, for example. Now, Kotok invokes the relevance of the gold standard: The reference to Mundell and the trinity provoked a thought as I saw the Chinese continue to acquire gold and pursue what seems to be a gold for USD substitution. China is not alone as we see others like India and Russia pursuing something similar. So my question involves how a gold substitute for USD alters the Mundell construction.

The recent expansion of negative rate sovereign debt to $14T only adds to the question as gold forward contracts have positive yield. Thus a country using gold as a part of its reserve allocation is incentivized to bias away from fiat currency and add to gold. This is a speculative assertion, of course, but the rising gold price seems to be reflecting the global downward march in interest rates. In a world where 95% of all high grade sovereign debt now yields below the fed funds rate and that rate is expected to fall, shouldn't we question the Mundell construction? And if we do, isn't gold reserve accumulation a force which might dampen the stress of Mundell's trinity?

Magnus doesn't consider this option. We ponder the question. Any Thoughts?

I have a lot of thoughts, although they are not yet well organized. Kotok is right that China is transferring to gold and has stepped up its purchases of late, but this is still on a very small scale. Its official gold assets are now $87 billion, according to the People's Bank of China. This is a lot of money, but still a tiny proportion of total Chinese reserves of more than $3 trillion:  And to be clear, the price of gold in dollars is its strongest in six years despite a global deflation scare, typified by collapsing German inflation break-even rates:  Deflation should make gold less attractive, as even paper money can gain in value over time – it loses the appeal that it works as a "store of value" that can guard against currency debasement. But I think Kotok is right that gold is benefiting from the loss of what is usually its greatest disadvantage – its failure to pay any yield. When bonds pay a negative yield, gold begins to appear much more attractive. But does the glittering prize of gold really allow China to escape endless compromises and find a way out of the Renminbi Trap? As Kotok says, thoughts welcome.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment