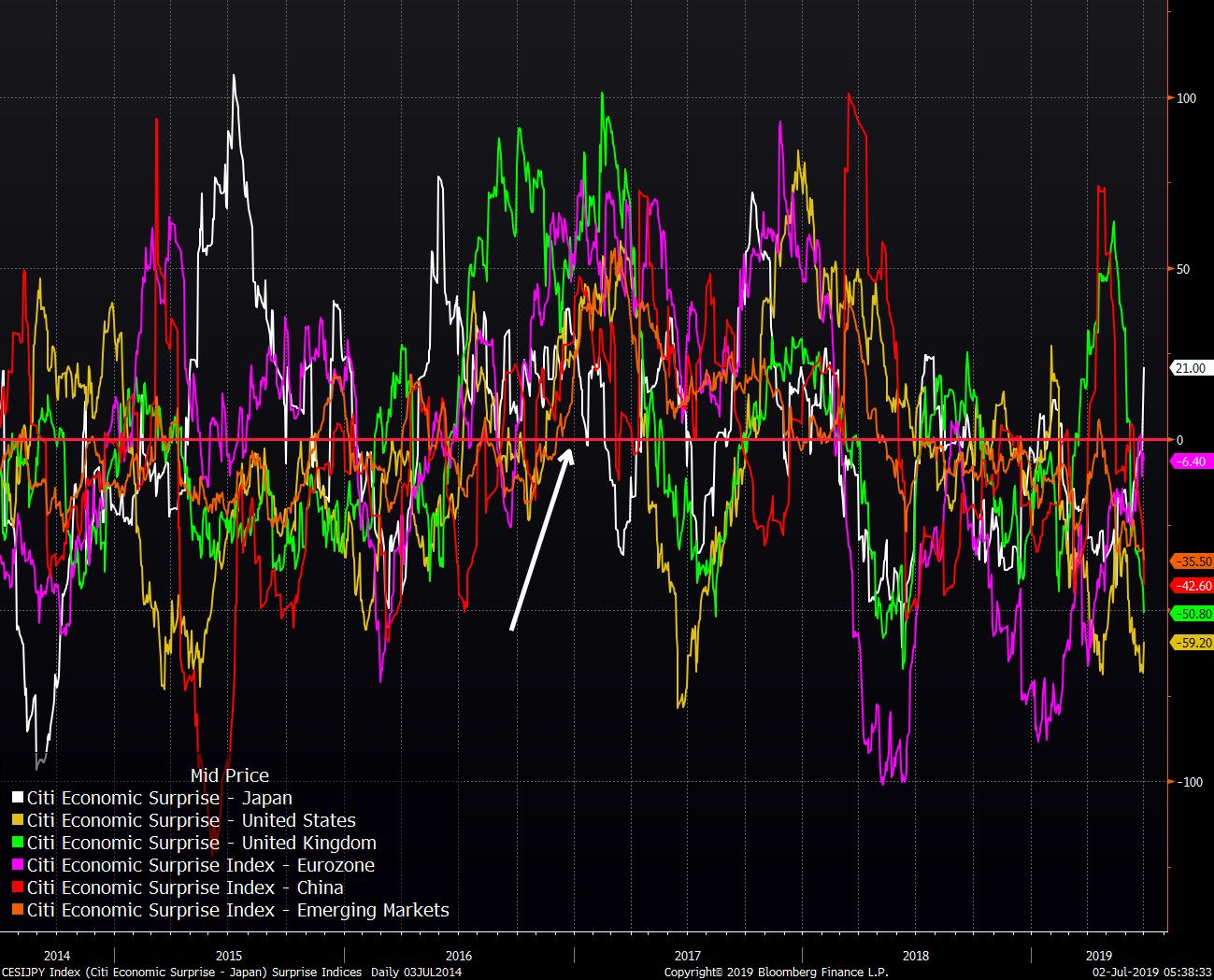

U.S. looks to hit Europe with tariffs, mega-IPO is back on, and the bond market is still in rally mode. This againThe never-ending dispute between the U.S. and Europe over support to subsidy-reliant aircraft manufacturers Boeing Co. and Airbus SE took another turn when Washington added $4 billion of EU goods that could be targeted as part of the tiff. Needless to say, the Europeans have their own list of retaliatory measures ready should the situation get more serious. Shares in Airbus dropped as much as 1.4% in Paris this morning, with the company calling the whole thing a lose-lose situation. One positive bit of news on the tariff front is that President Donald Trump said measures against Mexico are off the table after the country's response to immigration flows. And this againThe super mega-amazing IPO is back and this time it might actually happen. Maybe. Saudi Arabia is restarting preparations for an initial public offering of oil giant Aramco, the world's most profitable company. The history of this plan has already shown there is many a slip between cup and lip for the Saudi Crown Prince's goal of a $2 trillion valuation, but nevertheless it's what Mohammed Bin Salman expects to happen by early 2021. Also this is still happeningBond bears are continuing to have a terrible time. This morning the yield on Italian two-year debt turned negative for the first time in over a year. The German bund yield continues to hit new lows, with the 10-year yield closing in on the ECB's deposit rate of -0.4% as policy makers at that central bank hint at even more easing. U.S. Treasury yields are also holding near recent lows as Federal Reserve policy makers see the need for interest rate cuts. Markets mixedOvernight, the MSCI Asia Pacific Index climbed 0.4% while Japan's Topix index closed 0.3% higher as technology companies extended yesterday's gains. In Europe, the Stoxx 600 Index was broadly unchanged at 5:50 a.m. Eastern Time as investors rotated into more defensive stocks. S&P 500 futures pointed to a lower open, the 10-year Treasury yield was at 2.015% and gold was rising. Coming up…It's a quiet day on the data front today, with only auto sales numbers due. There is some policy stuff to watch out for though, with OPEC and its allies agreeing to extend production cuts and update their relationship status to something more formal. European Union leaders are trying again today to break the impasse over the distribution of top jobs in the bloc. Federal Reserve Bank of Cleveland President Loretta Mester is due to speak on the economic outlook later. What we've been readingThis is what's caught our eye over the last 24 hours. And finally, here's what Joe's interested in this morningThis week is jampacked with economic data, notwithstanding the July 4th holiday. Yesterday we got manufacturing numbers from all over the world, and the general gist is that they were bad, although the U.S. at least notched a reading in expansive territory. On Friday we get the latest Non-Farm Payrolls, which will be scrutinized after last month's flop of just 75,000 jobs. This time, economists expect a pickup to 164,000 and for the unemployment rate to hold steady at 3.6%. For a big picture look at how things are going, I've attached a chart of the Citi economic surprise index around the world. Each line, for those who aren't familiar with them, is a measure of how data is coming in relative to economist expectations. So the lines oscillate because they're naturally mean-reverting. As data deteriorates, analysts start slashing estimates, and then they go too far, and the data starts to exceed expectations again, and so on. I highlighted with an arrow a period in late 2016 where you could see that every line was above zero, meaning every region in the world was seeing economic data that bested forecasts. Fast forward to now, and it's basically the opposite. Virtually every line is below zero, with the exception of Japan. Of course, the lines will eventually bounce, but the question is whether it's a result of economic data improving, or economists realizing they're being overly optimistic and thereby slashing forecasts.  Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. Before it's here, it's on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can't find anywhere else. Learn more. |

Post a Comment