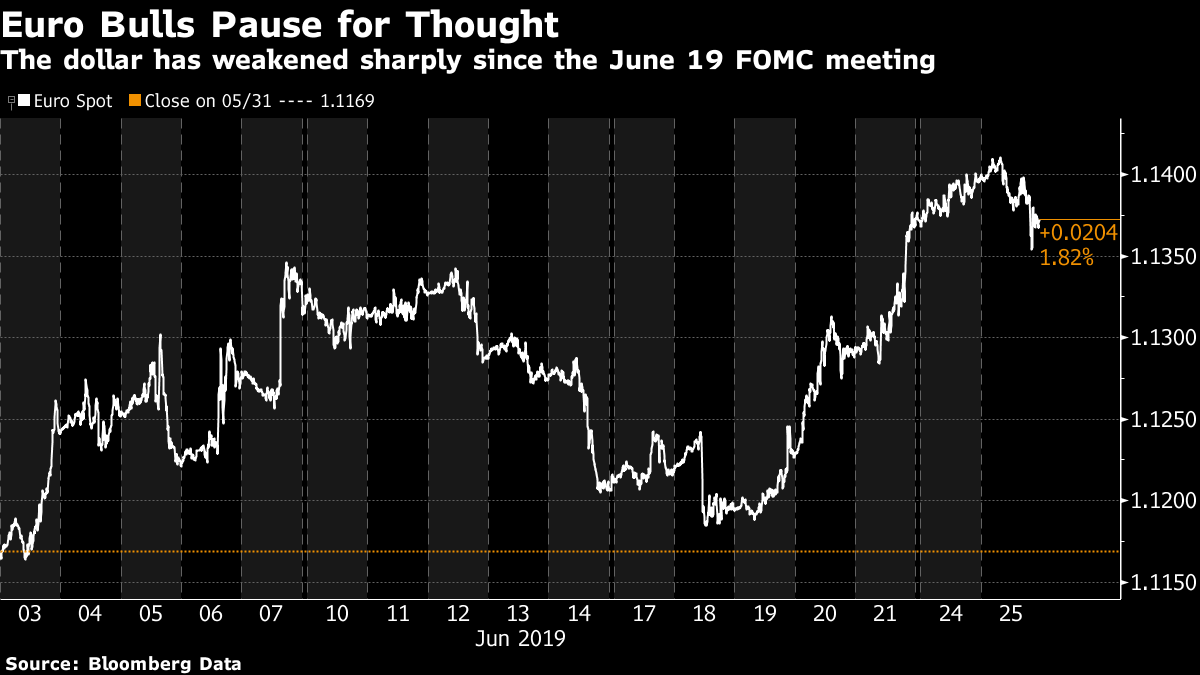

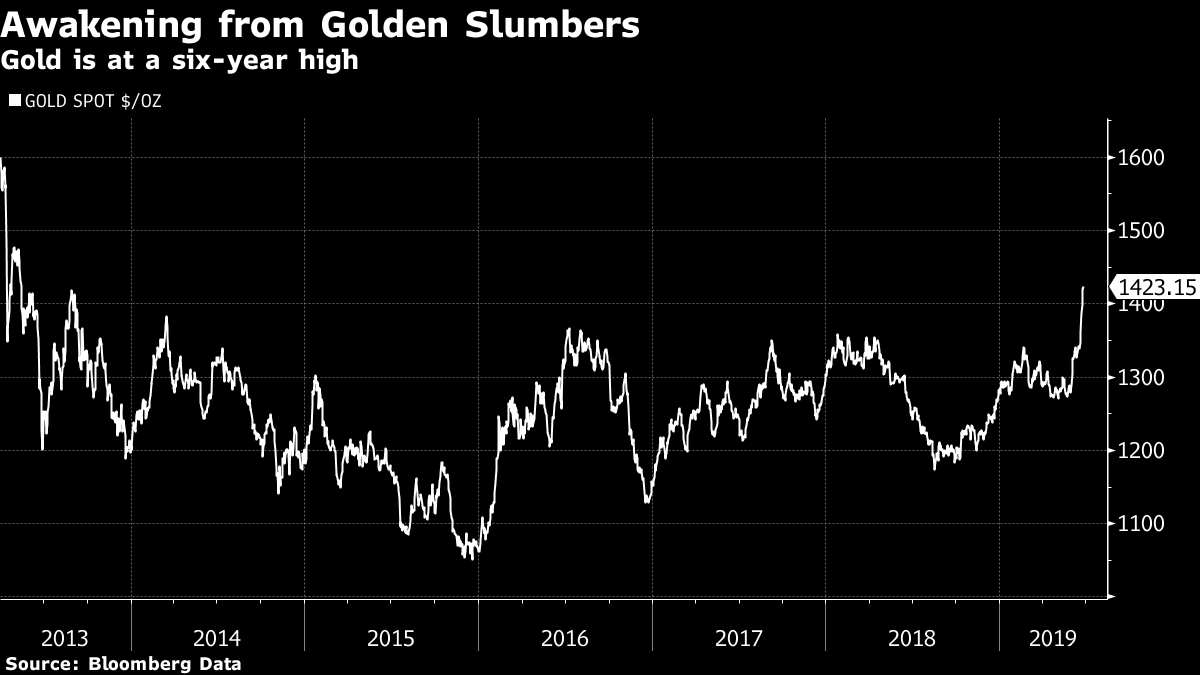

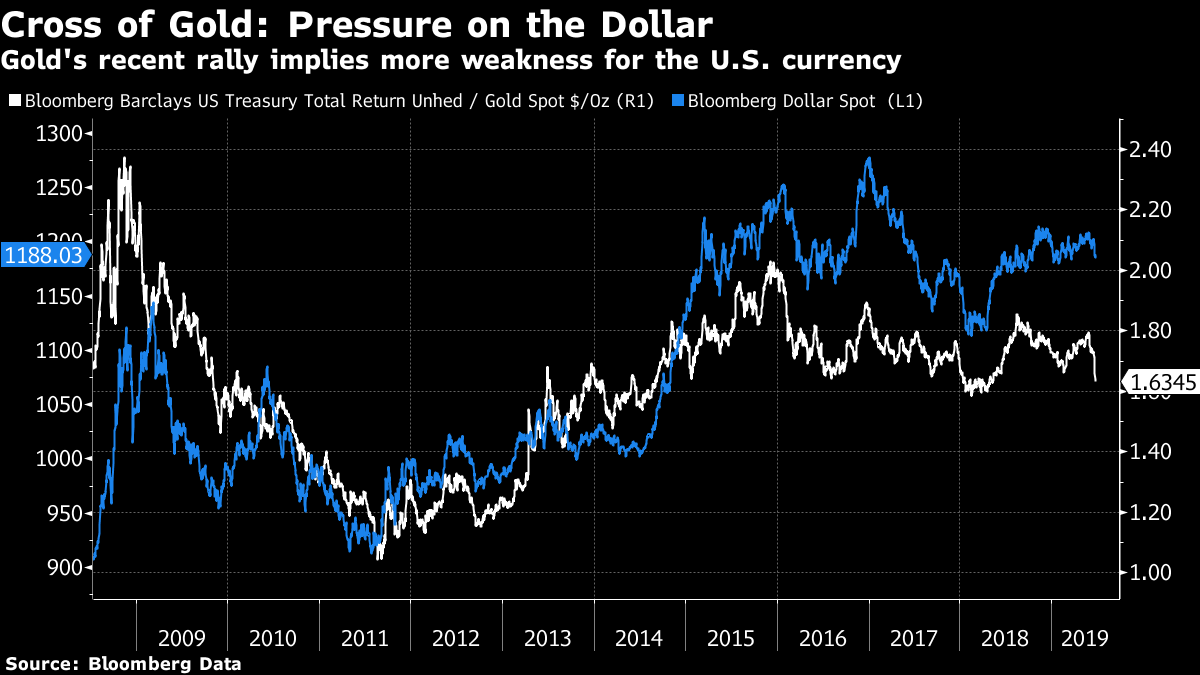

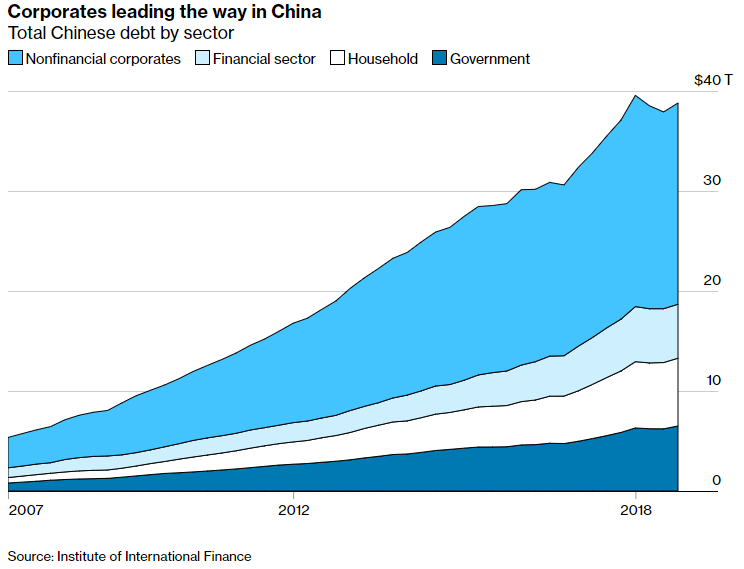

Reminder to the Fed: A weaker dollar would be helpful. A week after what turned out to be a landmark Federal Reserve monetary policy meeting, which set the stage for multiple interest-rate cuts starting as soon as next month, markets are still moving on every word from officials at the central bank. This helped the benchmark 10-year Treasury yield come to rest below 2%, which was quite a milestone. Stocks had a bad day Tuesday, as investors perhaps began to work out that assuming a sharp cut in rates assumes a sharp slowdown in economic activity. However, the most important market to watch is the one for currencies, for it is the dollar that holds the key to getting us all through the many political and economic risks for the rest of the year. The chart below shows what has happened to the dollar-euro exchange rate over the last month. Essentially the dollar has weakened following last week's Fed policy meeting. This is a bet on lower rates, rather than a serious positioning for the kind of awful economic conditions that would be required to justify the three or more rate cuts that money markets expect.  Tuesday brought the first serious sign of a rethink of Fed policy. A sharp drop in the euro was a reaction to comments by Federal Reserve Bank of St. Louis President James Bullard at around noon New York time. Bullard publicly dissented last week from the Fed's decision to hold rates steady in favor of cutting them immediately. Bullard is a known dove, but it was shocking when he said that an "insurance" cut of 25 basis points was needed, but he doubted that the 50 basis points that many in markets are banking on are needed. In other words, markets were priced on the expectation that he would be far more negative about the economy as Tueday's surge in the dollar suggested. But when Chair Jerome Powell subsequently commented that growth was disappointing, the dollar gave up some of its gains. The ongoing drop in U.S. bond yields has reduced upward pressure on the dollar by bringing the spread, or extra yield available on Treasuries relative to European bonds, back from what appeared to be extreme levels. But the spread remains wide:  However, moves in the price of gold suggest that there are downward pressures on the dollar this time. Unlike previous periods when rates declined, this has one has been accompanied by surging demand for gold, pushing prices to the highest in the more than six years:  What does this tell us? BCA Research highlights the importance of the bond/gold price ratio, which has sharply declined, implying further weakness for the dollar lies ahead, as this chart shows:  Why is there such a relationship? This is BCA Research's explanation: Interest rate differentials are moving against the dollar, but our important takeaway — that gold continues to outperform Treasurys — is an ominous sign. Gold has stood as a viable threat to dollar liabilities, any sign that the balance of forces are moving away from the U.S. dollar will favor a breakout in the gold-to-bond ratio. The rationale is pretty simple. Investors worried about U.S. twin deficits and the crowded long bets into Treasurys will shift into gold, favoring gold at the expense of the dollar. The gold-to-bond ratio and dollar tend to move tick for tick, so a breakout in one can be a signal for the other. The breakdown this week is a bad omen for the U.S. dollar. All of this matters because a weak dollar makes life easier for almost everyone. President Donald Trump, still attacking Powell in unprecedented fashion, wants a weaker dollar to help reduce the trade deficit. China also wants a weaker dollar because it makes it far easier to avoid a devaluation of its own currency. A weaker dollar relieves pressure on emerging markets around the world, and particularly those like Turkey and Argentina that have borrowed heavily in dollar-denominated debt that needs to be repaid. The euro zone's exporters could do without a stronger euro, but at least a weaker dollar gives U.S. investors more incentive to invest in European companies and thereby reduce the downward pressure on European share prices. And then there is the most important indicator of all for Trump, which is the U.S. stock market. During the post-crisis decade, all its periods of relative weakness have come during periods of dollar strength. When the dollar is weakening or stable, the S&P 500 has surged. The following chart shows all the periods of dollar strength, with the line for the Bloomberg Dollar Spot Index inverted for clarity.  Stocks had a bad day Tuesday as the dollar strengthened a bit. This was not coincidental. In the long term, the dollar cannot weaken forever. A dollar that perpetually depreciates would mean faster inflation with higher interest rates to follow, and it would probably only happen as a result of a serious economic slowdown. A weaker dollar is no kind of long-term solution to the worries about global growth, but for the next few months, it could make all those problems much easier to ignore and allow for one last U.S. gasp in the bull market in stocks. But if the rally is founded largely on a falling currency, there should be better alternatives. Gold would be a direct way to profit from a weakening dollar, while long-suffering European and emerging-market equities should also beat the U.S. in these circumstances. China's debt trap. What is going on in China? Most of us are focused on China's international relations at present, and particularly its trade relationship with the West, as the Group of 20 summit in Japan approaches. This is understandable, but might still fail to capture what is most at stake for the West's relationship with China. That is one of the most important lessons from the first four chapters of George Magnus' "Red Flags," which is this month's Authers' Notes book club selection. These chapters introduce us to China's economic history and take us up to a detailed description of what Magnus labels the "debt trap." I suspect that this issue is at the heart of the fluctuations in world markets today. To frame the issue, many focus on the amount that China has been allowed to export to the rest of the world since joining the World Trade Organization in 2001. But trade relationships are two-sided. China's role in the savage decline in U.S. manufacturing jobs is undeniable, but it also had a valuable role for the rest of the planet as the buyer of last resort. From WTO accession to the financial crisis, China's imports grew at an extraordinary rate. Once the crisis hit, China's huge fiscal stimulus of late 2008 allowed import growth to resume, and was vital in stopping the Great Recession from turning into something much worse. At this point, there was a tendency to extrapolate rising imports into the future at the same rate. That has not happened:  The chart shows a 12-month moving average to smooth out the effects of China's annual shutdown for the Lunar New Year. The era of extrapolation is over, as Magnus would put it, and the most recent trend in imports is slightly down. The trade friction of the last 12 months has a little to do with this at the margin, but what matters most by far is China's underlying economic appetite. That has been faltering for a while, and it is increasingly dependent on credit to spur growth. That was rammed home after the Chinese economy slowed alarmingly in 2015, causing a serious correction in world markets, and then stabilized after a big extension of credit. This is why so many care about Chinese credit, and why China's attempt to deal with its debt trap is at least arguably more important than its attempt to deal with Trump. At the end of last year, with China opening the credit taps again, risk markets around the world were able to rally in large part because of the belief that another Chinese period of reflation was on the way. Whatever the arguments that will be made in Osaka, it is plain that investors badly want China to keep borrowing and pile on debt at an even faster rate. If that is the short-term interest, however, there is a different longer-term interest, which is avoiding a massive credit crisis. Ever since 2008, fear of a Lehman-style credit implosion in China has pervaded markets, and China has continued to avoid any such denouement. Such a fear seems reasonable, as this chart, using figures from the Institute of International Finance, demonstrates:  So in the short run there is a widespread interest in China continuing to borrow, and in the long run there is a fervent desire for the country to head off a debt crisis. How to reconcile these and avoid the debt trap? The good news from Magnus is that a Lehman-style crash can and probably will be averted. He points out that President Xi Jinping has started to talk about financial security in the same way that he addresses national security, and that his assertion of authority has involved taking government control over debt. He details carefully how virtually every lever of credit creation has in the last year been brought ultimately under the control of Xi and the party: From an organisational standpoint, there would not now seem to be any obvious reason for a repeat of past financial excesses and abuses. Any mistakes or failures in future will be down to the decisions made by the holders of high office. This is important because the stimulus efforts of 2008 and 2016 were not primarily achieved with central government debt, but with local governments' off-balance-sheet activity in 2008 and with swaps involving local government financing vehicles in 2016. The echoes of the Lehman disaster will be clear to all who lived through it. But armed with control over all forms of debt, both on- and off-balance-sheet, and at the local as well as the central government level, Xi has been able to reshape China's credit landscape. This has costs. Magnus finds "a serious problem not just of weak regulation, which is now being partially addressed, but also of weak governance and operational management which are not only being inadequately addressed but are being exacerbated because of new political interference." He continues: China could become embroiled in a debt crisis arising from the increase in the burden of debt and the decline in capacity to shoulder it, but this does not seem a likely outcome. It is much more likely that debt will loom over the economy, manifesting itself as lower economic growth than as a crisis per se. Xi now has the ability to avert a systemic crisis by reining in excesses. He does not necessarily have the ability to thwart an economic slowdown. Armed with this frame of reference, I think the following chart, compiled by Absolute Strategy Research of London, is very informative as it includes all forms of debt:  There are two key takeaways. The first is that each measure of stimulus, when we look at the totality of debt as a proportion of GDP, has been far smaller than the one that came before it. (And if we refer back to the imports graphic, we can see that the economic impact of each successive stimulus has reduced even more.) The second is that the expansion of central government and official local government debt that aroused so much hope at the turn of the year was not about stimulating growth. Instead, it shows the hand of Xi in reducing vulnerability to a systemic crisis by ruthlessly reining in the excesses of the last two rounds of stimulus. Policy makers in the U.S. and Europe would have loved to have such power a decade ago. But the bottom line is that as China takes control over its financial system, its economy remains without the much hoped-for dose of stimulus. I think Magnus' key conclusion is the following: It is hard to imagine how the government can avoid the key challenge of the debt trap, other than by accommodating a proper and sustained deleveraging. Appropriately executed, this must entail an extended growth hiatus. … China cannot have high rates of economic growth on the one hand, and on the other hand simultaneously reduce the risk of financial stability. It looks as though just such a deleveraging is indeed being appropriately executed. Which is dreadful news in the short term for those hoping to avoid an economic slowdown both in China and the rest of the world. Any comments on this would be very gratefully received, as ever. Emails on this subject should go to authernotes@bloomberg.net, please, and we also have an IB chat room on the Bloomberg terminal where you can discuss these issues in real time. Just send an email to that address and we can give you access. I hope to produce another newsletter with "Red Flags" feedback next week. Britain's Whitehall farce has moved on to a contest between the current and former foreign secretaries, Jeremy Hunt and Boris Johnson, for the Conservative party leadership and hence the premiership of the U.K. The chances of either a "no deal" exit from the European Union or – perhaps more realistically – the biggest constitutional crisis in generations and a general election, continue to grow. One of the problems is the electorate, which is the body of dues-paying members of the Conservative party. British parties are not as open as their U.S. equivalents, and so this is nothing like a presidential primary. As this excellent piece in the New York Times explains, the total electorate is only 160,000, or 0.3%, of the British population. Wildly unrepresentative of the populace as a whole, Conservatives tend to be whiter, older and far more antagonistic to the EU than the average Briton. This explains why Johnson has promised "Brexit, do or die" on the current EU deadline of Oct. 31, meaning that he would leave without a negotiated settlement if necessary. Markets are priced on the assumption that this would be economically disastrous. He has challenged Hunt to promise the same, and received a more guarded promise to leave on Halloween. Meanwhile, Hunt is needling Johnson about his refusal to take part in a televised debate planned for Tuesday. This has even included a Twitter spat, to which Hunt has contributed the hashtag: #BoJoNoShow. If this sounds reminiscent of U.S. politics, it should. Meanwhile, both candidates ignore the fact that a number of Conservative MPs are on record saying that they would vote to bring down the government and force a general election rather than allow a "no-deal" exit to occur. Potential winners of that election include Labour's Jeremy Corbyn, described by Conservatives as a Marxist, and the Brexit Party's Nigel Farage, who was described as a Facist by his school teachers. Add to this that both candidates say they would not go forward on the basis of the withdrawal agreement negotiated by current prime minister Theresa May, and that it seems quite impractical to negotiate anything else in the time available before Halloween. Thus both seem to have committed themselves to "no deal." And so the situation is dangerous for anyone who has money tied up in Britain – and even more so for those of us who regard the country as home. Beyond the narrowness of the electorate and the narrowness of the options they are offering to the country, there is also the issue that the two candidates sprang from an alarmingly narrow pool of candidates. Both were ardent student politicians at Oxford University in the 1980s. (Full disclosure: I was a contemporary of both.) If any readers want to immerse themselves in the fetid atmosphere of 1980s Oxford student politics, I can guide you to my own piece on the baleful influence of the Philosophy, Politics and Economics degree, which produced virtually all the politicians who built Britain's relationship with the EU and whose mishandling of the economy prompted the population to revolt; and this piece by my former colleague and Oxford contemporary Simon Kuper on the group of largely privileged and privately educated chancers who led the charge for Brexit. Despite their great similarities, Hunt belongs more to the former, and Johnson more to the latter. Hunt is a far less flamboyant figure than Johnson, but has marked himself as a political survivor after weathering crises he created for himself in past jobs as media and then health minister. He has been in the cabinet uninterruptedly for nine years. It is fair to assume that he knows that a no-deal exit would be a very bad idea. Johnson is much more flamboyant, to put it euphemistically. He has already attracted profiles in the New Yorker (written by yet another Oxford contemporary), and the New York Times. There are plenty more where they came from. My personal favorite recommendation in the Boris genre is this extraordinary piece by Max Hastings, his former editor at the Daily Telegraph (the lynchpin newspaper of British conservatism). You could also read this earlier piece by Hastings, headlined: "Boris Johnson: brilliant, warm, funny – and totally unfit to be PM." This quote gives a flavor of Hastings' feelings about the man, but it is worth reading these pieces in full: If the day ever comes that Boris Johnson becomes tenant of Downing Street, I shall be among those packing my bags for a new life in Buenos Aires or suchlike, because it means that Britain has abandoned its last pretensions to be a serious country. And for a very much calmer take on the Johnson phenomenon, try this excellent podcast produced by a Cambridge academic. As for investment recommendations, suffice it to say that it is still hard to recommend British assets, even though they are selling at a Brexit discount. The U.K. still has many advantages, and will survive this awful self-inflicted mess. But there are many ways that things could get worse before they get better. To buy now would be to place a bet rather than to make an investment. See you next week. Unfortunately, I will be spending the rest of this week returning to my hands-on "investigation" of the U.S. healthcare system. Thanks for your patience, and I will be back next week.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment