Welcome to the Weekly Fix, the newsletter contemplating a Federal Reserve disowning an "America First" doctrine. –Luke Kawa, Cross-Asset Reporter

Our Currency, Your Solution

Richard Nixon's Treasury secretary John Connally is famously credited for telling foreign policy makers that the U.S. dollar was "our currency and your problem."

Nowadays, it's more like "foreign affairs are America's problem," and a cheaper dollar is the world's solution. Federal Reserve Chairman Jerome Powell this week highlighted slow global growth and uncertainty surrounding trade policy in explaining a monetary-policy pivot that exceeded analysts' expectations for its dovishness.

"It's really trade developments and concerns about global growth that are – that are on our minds," he said in the press conference. "So we're not exclusively focused on one event or one piece of data. Risks seem to have grown."

Powell struggled to answer a question about what a rate cut would do to help the American economy. That's because it's not really about the U.S. economy. It's about the positive second-order effects that would wash up on America's shores should a Fed rate cut buoy global economic activity. Bloomberg Opinion's Daniel Moss elaborated on this point, concluding that the Fed's willingness to add accommodation was not necessarily an "America First" position.

Fed Vice Chairman Richard Clarida's interview with Bloomberg on Friday, in which he'll be asked to expound on the Fed's decision-making process, will be must-see TV.

Clarida, when at Pacific Investment Management Co., penned an op-ed shortly after the 2016 election, writing that "in a world of global capital flows there will be a limit to how far U.S. rates can diverge from global interest rates without triggering volatility in markets and a much stronger dollar that reduces exports."

This America-centric statement focuses on the direct, real-economy effects of a lofty currency. A weaker currency has been seen as good for a nation because it incentivizes domestic production over imports and may, at the margin, help exporters. But a world of globalized supply chains means exchange-rate shifts don't make as big of an impact on trade as in the past. Instead, the financial-market effects of currency fluctuations have dominated.

This matters because the dollar is on the way down. The two-day drop of 1% for the Bloomberg Dollar Spot Index Wednesday and Thursday was the biggest such decline since February 2018.

And a depreciating greenback should boost credit overseas. As Hyun-Song Shin of the Bank for International Settlements wrote in a 2014 paper, local borrowers' balance sheets become stronger when their currencies appreciate, "resulting in lower credit risk and hence expanded bank lending capacity." Ethan Harris at Bank of America Corp. put it another way, ahead of the Fed meeting Wednesday, saying that U.S. rate cuts could be framed as "a cure for the world."

"Fed easing is a big boon to the more vulnerable economies because it allows their central banks to cut rates without causing significant currency depreciation," Harris wrote. "If you are looking for a silver lining in the trade war and in the persistent weakness in U.S. inflation, it is the Fed's willingness to ease policy, and the implicit accommodation that would provide for some economies that are particularly vulnerable to global shocks."

The response in global equities – a strong two-day showing, with emerging market and internationally geared stocks outperforming – testifies to these sentiments.

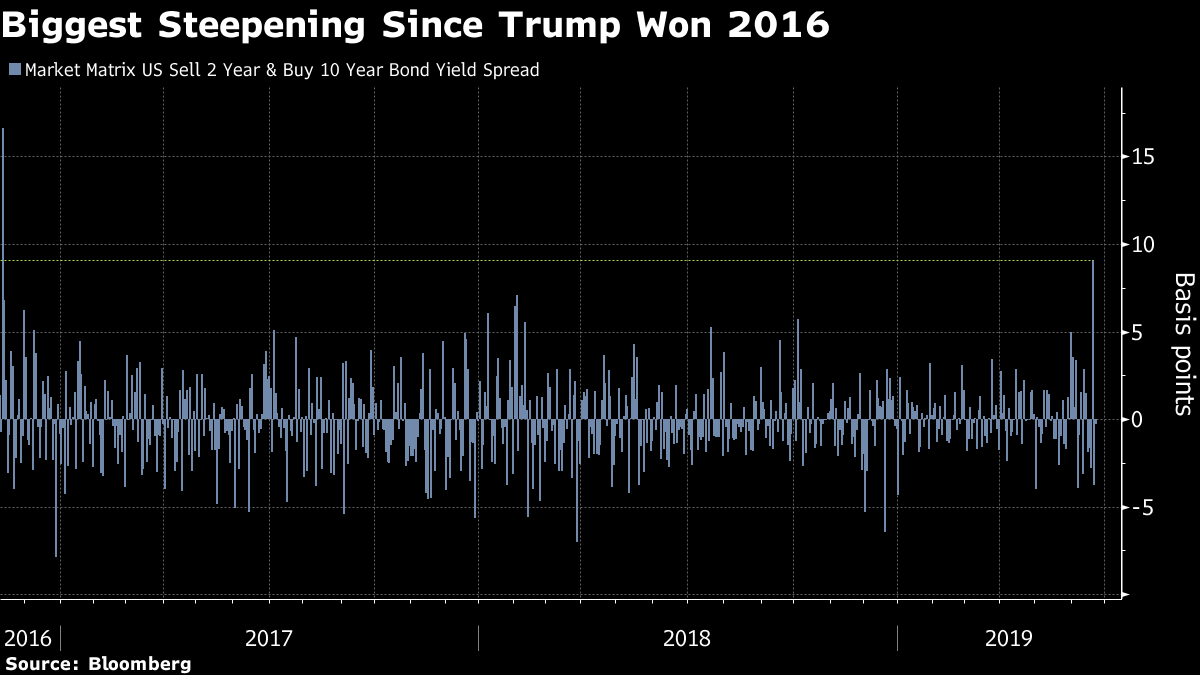

Meanwhile in the U.S., the Fed's stance fortified the market's faith that everything will turn out a-okay. The so-dubbed the Big Dipper curve shows the degree of investor optimism in downside scenarios being avoided. The three-month, 10-year yield spread became as much as 5 basis points more inverted right after the Fed decision. The bigger story, though, was the (bull) steepening in the two-year, 10-year curve – the biggest such move since the session after Donald Trump's shock 2016 election win.

Powell provided the most explicit evidence yet that the central bank is aware of the benefits of acting early to cushion the economy from downside risks.

``It's wise to react, for example, to prevent a weakening from turning into a prolonged weakening," he said. "In other words, sort of, an ounce of prevention is worth a pound of cure."

There's a school of thought that says cuts now would be akin to wasting ammo. But the Fed has already more or less conceded that it doesn't have conventional policy space to fight garden-variety recessions, so that argument is irrelevant. Recession prevention, as Powell identified, becomes the only game in town.

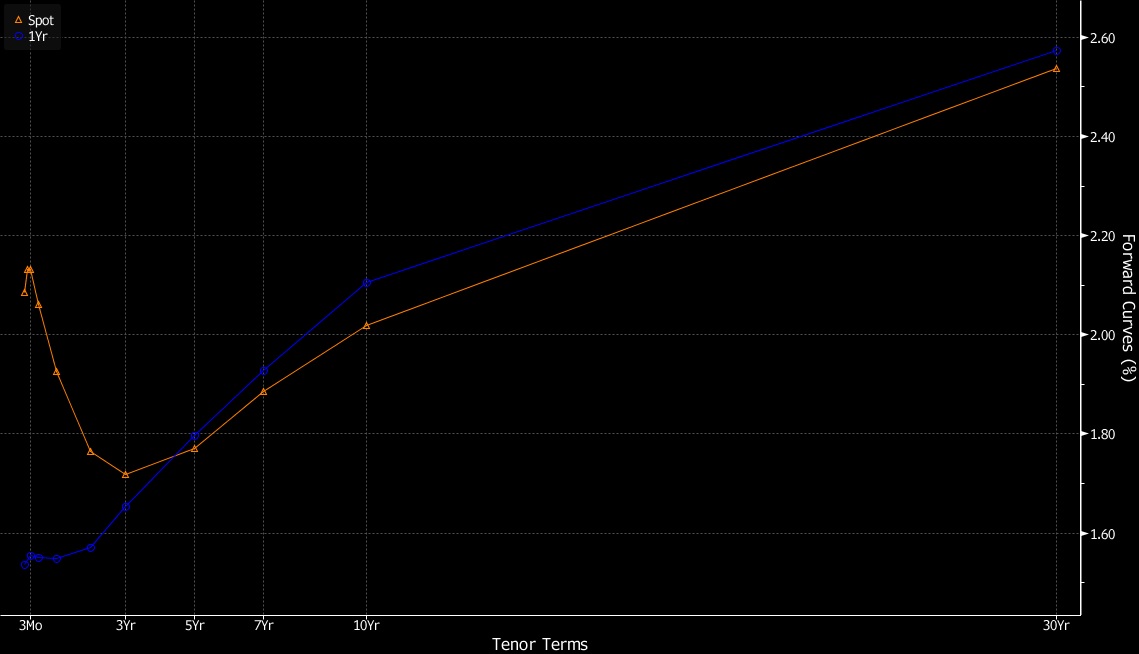

Forward markets imply that the U.S. curve will twist-steepen over the next year: that is, yields at the front end will fall precipitously as the Fed delivers cuts, while rates on 10-year notes and longer maturities will creep higher. This is consistent, relatively speaking, with a narrative that easing will be sufficient to buoy the global economy and lift all boats.

The 30-year yield has already erased all of its post-election rise. The 10-year yield is little more than a quarter-point away. But the two-year yield is still well above its November 2016 level. Put together, if the Fed is about to embark on its easing cycle, there's sufficient scope for all of those tenors to fall with a bull-steepening trend intact. The global economic outlook is not brighter than it was in late 2016, when economic surprise indexes around the world were swinging to the upside with the promise of U.S. fiscal stimulus to throw propane on the fire.

And to build on last week's argument that bonds are actually the optimistic asset class, Bloomberg Intelligence's Gina Martin Adams estimates that the S&P 500 Index's multiple would be higher if equity investors believed the easing that is priced in will actually be delivered – to the extent that it could leave the benchmark index in the neighborhood of 3,200, against Thursday close of 2,954. The bull case is that lower rates boost multiples. The super-bull case is that Fed cuts boost the rest of the world and lift earnings power, too.

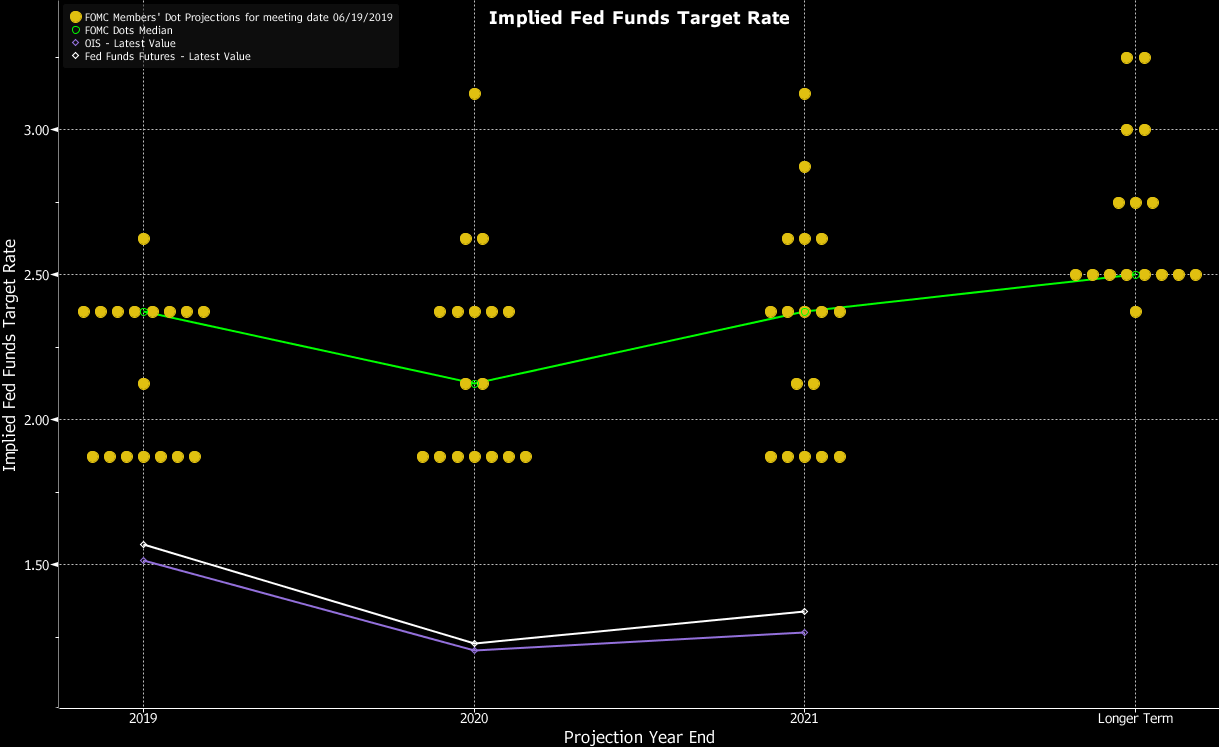

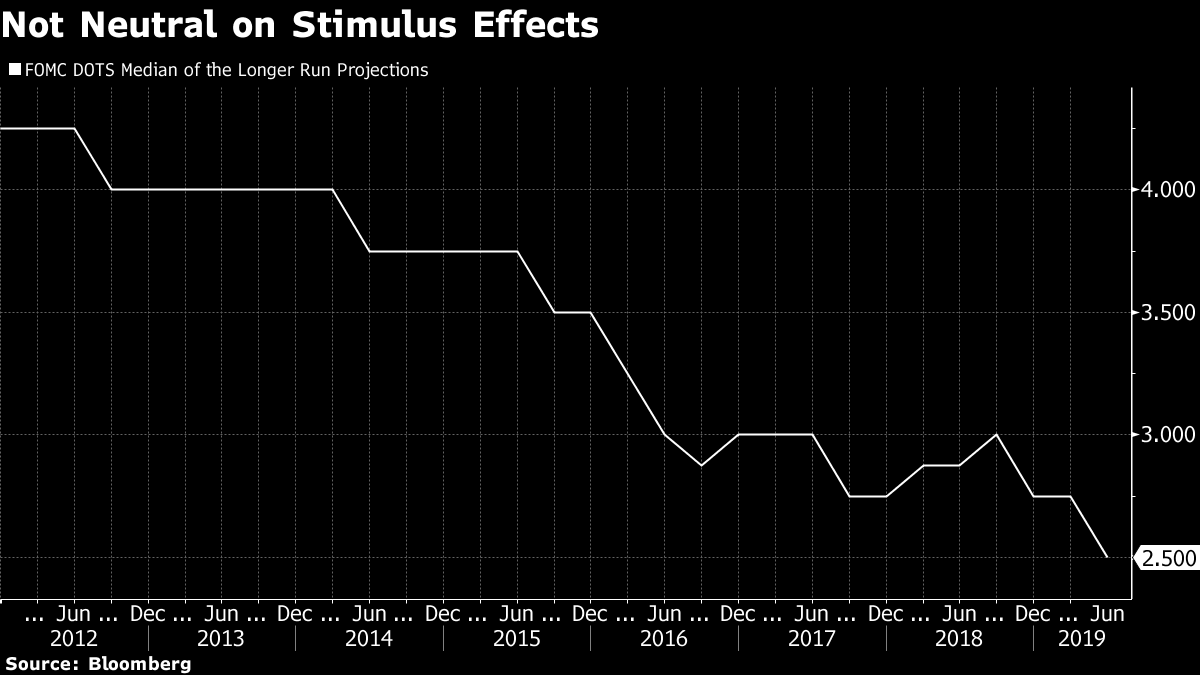

The nearly universal response from Wall Street was that the central bank's communiques on Wednesday were very dovish – especially because the dot-plot of rate projections pointed to a reduction (in 2020) for the first time in its relatively brief history.

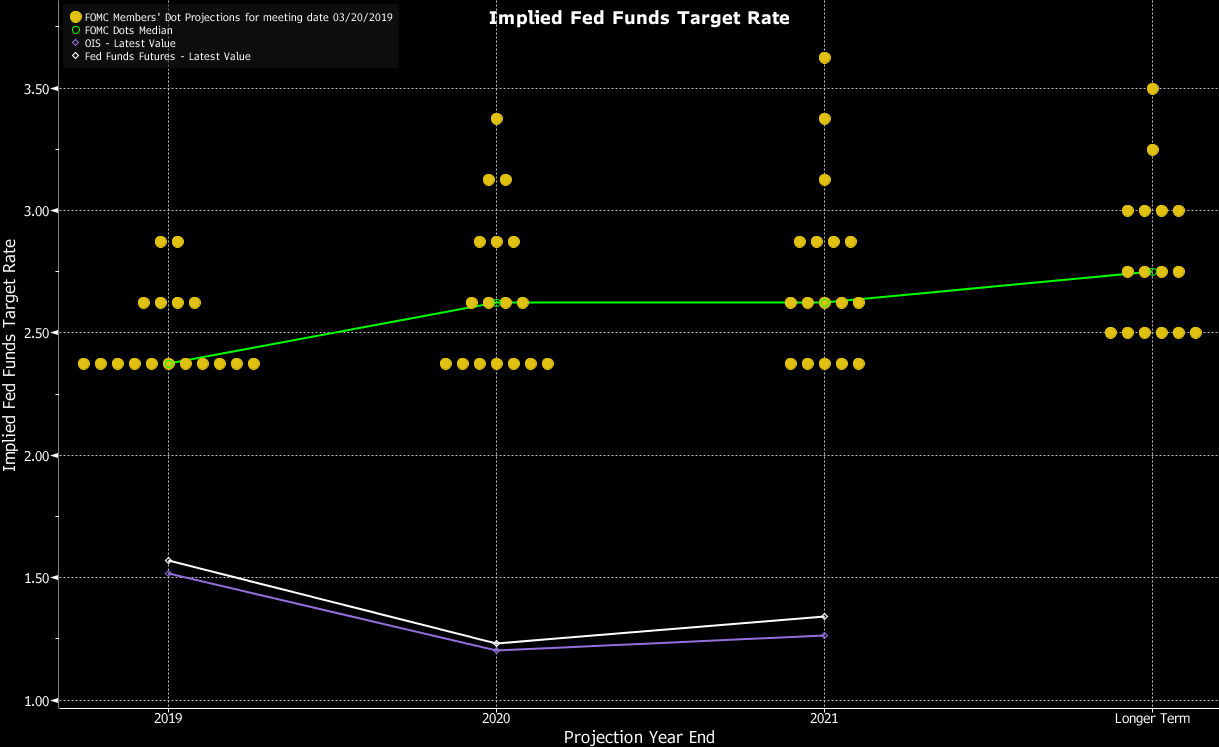

But was it really? For all the talk about increased near-term risks and a swelling case for adding more accommodation, there's an argument to be made that the Federal Open Market Committee had actually penciled in an estimated policy path that's tighter than the one they outlined in March, at least in the near-term.

In March, the median dot, when compared against the long-term "neutral" dot, implied accommodation of 37.5 basis points in 2019 and 12.5 basis points in 2020 and 2021.

Now, the sinking of the long-term dot implies that the degree of accommodation provided by keeping rates unchanged has lessened to 12.5 basis points this year, 37.5 basis points in 2020, and back to 12.5 basis points in 2021.

In essence, this bolsters the case for taking action in order to support the economy – if the risks are indeed higher, as the central bank indicated. Markets are bettingat least 25 basis points of easing will arrive next month.

There are other implications of that drop in the long-term dot. For Hindsight Capital, it serves as evidence that the December rate hike was a policy mistake. The Fed listened to the Trump administration too much on the potential supply-side benefits of its tax plan, it seems, and not enough on its diagnosis for proper monetary policy.

The Fed found religion on supply-side at precisely the wrong time, nudging up its estimate for the neutral rate. In Clarida's first speech as the Fed's No. 2, he pointed to market-based signs that the neutral rate had increased recently, and talked up the scope for business investment to increase.

A recent IMF publication highlighted the flaws in that argument.

"We find that U.S. business investment since 2017 has grown strongly compared to pre-TCJA forecasts and that the overriding factor driving it has been the strength of expected aggregate demand," the researchers wrote, using the letters for the name of the legislation. "Investment has, so far, fallen short of predictions based on the postwar relation with tax cuts."

Post a Comment