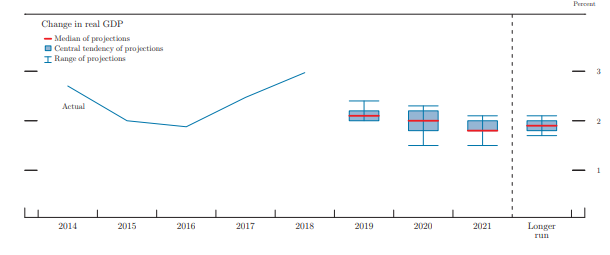

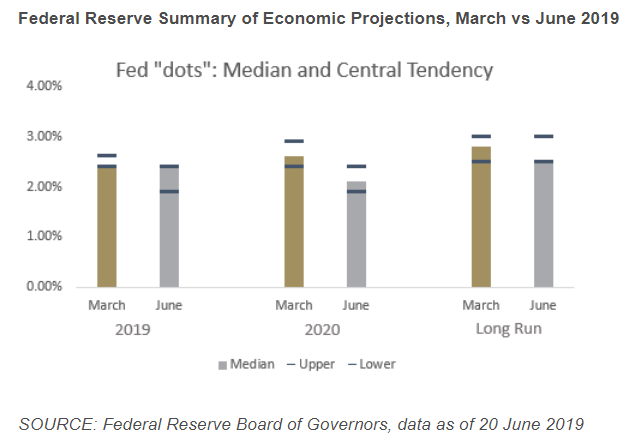

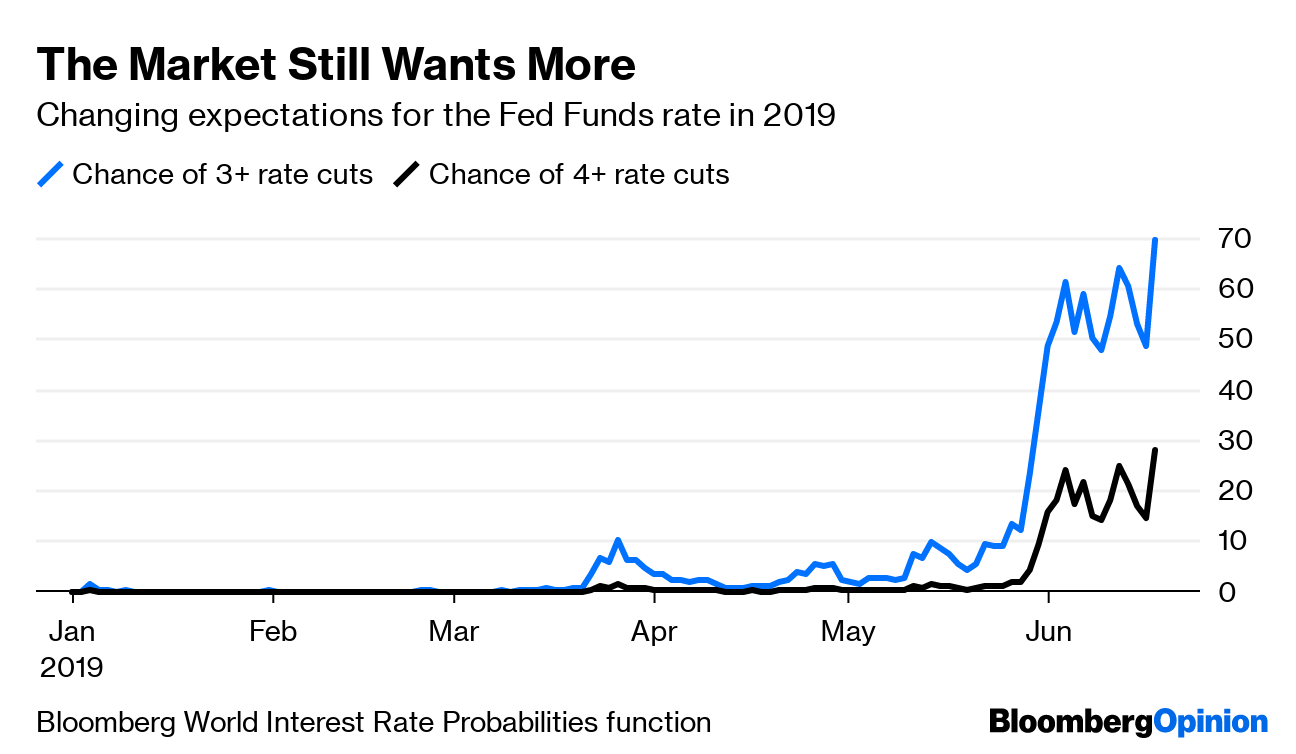

The thanklessness of being Jerome Powell. Central bankers are supposed to have great power, but I doubt whether Federal Reserve Chairman Jerome Powell feels that way. The June meeting of the Federal Open Market Committee that concluded on Wednesday was one of the trickiest of recent times, preceded as it was by a deepening war of words over trade, a collapse in the fixed-income market's expectations for growth and inflation, and a report that President Donald Trump had looked into the legality of demoting Powell. The Fed also had to contend with the fact that the meeting came just ahead of next week's Group of 20 summit in Japan that might become the stage for the next big development in the U.S.-China trade dispute. The FOMC did not want to be seen to affect that outcome in either direction. Thus, Powell's short-term aim was to get through this FOMC meeting without cutting interest rates or being seen as capitulating to either Trump or the market – while also not doing too much to antagonize anyone. Oh, and Trump also desires a weaker dollar. And yet, remarkably, Powell came up with a combination of statements and assertions that achieved all of this. For only the second time since Powell took over the Fed at the beginning of last year, the stock market gained on an FOMC day. Also, the dollar weakened. However, there is still the potential for lots of trouble ahead. First, note that the market and the Fed are still out of sync. These are the Fed's latest growth projections. They are unexciting, but they suggest zero chance of a U.S. recession, implying that the recent bond rally rests on faulty foundations:  That is not an optimistic projection, but with recession predictions widely bandied around, the message is clear that nobody on the FOMC think there is any risk of an economic contraction any time soon. Meanwhile, the central bank's main communication mechanism for the likely path of monetary policy, the notorious "dot plot," appeared to give the market what it wanted. The Fed presented in a chart the predicted path for interest rates of every FOMC member. As illustrated here by Bank of NY Mellon, this showed a dramatic move in a dovish direction (more cuts in rates) since the dots were last published in March:  This is a significant shift and shows that half the FOMC now expects two rate cuts between now and the end of the year. Add the public dissent in favor of cutting rates immediately away by Federal Reserve Bank of St. Louis President James Bullard, and this was about as dovish as the Fed could possibly have been without actually lowering rates. The Fed had little choice because of the dramatic rally in the bond market. It certainly wasn't because of stocks, which are virtually at an all-time high. But the market is greedy. Traders took the dots and immediately priced in more than on rate cut. The market is putting a 70% probability on the FOMC going a step further than anyone in the dots is suggesting, and cutting rates three times by year's end, according to data compiled by Bloomberg. And there is a significant, based on pricing in the market, that we could see four or more cuts.  So if Powell appeased the market Wednesday, he still suffered the fate of appeasers through the ages by seeing his opponent's demands intensify. Meanwhile, the widespread perception that the trade dispute is driving monetary policy is also a problem. During his press conference, Powell tried to explained that the Fed had been influenced by changes in the outlook for international growth since its last monetary policy meeting at the start of May, and not just concern over the trade negotiations. Specifically, both China and the euro zone are now giving cause for concern over slowing growth. That was made painfully clear by Mario Draghi, president of the European Central Bank, in Sintra on Tuesday. Draghi is now geared to ease policy, via rate cuts or conceivably by asset purchases. That can only have an effect on what the Fed decides. And we can see that short-term inflation expectations are declining in the U.S. Meanwhile, they have utterly collapsed in Germany. And Draghi's dovish words have not engineered any kind of a rebound. The declines have been spectacular:  In short, Powell's hand was forced. So, he did the most he could do to loosen monetary conditions without actually cutting rates. But arguably it was also the least he could do. Beyond very public pressure from bond markets and from Trump, international growth pressures left him little choice. Absent a sharp shift in the evidence and data around global growth, and a sharp change in direction in the fixed-income markets, the pressure to cut will only intensify, and the Fed will have to move even faster to catch up. Meanwhile, the risks for investors are shifting. Should inflation actually come back, any number of trades look very appealing and can be entered cheaply. This list comes from Vincent Deluard of INTL FCStone: The recent collapse of inflation expectations offers investors a historical opportunity to enter reflationary trades at historically low valuations. Gold's impressive advance last month suggest that the yellow metal is about to break the top of its six-year trading range. On the other hand, the three major equity reflation trades (long materials over tech, value over growth, emerging markets versus U.S.) are still at secular lows, offering an attractive entry point for contrarian investors. Meanwhile, the Bank of America Merrill Lynch monthly fund manager survey, which I cited Tuesday, names "long Treasuries" as the most overcrowded trade in the world. With yields low to begin with, bond prices are very sensitive to changes in interest rates. Should we move away from the current deflation scare, which looks overdone, then recent history suggests that there is much money to be lost, especially as many investors leverage up to buy fixed-income assets. The following chart shows total returns in the Bloomberg Barclays indexes for long-duration Treasuries and German bunds. Over the last decade they have done very well, but bunds have suffered two very sharp reversals, the second of which was driven by reactions to the Brexit referendum (seen as deflationary) and then the election of Trump (seen as inflationary).  To put it differently, if inflation fears recur, it will be as though fixed-income investors have stepped on a very large rake, which proceeds to hit them in the face. And there will be nothing Powell can do to save them.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

Post a Comment