Welcome to the Weekly Fix, the newsletter that isn't complaining about a Fed that took pre-emptive action to ward off inflation and also wants to take pre-emptive action to allay a downturn. – Luke Kawa, Cross-Asset Reporter

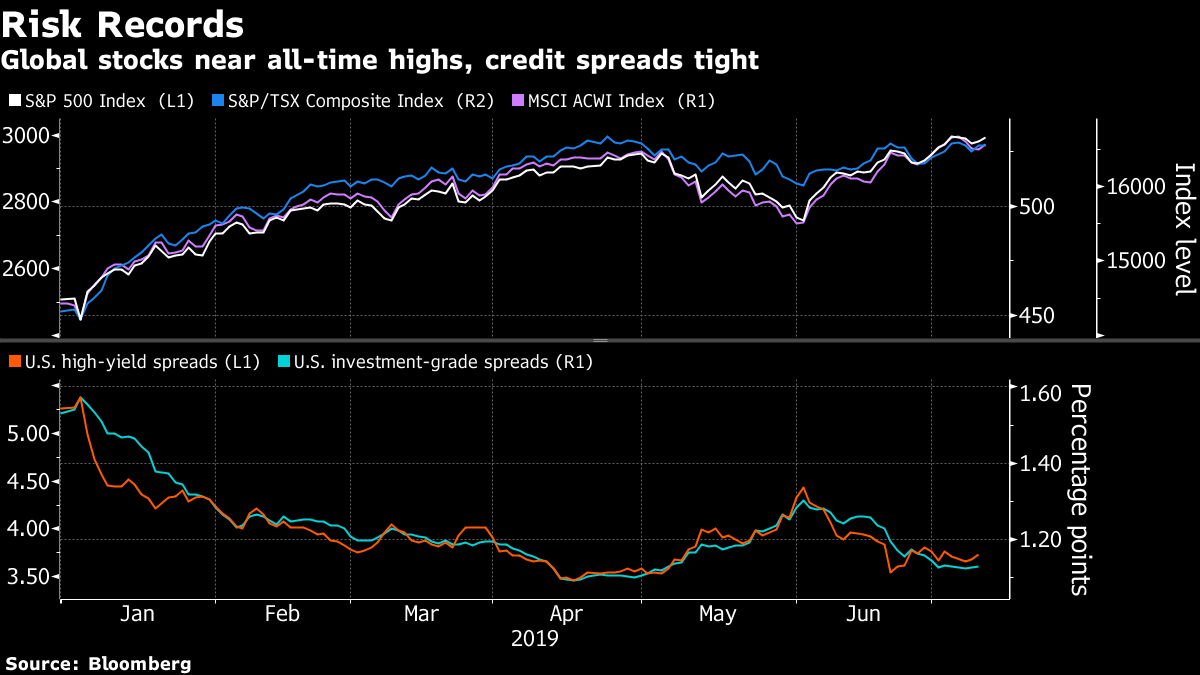

R.I.P. Everything Rally

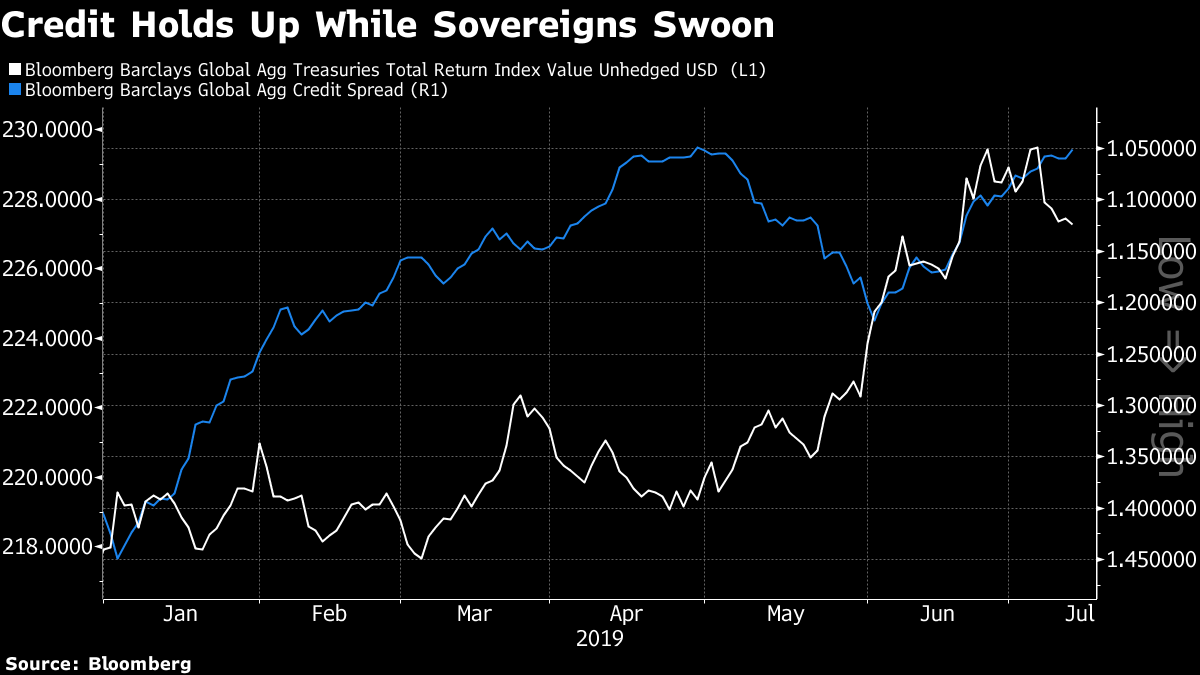

20/20 Hindsight Capital here: As soon as negative-yielding European junk bonds made it to the front page, the "everything rally" across asset classes had to come to an end.

The irony is that to keep the cross-asset narrative intact – global activity is gloomy but not dire, and central banks are coming to the rescue to ensure it doesn't get worse – it's the longer-term risk-free sovereign bonds that have borne the brunt of the adjustment process, not European high-yield companies whose debt is trading with yields below zero.

This week has seen the beginnings of duration risk, rather than credit risk, falling out of favor in the marketplace. It's the bonds, not the corporates, that have been the issue.

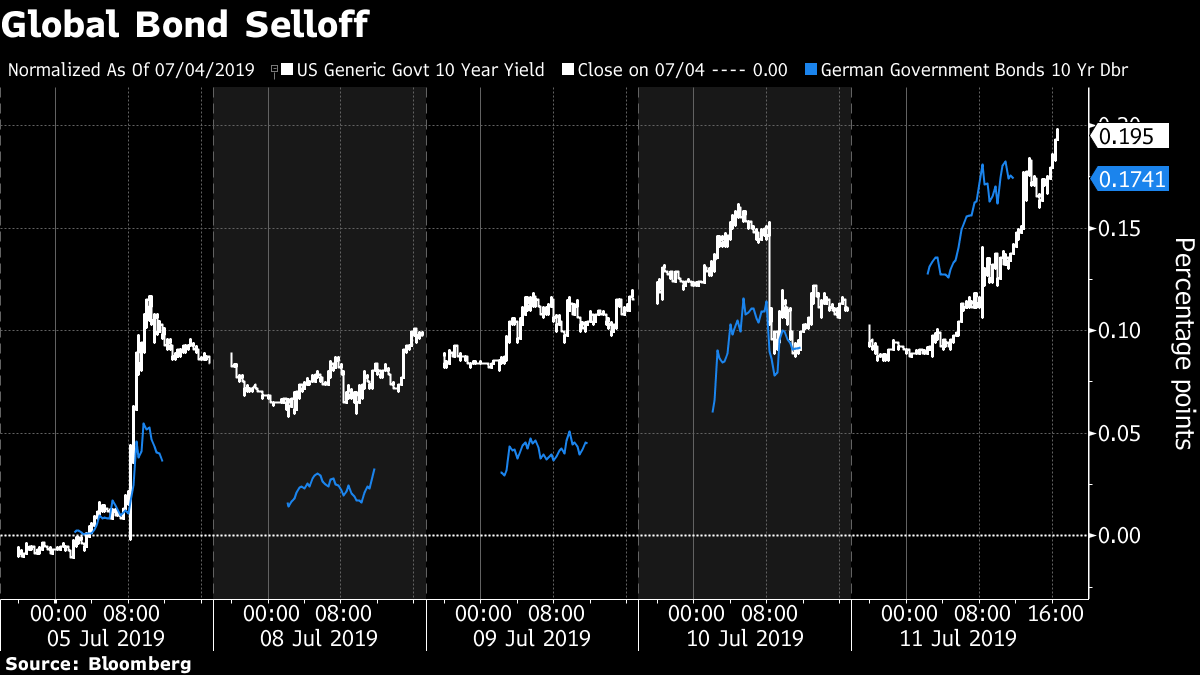

Between firmer than expected U.S. job growth and core CPI inflation and a pop in French industrial production, both American and German 10-year yields have risen nearly 20 basis points since last Friday. If the world isn't falling apart but central banks are still easing, there's a limit to how much longer-term yields should fall. The probability attached to tail risk scenarios involving a return to the zero lower bound in the U.S., and the potential for deflationary spirals, ought to diminish.

With the market pricing at least one Fed cut coming soon and other major central banks expected to add accommodation in coming months, this dynamic brings to mind a tweet from macro trader Jeremy Wilkinson-Smith:

"Central banks held on for 6-9 months of crappy data to stop out at the Low!! Ohhh I know that feeling all too well."

Or, put differently, a note from RBC's Tom Porcelli:

"Right now the Fed is cutting when growth prospects are nowhere near weak and Fed funds is close to neutral. Theoretically, risk assets should love this setup. In fact let us re-state that: in practice, risk assets should absolutely love this setup."

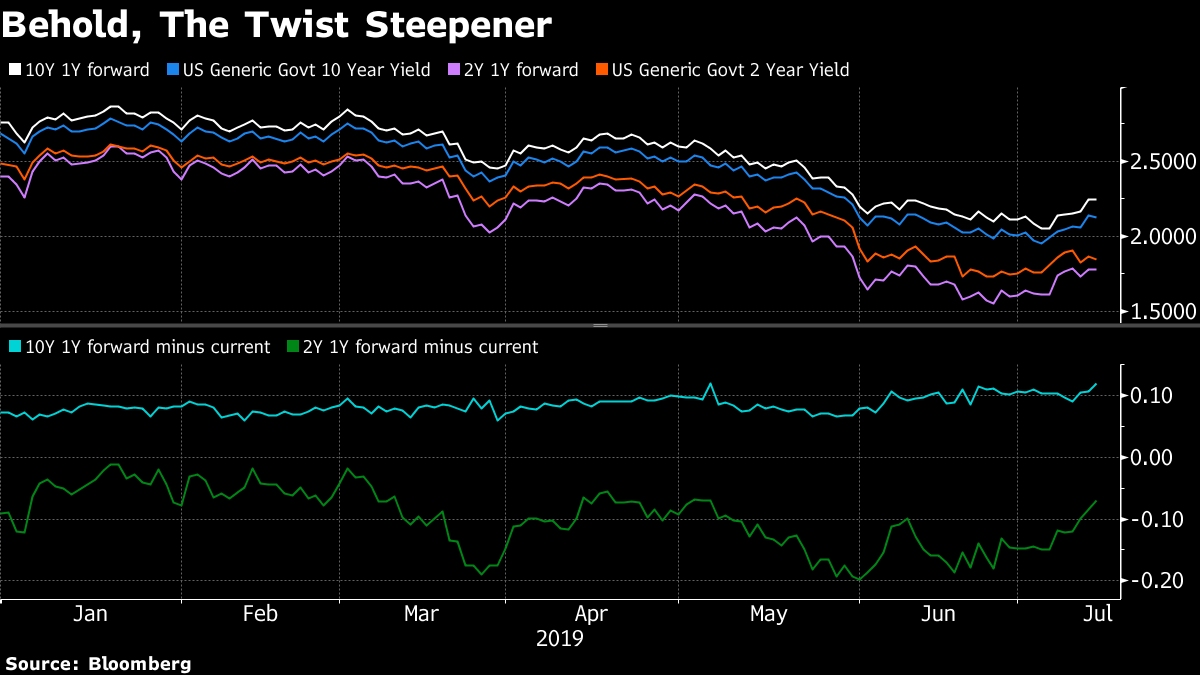

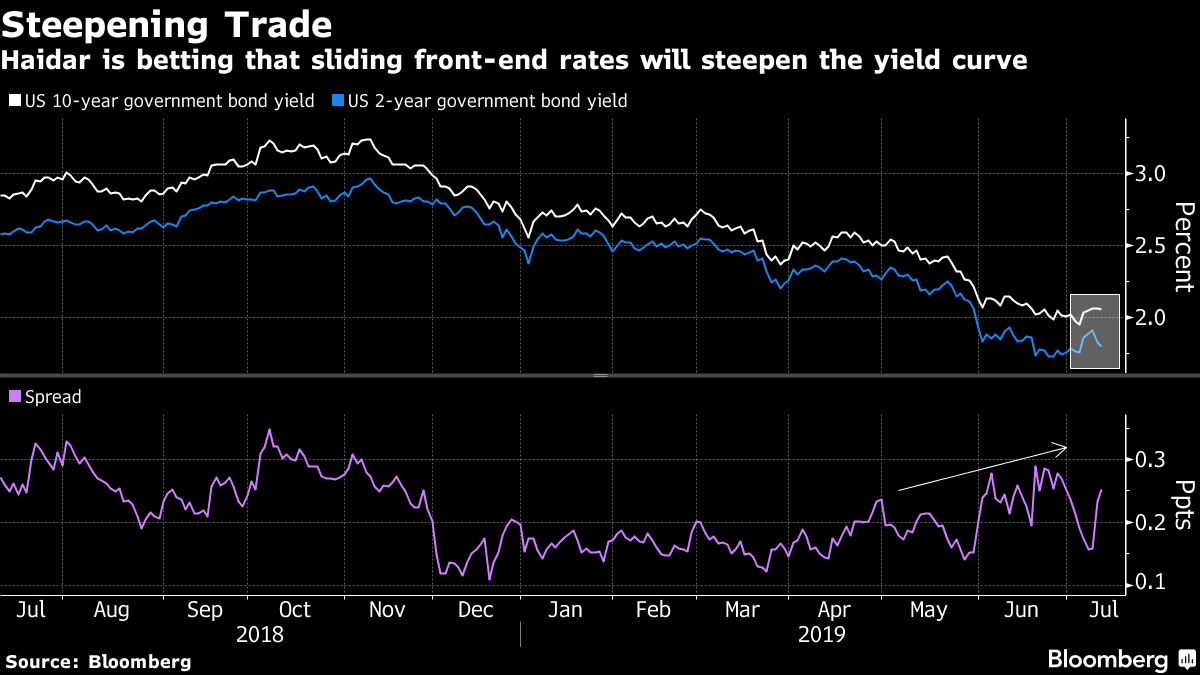

A look at forward curves suggest the world's preeminent long-term, risk-free asset – Treasuries – is expected to continue to be among the first casualties of the end of the everything rally.

The so-called twist steepener (two year bonds rallying while the 10-year sells off) is still firmly entrenched as an anticipated trend for the year ahead. It's "supposed" to be driven more by the bear side, which is a shift from when we last discussed this phenomenon: that points towards less Fed easing over the short term, and enhanced faith in the outlook for global activity.

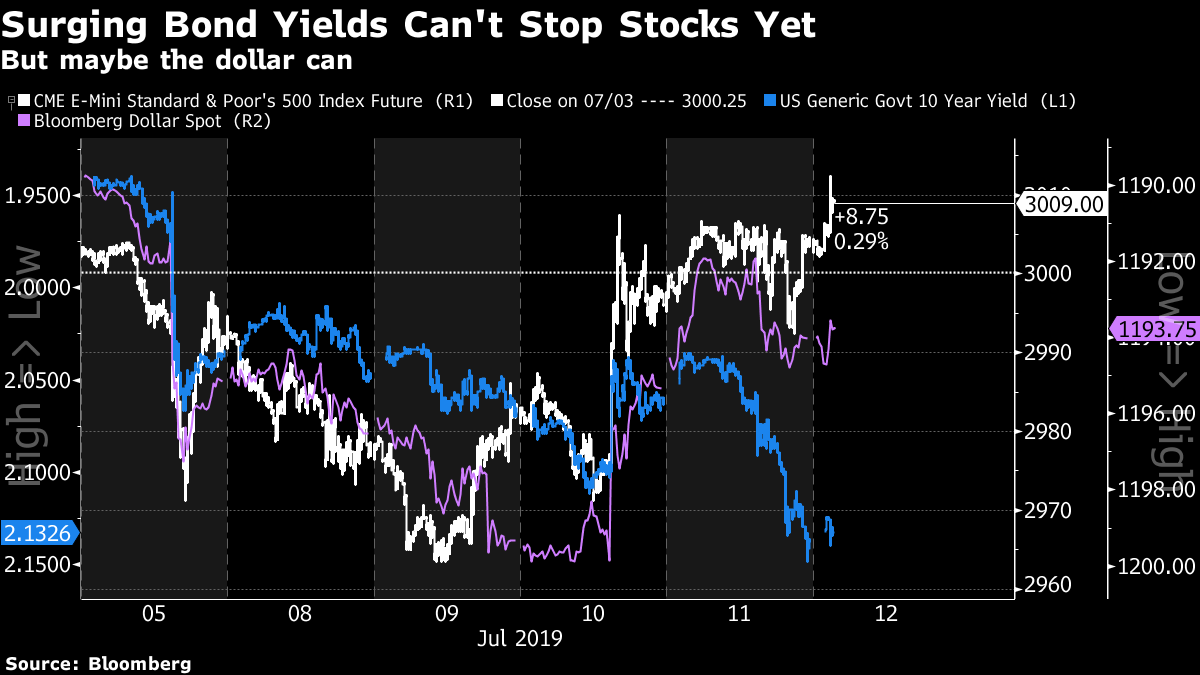

Equity bulls ought to be thrilled by the idea that U.S. stocks can hit fresh records even amid a reversal in the tumbling long-term yields that had been juicing valuations.

This dynamic, if sustained, allows for good economic news to be good news for risk assets (so long as earnings hold up, too!). It helps that central banks, namely the Fed, are perceived to be slightly data-independent at this juncture; poised to boost stimulus no matter what. As such, it's notable that this phenomenon appeared on the heels of good data from outside the U.S. coupled with Powell cementing the Fed's commitment to ease this week.

"I think it is extremely important that equities are rallying with the 10 year Treasury yield ticking higher," wrote Peter Tchir, head of macro strategy at Academy Securities, in a note on Thursday. "We have been in a cycle where rate expectations and stocks were highly correlated and were not getting many 'risk-on' days. Today is 'risk-on'."

It's clear that if there's a macro factor that's weighing on U.S. stocks, it's the dollar, not yields. This is a triumph of levels over rate of change: the greenback is much closer to cycle highs –that is, pain levels – than longer-term U.S. yields.

Something that may keep a lid on the selloff in long end bonds: market participants surveyed by the New York Fed in the immediate aftermath of Powell's "act as appropriate" remarks in early June say the federal funds rate will average 2% over the next decade – completely erasing the "Trump bump" in the wake of the 2016 U.S. election. Market participants' assessment of how short rates will unfold has proved a fairly reliable upper bound for where the 10-year yield will trade in the history of this survey – at least before 2018.

There's more proof in the global price action:

The European periphery – especially Italy – is enjoying spread compression relative to Bunds and seeing high demand for new issues. Emerging Europe has negative yields.

And Citi's Michael Anderson, who has espoused a cautious tone on U.S. junk bonds of late, isn't willing to stand in front of what appears to be a runaway train.

"High yield investors seem very eager to jump into the rate rally with both feet," he writes. "Who can blame them?"

Post a Comment